Labor legislation gives the right to every organization and enterprise to pay monetary rewards to its employees for quality work done (Labor Code, Art. 191). Such incentives are an effective way to motivate the team and individual employees to further improve their work performance, improve and develop their skills.

The conditions for the provision, size, and procedure for calculating bonuses are fixed in collective agreements, internal disciplinary regulations, charters and rules of organizations. Various salary bonuses for work done, exceeding plans, length of service, and fulfillment of special tasks can be paid based on the results of the month, quarter, or year. Taxation of such financial remuneration, the amount of insurance and pension contributions from premium amounts are determined by the Tax Code and the relevant Federal laws of the Russian Federation.

Is the premium taxable?

Types of awards

The most common types of monetary rewards include:

- individual or collective incentives for completing assigned tasks and conscientiously fulfilling duties;

- rewards for exceeding plans and achieving high performance results;

- incentives for completing special tasks;

- payments when an employee reaches significant length of service;

- awards for special services;

- one-time bonuses on the occasion of an important event, for example, dedicated to professional or public holidays, the founding date of an organization, or anniversaries of company employees.

There are different types of employee benefits

Depending on the internal rules of the organization and the decisions of management, employees may be paid several different types of bonuses at once. There are one-time incentives, as well as regular ones, which are awarded based on the results of a certain period. The bonus amount may be set at a certain amount, periodically revised over time, or may be a percentage of salary.

Attention! Moreover, such incentive payments are subject to mandatory tax established by law.

Sources of bonus payments and grounds for their taxation

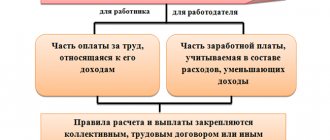

Unlike wages, cash bonuses are not mandatory payments. Such incentives are paid by decision of management in accordance with the internal rules of the organizations. In cases where regular bonus payments are provided for by a collective agreement or the company's charter, refusal to provide bonuses or a reduction in the amount of remuneration must be justified and formalized in the prescribed manner.

Most employers allocate incentive amounts as a separate part of the overall compensation system developed and approved by management for their employees. This makes it possible to interest and stimulate employees to generally improve the company’s performance, and also makes it possible to optimize income tax payments.

Bonus is an optional payment, which is made by decision of management, usually for certain merits of the employee

Sources of bonus amounts can be the cost part included in the company’s budget for salaries, wages for hired personnel, as well as the net profit of the enterprise. In the first case, bonuses are directly related to work activity and achievements at the end of a certain period.

Attention! Incentives from profits are usually allocated in connection with a certain event that is not directly related to the performance of functional duties or work results.

Regardless of whether monetary incentives are regular payments from the cost part of the budget or one-time rewards from profits, all these amounts relate to employee income, which is subject to mandatory taxation by law.

Bonuses are taxed as they are employee income

Salary: concept and composition

To understand whether bonuses are subject to tax and insurance contributions, it is necessary to determine their place in the remuneration system. The concept of wages is established by the Labor Code in Article 129. Wages are remuneration for the performance of labor duties and depend on the qualifications, quantity and complexity of the work. Salary includes:

- salary or tariff rate;

- additional payments, compensatory allowances;

- additional payments and bonuses of an incentive nature.

Bonuses are part of incentive payments. The taxation of employee bonuses in 2021 must comply with the requirements of current tax legislation.

Taxation of insurance premiums

The law defines labor relations as a special type of contractual obligations between employers and the employees they hire. The latter undertake to carry out certain activities within the framework of their position, profession, specialty and qualifications under the guidance of the employer and in his interests. Employees must obey the rules and regulations established within the organization. In turn, the organization hiring personnel is obliged to pay workers, create working conditions that comply with the norms and requirements of labor laws.

