Advance and salary

According to Art. 136 of the Labor Code of the Russian Federation, salaries should be paid once every half month. The amount of the first half of the month is the advance payment. It must be paid, even if the employee himself wrote a refusal in writing, otherwise the employer will be fined under Art. 5.27 Code of Administrative Offenses (letter of Rostrud No. 472-6-0 dated 01/03/07). This rule also applies to part-time workers.

The legislator indicates: the employer is obliged to pay both parts of the salary (including the advance) no later than 15 days after the end of the corresponding accrual period, i.e. for an advance payment the deadline is the 30th, and for a salary – the 15th of the next month.

The dates of advance payment are recorded in the LNA. If the days coincide with a weekend or holiday, the advance must be issued a day earlier. The date of issue is one day; it is unacceptable to use a date interval in LNA (Ministry of Labor, document No. 14-2-242 dated 11/28/13).

Is it possible for an external part-time employee to pay wages once a month and not pay an advance?

Problems associated with the withholding of personal income tax may result from the establishment of deadlines for the issuance of wages, incl. advance amounts.

If the advance payment takes place on the last day of the month, the fiscal authorities may require withholding tax in accordance with the Tax Code of the Russian Federation.

The date of actual receipt of income is the last day of the month, this is the moment of withholding personal income tax (223-2, 226-4 of the Tax Code of the Russian Federation, defined by BC No. 09-KG16-1804 of 05/11/16).

If the advance was issued on the 15th, the salary must be issued at the end of the month and a settlement must be made with the employee, which is rarely possible to do. Moreover, if the transfer of income tax from an advance payment is recognized by the Federal Tax Service as unfounded, the amount will be returned to the taxpayer, since it is not considered a tax under the Tax Code of the Russian Federation.

The employer decides how to calculate the advance:

- In the form of a fixed amount (or percentage of salary).

- Based on the actual amount of work (or time worked).

Officials propose calculating the advance in proportion to the time worked, including in the calculation a number of permanent compensation payments, allowances, in addition to the basic salary, or calculating the advance as a percentage, it should be approximately equal to the amount of wages (according to letters of the Ministry of Labor and Rostrud No. 14-1/B -725 dated 10/08/17, T3/5802-6-1 dated 26/09/16, Ministry of Health and Social Development No. 22-2-709 dated 25/02/09).

Calculating time worked is a labor-intensive process. Often the advance is set equal to 40% of the amount of permanent earnings, which, taking into account personal income tax in the final calculation, gives comparable values for the first and second parts of the salary.

On a note! The Labor Code of the Russian Federation does not contain a ban on issuing advances more than once a month, for example, weekly, ten days.

Rules for calculating salary advances 2018

Beginning in October 2021, restrictions were placed on pay periods. Namely, the payment of the second part of the settlement with the employee must be made no later than the 15th of the next month. Despite the fact that on the 15th, in accordance with the current regulatory document, it is still possible to issue a salary to an employee, tax officials recommend fixing an earlier calculation date in internal documentation.

Thus, in order to reflect the dates used in the organization, the specified information should be specified in collective and labor agreements. What punishment awaits the company if the interval between payments exceeds 15 days? The labor inspectorate may impose a fine of 50 thousand rubles.

How much is salary advance?

Advance payment for the first working month

Obviously, when calculating and issuing an advance to a new team member, it is necessary to take into account:

- a fixed part of payments and constant additional payments, allowances, compensations;

- hours worked;

- compliance with legal regulations regarding payment deadlines.

When it comes to an advance in the first month of work, various nuances may arise in the calculation and issuance of this mandatory payment.

Example: an organization has established a fixed advance in rubles. If such a procedure is prescribed in the LNA, then this amount must be given to the newly hired employee. However, in the first month of work he may not earn enough to cover the advance payment because:

- worked fewer days compared to others;

- got sick;

- decided to quit in the same month, etc.

Here the advance acts as an advance payment for labor, and not payment for the first half of the month. An employer, by paying fixed amounts to a newcomer, risks incurring unjustified costs and attracting unwanted attention from regulatory authorities.

In a situation where an employee, including a new one, asks for an advance payment several months in advance, which is also, in fact, an advance payment for his work, it is advisable to draw up a loan agreement, indicating the minimum interest rate. Otherwise, such an advance may be equivalent to an interest-free loan and raise questions regarding the payment of personal income tax and insurance premiums.

A monthly advance to a newly hired employee must be paid without fail, even if he worked only a few days in the first half of the month.

He is not entitled to payment only if he is absent from work, this is the opinion of the judges (appellate ruling of the Moscow City Court on case No. 33-15891/2012 dated 08/07/12).

