Financial assistance at the birth of a child

It is not the employer's responsibility to pay financial assistance at the birth of a child.

The employer may decide to provide employees with this type of social support independently. The conditions and procedure for the payment of material assistance, as well as its amount, are established by a labor or collective agreement or a local regulatory act (Article 8, Article 41, Article 57 of the Labor Code of the Russian Federation). In contrast to payment at the expense of the employer, financial assistance for the birth of a child from the state is paid to all young parents. However, it is called differently - “one-time benefit for the birth of a child.”

Working citizens apply for this payment at work, but the employer does not spend his own funds - the costs of the one-time benefit are reimbursed by the Social Insurance Fund. In 2021, the payment amount will be 17,479.73 rubles. Only one parent has the right to receive the payment, and the second will have to provide a certificate stating that he did not receive such benefits at his place of work.

State aid

If the employer is not obliged to provide financial support to the employee, is financial assistance from the state entitled? What are the conditions for receiving? - questions that puzzle women when preparing to become mothers. The first one-time assistance is awarded for early pregnancy registration. Obtaining it requires fulfilling a simple condition - registering with an antenatal clinic when your pregnancy is up to 12 weeks.

The legislation provides financial support and benefits for women during pregnancy, at the birth of a child and caring for him. Assistance is paid in a lump sum, monthly and by issuing a certificate for maternity capital.

Lump sum benefit at birth

Financial assistance from the state to one of the parents (guardians, trustees) regardless of social status - a one-time benefit at the birth of a child. From 02/01/2018 the amount of the benefit in cash equivalent is 16,759.09 rubles and is indexed annually (Federal Law No. 444-FZ dated December 19, 2016). The indexation coefficient is set both at the federal and regional levels, taking into account the climatic conditions of the area.

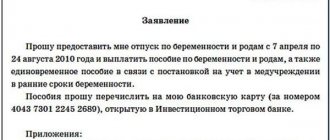

You must apply for funds before your child reaches six months of age. The benefit is paid in the amount in force on the date of birth. Payment is made by the employer within 10 calendar days.

Upon receipt at your place of work, you need to write an application for payment; the sample completion includes a list of attached documents:

- a certificate from the second parent’s employer confirming non-receipt of benefits;

- a copy of the child's birth certificate.

Priority in receipt is given to working family members. If one parent is unemployed, the other parent receives the money due. When registering with the social security authorities (if both parents do not work), additional documents must be submitted:

- passports (originals and copies);

- work books and copies of the first and last pages confirming the fact of termination of the employment contract;

- copies of diplomas for students without work experience, certificates from the educational institution.

Upon divorce, funds are paid to the parent with whom the child lives. Adoptive parents and guardians additionally submit supporting documents.

One-time Putin benefit

From 01/01/2018 Federal Law No. 418-FZ came into force, which introduced a new allowance for the first child for needy young families - financial assistance proposed by V. Putin, called the “Putin payment”. To receive it, you need to confirm the status of a “young family in need” and fulfill a number of indicators:

- spouses must be under 35 years of age or at least one spouse whose age does not exceed 35 years;

- one of the spouses must have Russian citizenship;

- the average monthly income per family member (the calculation period is the total income for the year preceding the application) cannot exceed 1.5 minimum wages;

- the date of birth of the child (adoption before 3 months of age) falls in 2021;

- The age of the child at the time of application should not exceed 1.5 years.

The size is set equal to the cost of living in the 2nd quarter of the previous year, subject to adjustment by regional coefficients. In 2021 the average figure was 10,523 rubles. For subsequent children, assistance is provided from maternity capital funds.

Is maternity assistance provided to both parents?

Financial assistance for the birth of a child is paid by the employer only if the provision of this type of social support is provided for by internal documents. Payments are provided at the expense of the enterprise's own funds, most often from the retained earnings fund, so the employer does not care whether the second parent, working in another organization, received such assistance.

Nuances when paying money may arise if both parents of a newborn child work in the same organization. In these circumstances, you must also be guided by the provisions of the collective agreement or other document defining the procedure for providing payments. If it specifically states that only one parent can receive assistance, only the mother or father of the child will be able to apply for the payment. If there are no such instructions in the contract, both parents can apply.