According to Article 129 of the Labor Code, all regular, one-time monetary rewards for work performed are part of the general system of remuneration for hired personnel, developed and approved by the management of the organization. In accordance with the Tax Code, which regulates the conditions, rules of contributions to the state Pension, Medical, Social Insurance Funds, payments related to the sphere of labor relations, in addition to various benefits and compensations, are subject to corresponding insurance contributions.

Attention! This rule also applies to incentives in the form of cash bonuses.

Article 129 of the Labor Code of the Russian Federation

The amount of insurance premiums is calculated in the same month when the reward is accrued. It does not depend on the duration of the work for which the remuneration is assigned. For example, in April, management decided to award a cash bonus to the work team for fulfilling the plan in the 1st quarter. It is in the same month that premiums will be subject to insurance fund charges, although the incentive is paid for work done in the previous three months.

Insurance contributions do not depend on the sources of incentive amounts - the salary part of the budget or the company’s net profit, with the exception of certain cases of one-time awards.

Attention! It also does not matter whether bonus payments are provided for by collective agreements and internal rules of enterprises.

Bonuses can be paid from the salary part of the budget, the net profit of the enterprise

Insurance premiums from premium

The taxation of incentive payments depends on the type of bonus and the regularity of its accrual.

Contributions from regular premiums

The size of permanent bonuses, as a rule, depends on the employee’s length of service, his position or production achievements. It can be fixed or set as a percentage of a certain value. Employee bonuses are awarded to:

- based on the results of work over a certain period of time, for example, for fulfilling a plan or achieving certain indicators;

- for completing a specific task;

- for particularly important or urgent work, etc.

Permanent bonuses may not depend on work achievements and may be an additional payment to the salary. They can be paid monthly, quarterly, annually or at other intervals. In all cases, these payments are remuneration for work. Therefore, they need to pay contributions for pension and health insurance, as well as in case of temporary disability and in connection with maternity. They are calculated in the same month in which the bonus is accrued.

Contributions from one-time bonuses

There are two types of one-time bonuses:

- Related to the employee’s production activities.

They are paid for high performance results, completing a complex task, concluding an important contract, etc. Despite the fact that these payments are not included in the remuneration system, they are directly related to the employee’s performance of his job duties. And therefore they are always subject to insurance premiums.

- Not related to the employee’s production activities.

Insurance-free incentives

There are types of one-time monetary awards that are not related to the direct performance of employees’ duties or success at work. They can be dedicated to professional or public holidays, the anniversary of the founding of the company, or dedicated to birthdays and anniversaries of employees. The amounts of such remuneration are usually the same for all team members, regardless of positions, duties performed, length of service, salary, or success in work. Even when these remunerations are provided for, specified in the collective agreement, the charter of the organization and called bonuses in the order, in fact they are not included in the framework of labor relations. Accordingly, insurance contributions are not deducted from such payments.

Often, tax inspectors raise claims against employers regarding the imposition of insurance contributions on one-time premiums dedicated to important dates. This is motivated by the fact that absolutely all amounts paid to hired personnel relate to the sphere of labor relations. However, according to the decision of the Arbitration Court of the North-Western District, if such incentives are paid from net profit, distributed among team members in equal shares, they are not payment for work and insurance fees should not be withheld from them.

Attention! If employees receive bonuses for a special date in different amounts, the court will consider them a reward for the performance of duties and will oblige them to accrue contributions to insurance funds.

It all depends on the type of premiums - some are still not taxed

One-time incentive payments issued as cash gifts to employees under gift agreements concluded with them should not be taxed. Article 420 of the Tax Code defines such actions as acts of civil relations that are not subject to insurance fees.

Thus, contributions to the state Insurance Funds must be withheld from almost all types of premiums. The exception is one-time incentives for important dates or events, allocated from the net profit of companies, issued to employees in equal amounts, as well as bonus amounts issued as monetary gifts under gift agreements.

If bonuses are given to employees in equal amounts and this occurs in connection with important events, they should not be taxed

Income tax

The main type of tax in Russia is the collection on personal income – personal income tax. It is also called income tax. At the same time, individuals include Russian and foreign citizens living in Russia, regardless of gender and age. Profits received by individuals as a result of activities carried out on the territory of the Russian Federation are subject to personal income tax.