For example, if a new employee worked on the 14th and 15th, he will be paid an advance for 2 days actually worked, and then his salary will be calculated. If he worked from the first day of the month, the new employee will receive an advance for this month on an equal basis with others, taking into account the organization’s procedure for calculating and issuing salaries for the first half of the month.

If an employee is hired at the beginning of the month, and the advance for the period in the organization is paid at the end of the month, then the salary for the previous month is not due to him as a general rule. However, the period from the start of work to the first advance payment, lasting more than 2 weeks, is illegal.

Eliminate the violation of Art. 136 of the Labor Code of the Russian Federation, it is possible to register in the LNA special conditions for the first month of work of employees - according to the timing and procedure for calculation and payments.

How to calculate salary advance?

Many employees are relatively easily reconciled to the fact that they are paid a fixed payment, while calculating the amount of the advance will not be very difficult.

Let’s assume that an employee’s salary is 60,000 rubles. The salary tax will be equal to 7800 rubles. (60,000 x 13%). Advance payment is made on the 15th of the current month. According to the employment contract, the advance payment is issued based on the actual time worked on the date of its payment, while the date of payment is not included in the time worked in this month. From this, the advance payment for April 2021 must be issued to the employee on the 15th and its amount will be 26,100 rubles ((60,000 - 7800) 20 x 10), where 20 is the number of working days in April, and 10 is the number of days worked.

The calculation is extremely simple and it is easy to calculate the amount of the expected payment yourself.

Vacation in advance

An employee can take leave in the first month of work if there is a mutual agreement with the administration or he is one of the beneficiaries who are denied, according to Art. 122 of the Labor Code of the Russian Federation, it is impossible (pregnant women, minors, adoptive parents, spouses whose wives are on leave for the BiR, veterans, Chernobyl victims, spouses of military personnel). These cases are spelled out directly in the Labor Code of the Russian Federation and in the federal laws corresponding to the categories of beneficiaries. An employee who uses vacation in the same month in which he started working does not have days worked and wages in the calculation period.

According to government document No. 922 dated 12/24/07, paragraphs 7-8, the calculation takes into account the time that he actually worked for this month before the start of the vacation and the amount actually accrued to him. If a citizen, having registered, did not have time to work and immediately took a vacation, the calculation is based on the salary or tariff rate.

Question: The employee was fired on January 16, 2020, personal income tax was calculated and withheld, and on January 17, 2020, personal income tax was transferred to the budget. On January 13, 2020, the employee was paid an advance on wages. Personal income tax was not withheld from the advance payment. When should personal income tax be transferred from the advance in this situation? View answer

Method for calculating advance payment when hiring

Establish in a local act the method for calculating the advance payment when hiring - it should not contradict the requirements of the law, which determines the calculation of the first and second salary payments based on the time actually worked.

It is impossible to establish an advance payment in a fixed amount for all employees - it is impossible to do without preliminary calculations.

In addition, you should take into account the requirements of legal acts and the opinion of officials regarding the minimum and maximum amounts of the advance:

Advance amount

Opinion of officials and legislators

Advance in LNA

Issues of providing an advance in a company should be regulated at the level of local authorities. This applies to both the provision of leave in advance and the issuance of salary advances. Advance leave, if it is provided by law to new and long-term employees, requires that it be specified who will perform their functions during this period and in what order, and what the payment procedure will be.

The procedure for calculating and paying advances is also regulated by the legislator only in general terms. The LNA reflects the algorithms for calculating the advance payment, the terms and procedure for issuance.

For new employees, it is necessary to prescribe a special procedure for receiving the first and second parts of wages for the first month of work, so that no more than 1⁄2 months pass from the start of work to the first payment, regardless of the general salary payment schedule.

For example, if an advance in a company is issued on the 22nd, and a salary is issued on the 7th, you can register in the LNA the receipt of the first salary for:

- accepted in the first two weeks (before the 14th) – on the 15th;

- accepted from 15-21 – 22 numbers, simultaneously with others;

- accepted from 22 to the end of the month - the 7th, the total payment period.

LNA here means an agreement with an employee or a collective agreement with the attachment: Internal Labor Regulations - PVTR (Articles 136, 190 of the Labor Code of the Russian Federation). Based on the wording of Art. 190, it follows that the PVTR can serve not only as an annex to the collective agreement, but also as an independent LNA if the collective agreement has not been concluded.