Important! A local act may indicate that the payment is provided only if the employer has available funds. If the director or other authorized person decides that the company does not have the financial ability to pay financial assistance, the application will be rejected.

Taxes and fees

In order not to pay income tax, according to the law, this type of assistance should not exceed 50 thousand rubles (clause 7 of Article 217 of the Tax Code of the Russian Federation).

Thus, there will be no tax withholding on financial assistance for the birth of a child in 2021 if:

- it was no more than 50,000 rubles;

- received by the parent before the child reaches the age of 1 year.

For more information about this, see the article: “Personal income tax on financial assistance.”

Keep in mind: absolutely similar rules apply to insurance premiums (subclause 3, clause 1, article 422 of the Tax Code of the Russian Federation).

Registration of assistance

As a rule, to apply for one-time financial assistance in connection with the birth of a child at the place of work, you must submit:

- application for payment of funds; it is compiled in any form;

- a copy of the child's birth certificate.

The amount of payment assigned to an employee upon the birth of a child is established by the employer. Financial assistance is paid in a fixed amount established by the provisions of the collective agreement, or is determined by management individually in each specific case - it all depends on the financial condition of the enterprise and the content of internal documents governing the payment procedure.

Financial assistance from the employer

Not a single legislative act provides for the obligation to pay financial aid to an enterprise or individual entrepreneur to its employees. Obligations can be secured by a local internal document. If there is no such provision in the collective agreement, then financial assistance for the birth of a child from the employer is exclusively an “act of goodwill.”

Amount and source of payment

Financial assistance is paid at the expense of the net profit remaining at the disposal of the enterprise, and is not limited to the maximum amount.

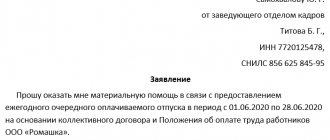

To receive the employee, the following documents must be submitted:

- an application for financial assistance in any form addressed to the manager, indicating the reason (for the birth of a child);

- a copy of the birth certificate or a certificate from the registry office;

- a certificate of non-receipt of financial assistance by the second parent (in case of non-receipt) or form 2-NDFL indicating the amount (in case of receipt).

The manager reviews the application with the attached documents and imposes a resolution within 3 days, specifying the amount. Within the limits of 50,000 rubles, provided payment is made during the first year of life and is of a one-time nature, it is not subject to personal income tax and insurance contributions in accordance with Article 217 of the Tax Code of the Russian Federation.

The one-time nature must be reflected in the order. Even if the assistance is paid in installments, it will remain a one-time payment according to the order. If the director issues a second order for payment, the lump sum will no longer be valid and the additional amount will have to be assessed with personal income tax and all “salary contributions”, regardless of the size.

Both parents (adoptive parent, guardian) can receive financial assistance in the amount of 50,000 rubles, but for the purpose of preferential taxation, careful accountants calculate the total income of the family. Brave accountants calculate 50,000 rubles for each parent, without requiring certificates from the second one’s place of work. The argument and counterargument are letters from the same department - the Russian Ministry of Finance.

- What are the salary supplements?

If the employer has a trade union organization, you can claim mandatory payments from the trade union, provided that the provision is fixed in the collective agreement. In the absence of prescribed norms in internal local documents, you can only be a “petitioner”. Payments to the management of an enterprise do not limit trade union organization in the same way that trade union payments do not influence the decision of the management.