Attention! To determine tax payer status and tax rates, citizenship is not the main factor. The fees depend on whether the resident is an individual or not.

The following citizens are tax residents:

- over the past 12 months, living in the Russian Federation for at least 183 calendar days;

- military personnel serving abroad, regardless of length of stay in the Russian Federation;

- civil servants who are on a business trip abroad, regardless of its duration.

Tax resident – not necessarily a citizen of the Russian Federation

There are types of income of citizens that are not subject to personal income tax. Non-taxable income tax payments include the following:

- various benefits, for example, unemployment, in connection with pregnancy, childbirth, child care;

- compensation payments due for unused vacation or upon dismissal from employment;

- pension accruals;

- student and scientific scholarships;

- additional payments for donation;

- monetary awards for high achievements and special merits in science;

- various grants;

- social additional payments, financial assistance;

- compensation for losses resulting from natural disasters and emergency situations;

- various types of alimony;

- rewards for assistance in solving crimes, preventing terrorist acts, and capturing dangerous criminals.

Pensions, various benefits, scholarships, additional payments, etc. are subject to personal income tax.

Attention! Also, funds allocated for charitable activities are not subject to income tax.

Holiday bonus - New Year, May 9, etc.

Taxes:

- Subject to FSZN, BGS.

- Not subject to income tax up to the social security limit. payments (for 2021 - 2115 rubles for main employees, 140 rubles for part-time workers), tax is charged on the excess amount.

- Not included in income tax expenses.

Using a holiday bonus is beneficial for companies that do not have income tax (HTP residents, companies using the simplified tax system, as well as companies with losses) and the salary consists of a salary and a bonus .

How to use:

- If the salary of employees consists of salary + bonus, then in months with holidays you can replace part of the bonus with a bonus for the holiday. This will allow you to save on income tax by using tax-free benefits for social security. payments.

Example: in a company of 50 people, if you accrue part of the regular monthly bonus as a holiday bonus, for example 500 rubles, the income tax savings will be: 50 people. x 500 rub. x 13% = 3250 rub. (for non-residents of the HTP); 50 people x 500 rub. x 9% = 2250 rub. (for HTP residents).

- Instead of an annual bonus at the end of the year, pay a bonus by the New Year.

Due to the income tax-free limit on social payments, it is possible to save one employee at a time in 2021 up to 2115x13% = 274.95 rubles. on income tax for non-residents of the HTP, up to 2115x9% = 190.35 rubles. for HTP residents.

It should be taken into account that the holiday bonus does not count towards sick leave and vacation pay . Because of this bonus, the employee may receive slightly less vacation pay in the future.

Tax rates

Russian tax legislation provides for various types of fees for both residents of the Russian Federation and non-residents. At the same time, the bet sizes also differ and depend on the type of income. The most common value used to calculate taxes for residents is 13% of the amount of income received from the sale of property or in the form of wages. The same rate is applied when withholding income tax on the amount of regular bonuses allocated from the cost part of the organization’s finances, as well as one-time payments from profits dedicated to an important date or special event.

Attention! The type of source of bonus funds does not matter; all cash incentives are subject to an income tax of 13%.

As a rule, personal income tax on income is 13%

For non-residents, 13% is calculated from the following income:

- profits received in the Russian Federation by citizens of other states;

- wages of foreign citizens working in the Russian Federation on the basis of patents;

- income of non-residents who move to the Russian Federation under a program promoting the voluntary resettlement of compatriots;

- income of stateless persons, as well as foreign citizens who have received asylum in the Russian Federation;

- salaries and remunerations of crew members of Russian ships who have citizenship of other states.

There are other rates that are deducted from different types of income. For example, 9% is charged on profits received from bonds, 15% on dividends transferred to individuals from organizations.