According to judges and officials of Rostrud, the norms can be prescribed in one of the LNA, but Rostrud considers the provisions of the PVTR to be paramount (document No. PG/1004-6-1 dated 06/03/12, determined by the Moscow City Court No. 4g/5-12211 /12 dated 12/24/12). You can specify all the features of issuing an advance in the Rules, and provide links to the document in other LNAs that address this issue.

The Ministry of Labor changed the calculation of advance payments in 2018

The Ministry believes that when paying an advance, the following are taken into account:

- allowances for night work, for combining positions, professional skills, etc.;

- current salary size.

Here is a list of indicators that are not taken into account when forming an advance payment:

- bonuses;

- compensation payments (overtime, for work on days off, etc.).

All these accruals will be paid with the second half of the salary.

Now let's move on to the most important point. What are the rules for calculating an advance payment in 2021, when can you expect to receive it, and what responsibility does an employer bear if, for one reason or another, the payment is not made within the agreed time frame?

Interesting fact! When calculating the minimum advance amount, all bonuses, allowances, and additional payments are not taken into account - only the net salary. If these bonuses are permanent and not one-time, it is possible to recalculate the amount of the advance, taking into account all bonuses.

Main

- An advance to an employee for the first month of work is issued on a general basis, taking into account the actual time of his work. Issuing fixed advance amounts is not practical.

- The timing of advance payments (salaries) for new employees should be determined so that no more than 15 days have passed from the start of work.

- A new employee can receive an advance payment and labor leave in the first month of work, if the company’s management has no objections. Preferential categories of workers, according to Art. 122 of the Labor Code of the Russian Federation, can use early leave regardless of the consent of the administration.

- Specific terms, conditions, and methods for calculating the advance payment are prescribed in the local NA. It is also advisable to specify the conditions for granting leave to the employee in advance.

The first salary has a separate deadline

When formulating the text of the salary part of internal local acts, be guided by the following rules:

- The salary payment deadline is a specific day, not a calendar period (not a “fork” of dates). Rostrud insists on this.

Find out more here .

- Distribute the days for issuing the first and second parts of the salary so that every half month workers receive payment for their work. This is a requirement of Art. 136 Labor Code of the Russian Federation.

Choose convenient dates based on the specifics of the company’s work. This could be, for example, the 10th day (final payment for the previous month) and the 25th day (advance payment for the current month).

It should be taken into account that with this formulation, newcomers find themselves in a special position - persons who started work on one of the days of the billing month. It turns out that with salary payments on the 5th (calculation for the previous month) and on the 20th (advance for the current month), an employee who started work on the 1st needs to pay only the advance on the 20th. That is, the gap between the start of work and the date of payment of the advance is more than ½ month, which is a violation of the law. We will tell you what to do in such a situation below.

Results

Newcomers must receive their first salary payment no later than 2 weeks after starting work. All subsequent payments are made within the time limits set by the company for issuing wages (every half month, taking into account the actual days worked).

In order to comply with the salary requirements of the law for newcomers, it is necessary in the local act of the company to provide for special deadlines for the payment of the first salary. Otherwise, the employer may be subject to disciplinary, material, administrative or criminal liability.

Every organization has a regulation on remuneration, which determines the procedure and terms for payment of wages. Usually wages are paid twice a month. For the first 15 days worked no later than two weeks. This time is necessary to collect time sheets, make the necessary calculations and organize payment. The regulations may provide for other incentive payments, the decision on which is made by management based on the employee’s application.

Postings for payment of salaries and advances

The main entries for the payment of wages will be as follows:

| Household operation | Debit | Credit |

| Advance issued from the cash register | 70 | 50 |

| The advance money was transferred to a bank account | 76 | 51 |

| The advance is transferred to employee cards | 70 | 76 |

| Advance paid to one employee | 70 | 51 |

| Revenue from the transfer of products as an advance payment is reflected | 70 | 90-1 |

| The cost of production has been written off (which was transferred as an advance) | 90-2 | 43(20) |

| Money towards the basic salary was transferred to a bank account | 76 | 51 |

| Basic salary is transferred to employee cards | 70 | 76 |

| The basic salary is transferred to the employee’s personal account | 70 | 51 |

Prepaid expense

Based on the Labor Code of the Russian Federation (136 Labor Code of the Russian Federation), wages must be paid every half month. The first payment implies payment for the first half of the month (the so-called advance), and the second payment is the final payment for the month worked by the employee.

Often employers make the mistake of setting an advance at a fixed amount of wages, for example, 40% of the salary. In addition to the fact that this contradicts the very concept of wages, it can also lead to difficulties in paying the final amount.