Reflection in accounting

In accounting, payments from the employer at the birth of a child are reflected in the table. For convenience, the calculation and receipt of payments are considered using a numerical example: an employee was given financial assistance in the amount of 60,000 rubles.

| Postings | % of charges | Sum, | Normative | Business transaction | |

| Dt | CT | and deductions | rubles | document | |

| 84 | 70 | — | 60000 | Director's order | Financial assistance awarded |

| 70 | 68 | 13 | 1300 | Article 224 of the Tax Code of the Russian Federation | Personal income tax withheld from 10,000 rubles |

| 84 | 69.1 | 2,9 | 290 | Article 426 of the Tax Code of the Russian Federation | Contribution to the social insurance fund has been accrued |

| 84 | 69.2 | 22 | 2200 | Article 426 of the Tax Code of the Russian Federation. | Contribution to the pension fund has been accrued |

| 84 | 69.3 | 5,1 | 510 | Article 426 of the Tax Code of the Russian Federation | Contribution to the health insurance fund has been accrued |

| 70 | 50 | 50000 + (100000 — 100000*0,13) | 58700 | — | Financial assistance was paid from the company's cash desk to the employee |

| 68 | 51 | — | 1300 | Article 224 of the Tax Code of the Russian Federation | Personal income tax transferred to the budget |

| 69 | 51 | 290+2200+510 | 3000 | Article 426 of the Tax Code of the Russian Federation | Contributions to social funds are transferred |

Financial assistance is paid regardless of the financial results of the enterprise and the personal contribution of the recipient as a specialist. It does not belong to the wage fund either as a salary or as a bonus, since it does not require the fulfillment of production targets. Therefore, they are not taken into account in income tax expenses (clause 23 of Article 270 of the Tax Code of the Russian Federation) and are not reflected in tax accounting. Financing is provided from our own sources.

Application for payment

The form of the application is not established at the legislative level, so it is drawn up in free form.

The main thing is to indicate:

- FULL NAME. directors;

- Business name;

- FULL NAME. the employee submitting the application;

- name of the department in which the employee works;

- content of the request (to pay financial assistance in connection with the birth of a child in accordance with the provisions of an employment or collective agreement, or other local document);

- details of the birth certificate;

- date of document preparation.

The application is signed by the employee submitting it, the immediate supervisor and the person whose authority includes the distribution of funds (most often such decisions are made by the general director of the enterprise). After all the signatures have been collected, the application is transferred to the personnel department - on its basis, an order for the payment of financial assistance is drawn up. The order is received by the accounting department, after which money is transferred to the employee’s bank account.

Maternity benefits (maternity benefits)

In fact, this is payment for sick leave, which is issued 70 days before childbirth and lasts 140 days. It can be received by women for whom insurance contributions were made to the social insurance fund, i.e. the following categories: officially employed, full-time students, contract employees and persons who independently pay insurance premiums for themselves (for example, individual entrepreneurs, notaries, lawyers and etc.)

The amount of payments varies depending on the status of the expectant mother:

working people - 100 percent of the average daily earnings calculated for the previous 2 years, but not more than 340,795 rubles. There is also a minimum limit of 58,878 rubles; it is paid if the woman has little work experience, or the official income was at the level of the minimum wage or below.

students - payment is calculated based on the scholarship

military personnel - calculated based on the amount of allowance

the unemployed, part-time students and the self-employed cannot receive additional payment.

Results

So, financial assistance from the employer is provided to the employee upon the birth of his child only if this type of social support is provided for by a collective agreement or other local regulatory act in force at the enterprise. Help from the employer should not be confused with a one-time benefit for the birth of a child, which is paid by the employer, but not on its own, but at the expense of the Social Insurance Fund.

Sources: Labor Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Personal income tax and insurance contributions from financial aid

According to paragraph 8 of Art. 217 of the Tax Code, financial assistance for the birth (adoption) of a child, paid at the expense of the employer, is exempt from personal income tax only if the following conditions are met:

- the total amount will not exceed 50 thousand rubles per child. Moreover, it can be paid at will to one parent or both, but the total amount should not be more than specified;

- paid to the parent or parents, as well as guardians in the case of adoption;

- produced at one time (is of a one-time nature);

- paid within one year after the birth or adoption of the child.

A similar approach to exemption from calculation and payment is applied in the case of insurance contributions to the Pension Fund, as well as social and compulsory health insurance funds.

It should be noted that the employer has the right to set the amount of material payment in any amount, including exceeding 50 thousand rubles. But only the specified limit will be exempt from personal income tax and insurance premiums. The amount exceeding this is subject to taxation in the usual manner.