Attention! Non-residents must pay 30% of the amount received from the sale of securities to a Russian company.

Some income is subject to different tax percentages

An example of calculation and registration of income tax on bonus payments

Let's consider, using a specific example, all aspects of paying income tax on the bonus amount - calculation, registration procedure with subsequent withholding of personal income tax.

Sergey Tokarev worked for a long time at the manufacturing enterprise Elektropribor CJSC. Now he is retired. Due to his advanced age and health reasons, Tokarev is forced every year to undergo a medical examination and a course of treatment using expensive medications. Tokarev Andrey, his son, followed in his father’s footsteps and also became an employee of the Elektropribor enterprise. At the same time, he is one of its best employees.

At the end of the year, the director of JSC Elektropribor awarded Andrey Tokarev a bonus of 10 thousand rubles for quality work done and success in production activities. At the same time, the manager, at the expense of the enterprise, decided to compensate him for the funds spent on medicine by his father. According to the sales receipts provided by A. Tokarev, this amount is 3.5 thousand. Accordingly, the total amount of bonuses issued by the director of Elektropribor for Andrey Tokarev amounted to 13.5 thousand rubles.

The manager can, at his own discretion, issue a bonus to the employee

The accounting department of the organization was faced with the problem of how to correctly draw up bonuses in order to optimize and correctly calculate the amount of income tax. The accounting department did this:

- as a gift to Andrey Tokarev for the New Year holidays, 4 thousand rubles were drawn up from the net profit of the enterprise, and a corresponding agreement was concluded for the donation of this money;

- another 4 thousand rubles were issued in the form of financial assistance;

- 3.5 thousand were allocated to compensate for the cost of medications for Tokarev’s father;

- According to the official order, Andrey Tokarev was allocated 2 thousand rubles for an annual bonus for successful work.

The task of accountants is to correctly process such payments.

All bonus payments were approved by the relevant orders, signed by the director, executed and documented in the proper manner.

In accordance with the norms of labor and tax legislation, of all amounts paid to Tokarev, only the annual bonus of 2 thousand rubles for labor success will be subject to income tax. All other payments, including financial assistance, reimbursement of the cost of medicines, holiday gifts in the form of cash, formalized by a gift agreement, are not subject to taxation.

So, 13% is deducted from 2 thousand. The income tax amount will be 260 rubles, which will be withheld from Tokarev’s annual bonus. Adding up all the other amounts, we get 13,240. This is the amount of bonuses Ivan Tokarev will receive at the end of the year. If the accounting department had issued 10 thousand rubles as a reward for successful work during the year, the income tax on this amount would have been 1300. In this case, Ivan Tokarev would have received 12200, which is 1040 rubles less.

Financial assistance is not subject to personal income tax

All bonus funds issued by the enterprise must be indicated in the 2-NDFL certificate, which is submitted to the tax authorities. Moreover, each type of payments and deductions is designated by special codes established by the Appendices to the orders of the Federal Tax Service. For example, a monetary gift corresponds to code 2720, material assistance – 2760, compensation for the cost of medicines – 2770, annual remuneration for labor achievements – 2000.

Separately, bonus amounts will be reflected in the 2-NDFL certificate in the application for deduction codes.

| Description | Code |

| Gift code in the form of cash under a gift agreement | 501 |

| Material assistance code | 503 |

| Medical reimbursement code | 504 |

Attention! It must be remembered that in order to exempt a premium from income tax, it must be formalized accordingly, confirmed by an order, agreement and other documents confirming that the payment relates to non-personal income tax items.

It must be confirmed that this or that payment relates to non-taxable personal income tax

Deadlines for paying income tax

The procedure and deadlines for transferring income tax to the state budget depend on the type of bonus. For example, if an incentive payment is tied to salary, the date of receipt of such income will be considered the last day of the month. The time of receipt of bonus funds that do not relate to labor compensation will be considered the actual date of payment.