It is impossible to set an advance in a fixed amount, since in essence it is just a part of the salary. And the salary represents payment for the time actually worked by the employee for the first part of the month, which is calculated based on the salary (tariff rate) plus various allowances, additional payments and bonuses (

Responsibility for failure to pay wages on time

If an employer violates the deadlines for paying wages and advances, which are provided for by the Labor Code of the Russian Federation, then he faces a fine:

- 30,000 – 50,000 rubles – for an organization;

- 1,000 – 5,000 rubles – for an entrepreneur;

- 1,000 – 5,000 rubles (or warning) – for a manager (other official).

Such fines await an organization or entrepreneur who violated payment deadlines once. If the employer violates the deadlines again (repeatedly), the amount of the fine will increase:

- 50,000 – 70,000 rubles – for an organization;

- 10,000 – 20,000 rubles – for an entrepreneur;

- 10,000 – 20,000 rubles (or disqualification from 1 to 3 years) – for a manager (other official).

In addition, if an organization violates payment deadlines and issues wages once a month, this can also be regarded as a delay in payment of wages. And in addition to the fine, the employer will be required to pay compensation for delayed wages.

Insurance premiums and personal income tax from advance payment

By issuing an advance, insurance premiums are not charged and personal income tax is withheld. Personal income tax is calculated only based on the results of the month in which all income is accrued to the employee. Since when paying an advance, the full amount of salary that the employee will receive is still unknown, personal income tax cannot be withheld. Personal income tax is withheld when paying the basic salary for the month.

But do not confuse personal income tax, which is withheld from income received by an employee in kind, as well as material benefits. According to them, personal income tax is withheld from the income that is closer in date to the income received. That is, if, after receiving income in kind, an advance payment is due for the next payment, it is necessary to withhold personal income tax.

There is also no need to calculate insurance premiums from the advance payment. They are calculated based on the results of the month, knowing all the payments accrued to the employee for this period. The same applies to insurance against accidents and occupational diseases. Contributions for them can be calculated only by knowing the accrued salary, and since the advance is only part of it and the salary has not yet been accrued by this day, then there is no need to accrue contributions (

Payment of piecework wages

If the organization has established a piece-rate wage system, then the amount of the advance is set, as a rule, based on the amount of work that the employee completed during the first half of the month. There are no exceptions for such organizations. Accordingly, salary payments should also occur every six months or more often, and the amount should be calculated based on the amount of work performed by each employee. Moreover, if we take into account that the legislation determines for employees who work on piecework pay full time the minimum wage equal to the minimum wage, therefore, the advance payment should not be less than ½ the minimum wage. The comparison takes into account the minimum wage established at the federal level.

An example of an advance payment if an employee is hired in the middle of the month

The third reason: you will have to immediately transfer insurance premiums from the entire payment amount. It doesn't matter that some of the money does not apply to the current month. Such an advance is “other payments within the framework of the employment relationship.” And they need to be taxed in the month when the money is given to the employee.

You will also have to pay premiums for insurance against accidents and occupational diseases. They are always transferred in the month of payment to employees. All this is established by part 1 of article 7, parts 3–5 of article 15 of the Law of July 24, 2009 No. 212-FZ, paragraph 4 of article 22 of the Law of July 24, 1998 No. 125-FZ.

Fourth reason: tax aspect. Such a payment may be considered as an interest-free loan to an employee, from whom the company should have timely withheld personal income tax from the material benefit of saving on interest. If this is not done, the organization may be fined (clauses 1, 2, article 212, subclause 3, clause.

1 tbsp. 223, paragraph 4 of Art. 226 of the Tax Code of the Russian Federation).

Advance to a new employee in the first month of work

Attention: There are no exceptions to the piecework wage system in the legislation. At the same time, this requirement can also be realized with a non-advance model of organizing remuneration.

In particular, in its local documents, the employer can provide for the payment of wages to employees at least every half month based on the actual amount of work performed (Rostrud letter No. 1557-6 dated September 8, 2006).

Question from practice: is it possible to pay salaries once a month if written statements of consent to such an order have been received from employees? No, it is not possible. The frequency of payment of wages is established by the Labor Code of the Russian Federation. Therefore, paying wages at least every half month is not a right, but an obligation of the organization (Part.

6 tbsp. 136 of the Labor Code of the Russian Federation). By paying salaries once a month, the organization violates the requirements of the law.

Is an advance paid to an employee if the vacation starts from the middle of the month?

Accordingly, in this situation the employee does not receive any money. Moreover, he will not receive a salary for either the first or the second part of the month, since there will be no days worked. But he will be paid vacation pay for the entire period. How it is calculated - an example of calculation Initial data: Employee T.V. Makarov returned from his next paid leave on February 5th.