“Putin’s” benefits for children from 3 to 7 years old

The payment was introduced by the President in January 2021. The right to the new benefit will be available to families whose average per capita income is below 1 subsistence level established in the region of residence. Please note that compared to “Putin’s payments” for up to three years, the criterion of need has already been significantly increased.

The amount of the benefit in 2021 will be 50% of the subsistence minimum per child established in the region of residence, that is, the national average payment will be about 5.5 thousand rubles .

From 2021, some families will no longer be able to receive 50, but 100% of the regional subsistence minimum per child.

Maternal capital

Since 2021, they began to issue it for the birth of not the 2nd, but the 1st child. Amount 483,881 rubles . At the birth of the second and subsequent child, another 155 thousand will be added. The program itself has been extended until the end of 2026.

You can find out more about the changes and the procedure for payments under the maternity capital program in the following article.

Child care allowance up to 1.5 years old

for working citizens - the benefit will be 40% of average earnings for the last two years, but not more than 29,600 rubles per month

for non-workers - for the 1st child 6,752 rubles, for the 2nd and subsequent children 7,082 rubles.

You must apply for benefits from your employer. In case of lack of employment, contact the social security authorities. Child care benefits for children up to 1.5 years old are accrued the day after the end of sick leave for pregnancy and childbirth. By the way, instead of the mother, the father or, for example, the child’s grandmother can apply for leave and benefits.

The legislative framework

| Legislative act | Content |

| Law No. 418-FZ of December 28, 2017 | “On monthly payments to families with children” |

| Article 217 of the Tax Code of the Russian Federation | "Income not subject to taxation" |

| Article 422 of the Tax Code of the Russian Federation | “Amounts not subject to insurance premiums” |

| Letter of the Ministry of Finance of Russia No. 03-04-06/24978 | “How, for personal income tax purposes, to document the fact of receipt of financial assistance at the birth (adoption) of a child by the second parent” |

Alimony with financial assistance

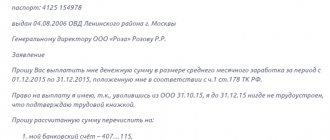

There are often situations when a baby is born in a second marriage and already has a half-brother or sister. The new father claims to receive financial assistance from the employer, and the ex-wife claims to withhold alimony from this amount. Is this legal?

According to Russian legislation, child support payments are withheld not only from the main type of income, but also from other types:

- pensions, pension supplements;

- unemployment benefit;

- scholarships;

- income from rental real estate, vehicles, etc.

The main question that concerns men with children from their first marriage: is alimony taken from additional payments from the employer (financial assistance)? The problem is quite acute, since Russian wages are low, and the amount of payment upon the birth of a baby is quite large.

Russian legislation allows alimony to be withheld from certain types of financial support from employers, guided by the principle of the intended purpose of the funds issued.

If the money is transferred to fulfill a certain social task, alimony cannot be withheld from it. If the lump sum payment is additional to the salary, it is allowed to collect alimony.

Let's take a closer look at the types of financial assistance with which alimony maintenance can or cannot be collected.

Cases of withholding alimony with assistance

Alimony is subject to non-targeted financial assistance.

Inappropriate provision of funds means that the employer does not intend to help the employee in resolving a specific issue. These types of financial assistance include payments:

- when granting the next paid leave;

- for a holiday (all-Russian, professional);

- for treatment (rehabilitation, recovery, improvement of general health).

Financial assistance for treatment is a rather controversial issue, and it is difficult to understand whether alimony is withheld from it. The recipient needs to prove that this payment is of a targeted nature, intended to solve a specific critical situation (carrying out an operation, purchasing a vital medication).

When alimony is not withheld

Financial assistance, with which alimony cannot be withheld, must be targeted in nature and aimed at solving social or other critical situations.

This includes cash accruals for the following reasons:

- birth of a child;

- death of a relative;

- Marriage registration;

- fire;

- transfer of an employee to another location;

- theft of property;

- injury;

- disaster;

- terrorist attack

Such cash payments are not subject to alimony, despite the fact that, according to all the employer’s documentation, they are considered financial assistance to the employee.