Income tax must be withheld from the incentive amount on the day the issued money is issued to the employee. Personal income tax must be transferred to the state budget no later than the next day.

Attention! For each day of delay, a fine of 20% of the amount of unpaid income tax is assessed.

Personal income tax is withheld on the day the money is given to the employee

Premium tax

Now let's look at how income tax is deducted from the premium . According to the rules of the Tax Code (Article 226), the day of receipt of the bonus is actually considered the day of its payment. It coincides with the date of personal income tax withholding. That is, the tax on the employee’s bonus must be taken on the day of its actual payment. In this case, the mechanism that the company uses when issuing bonuses is not of fundamental importance. Whether in cash at the company's cash desk, or to a bank account (salary card).

When income tax on the bonus is calculated and withheld, it must be transferred to the treasury. The law allows a maximum of one day for this. The deadline is the next day after the award is issued.

Only international, foreign and Russian awards for outstanding achievements in various fields, which are mentioned in Decree of the Government of the Russian Federation dated 02/06/2001 No. 89, are not subject to personal income tax. At the end of 2021, there are 77 types.

Benefits of taxation of bonus payments

According to the provisions of Articles 255, 272 of the Tax Code, all bonus payments that are paid to employees of the organization for the performance of labor duties are fully included in part of the cost of payment for work. Thanks to this, it is possible to reduce the total amount of company income tax that must be transferred to the state budget. It is advisable for organizations of the following type to use this advantage in the taxation of incentive compensation:

- companies that use a simplified tax system;

- enterprises that use a common taxation system.

To the amount of premium funds issued, organizations have the right to add all fees paid from these amounts to the Insurance Funds. Taking these contributions into account will also reduce your income tax payments.

Sometimes you can reduce your income taxes

To avoid claims from representatives of the tax service regarding tax reduction, all incentive payments to hired personnel should be carefully documented and executed accordingly. It is also advisable to include a detailed description of the provisions on the types, terms, and conditions of providing employee benefits in the internal regulations governing the company’s activities.

Attention! This will allow you to document all bonus payments as a costly part of the organization’s budget allocated to pay for the work of hired employees.

Incentive compensation clauses should be included in such documents.

- An employment agreement or contract concluded with an employee. The presence of a condition for accruing bonuses in such an agreement will allow their amount to be deducted from income tax when transferred to the budget.

- Collective agreement. This agreement must fix the possibility of providing collective and individual rewards for quality work done, labor achievements, and also indicate the amount of funds allocated for these purposes.

The collective agreement must indicate the possibility of providing individual remuneration

- A separate internal document should document the provisions on the conditions for bonus payments to employees of the organization. This local act, drawn up in accordance with all the rules and approved by the company’s management, must indicate in detail all aspects of the provision of bonuses to employees - types, conditions of remuneration, sources of payments, periods of formation and delivery, established amounts or percentage of salaries, the total amount of bonuses included in expenditure side of the budget.

All these regulations will make it possible to completely protect the enterprise from possible accusations by inspection inspectors of tax evasion and illegal reduction of taxation of the company’s profits. In the absence of mention of the terms of provision and the procedure for processing monetary rewards, the management of the enterprise will have to prove the labor orientation of such payments. Otherwise, inspectors recognize bonus amounts as unearned and unrelated to the company’s performance, which, in accordance with the decision of the Ministry of Finance, cannot lead to a reduction in income tax.

What about UST, pension contributions?

All about pension contributions

Payments in this case directly depend on whether the premiums themselves are taken into account as part of income tax expenses or not. In this case, tax authorities take into account the two types of tax separately.

Those who deal with unified social tax are always looking for a reason to charge additional tax. They believe that if any payment is indicated in the employment contract, it means that it is related to direct work. This means that it is subject to the accrual of unified social tax. To avoid such additional charges, it is recommended to exclude any reference to labor when paying expenses. There is no need to include relevant conditions in labor and collective agreements.