The employee's salary is 40,000 rubles. The employee receives an additional payment for a partner who has gone on vacation in the amount of 50%.

Calculation: The standard working time in February is 19 days. According to the production calendar, the hours worked, including weekends and holidays, includes 9 days.

Advance = (40,000 +20,000) / 19 * 9 = 28,421.05 rubles. Conclusions So, an advance is a part of the salary that must be paid in accordance with labor legislation and other regulations.

Calculation of salary advance

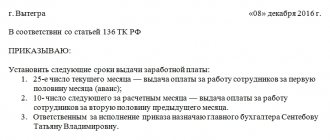

Taking into account the above, the employer must independently determine the dates for payment of wages and register them in the documents. To avoid disagreements with inspectors, pay the advance in the middle of the month (15th or 16th), and pay the salary for the month worked on the 1st or 2nd of the next month.

Meanwhile, the general practice that has developed today indicates that it is quite acceptable to pay an advance before the 20th, and a salary, accordingly, before the 5th.

However, it should be taken into account that such an approach in some cases may cause claims from inspectors, including leading to legal proceedings.

Question from practice: is it necessary to pay an advance on wages with a piece-rate wage system? Yes, it is necessary. The organization must pay employees salaries at least every six months (Part.

6 tbsp. 136 of the Labor Code of the Russian Federation). When calculating advance payments, the accounting department will take into account only working days from September 11 to 15, i.e. 5 working days. Payment of benefits for 6 working days will be included in the final payment for the month. The calculation will look like this:

- the salary of 15,000 rubles is divided by the number of working days in the month, and the average daily wage is obtained.

15000/21 = 714.29 rubles per day.

- The result obtained is multiplied by the days worked.

714.29 x 5 = 3571.45 rubles.

- The amount attributable to personal income tax is calculated

3571.45 x 13%=464.29 rubles

- The amount to be paid is calculated

3571.45-464.29=3107.16 rubles. Total: Taking into account rounding, the employee will be paid an advance in the amount of 3,100 rubles.

To make the calculation, the accountant can use the following documents and data:

- the amount of wages for previous months, if the employee has been working at the company for a long time;

- tariff schedule with allowances and surcharges;

- staffing schedule;

- orders to combine or expand the service area;

- orders for leave, reception and transfer of employees.

When calculating the advance, the total number of working days in the billing period and those days actually worked at the time of accrual are taken into account. Recommendations and regulatory letters indicate that income taxes and other deductions are not levied on the amount for the first half of time worked.

However, if the accountant does not take them into account, the amount will be greater than the amount due on the day of the main part of the salary.

Labor Code of the Russian Federation), and therefore the rules for its provision need to be enshrined in local regulations. Example

- The procedure for paying wages (Section 3 of the Regulations on Remuneration).

3.1.

Salaries at Trading-Consulting LLC are paid:

- 25th day of the current month - for the 1st half of the month;

- On the 10th of the next month - for the 2nd half of the previous month.

3.2. Newly hired employees are paid:

- when starting a job from the 1st to the 14th - on the 15th of the corresponding month;

- for admission from the 15th to the 24th - on the 25th of the corresponding month;

- for admission from the 25th to the end of the month - on the 10th of the next month.

At the end of the first month of work, the employee ceases to be considered newly hired and receives wages in accordance with clause 3.1 of the Regulations.

In 2021, the amount of the fine for the first violation detected is:

- from 10 to 20 thousand rubles per official or entrepreneur;

- from 30 to 50 thousand rubles for the enterprise itself (legal entity).

If a repeated violation is recorded, the amount of fines increases almost 1.5 - 2 times:

- from 20 to 30 thousand rubles per official or entrepreneur;

- from 50 to 100 thousand rubles for the enterprise itself (legal entity).

In addition to a fine, an official may be disqualified for a period of up to 3 years. If other violations of the procedure for paying wages and advance payments are detected, for example, incorrect calculation, a fine is assessed in accordance with paragraphs. 1 and 2 of Article 5.27 of the Administrative Code.

He will be on another vacation until the end of the month. The employee's workdays are marked on the working time sheet from the 1st to the 15th. Obviously, the advance must be paid to the employee in accordance with the time worked, that is, in full as usual.

Vacation pay will be issued to the employee separately, no later than three days before the start of the vacation (13th). The amount of vacation pay will be included in the calculation at the end of the month, minus the amounts issued (vacation pay + advance payment).

Thus, if the start of the vacation falls on any day of the second half of the month, then the money for the current month must be paid in full.

As for the advance for the next month, you need to look at what day the employee goes to work and accrue funds in accordance with the days worked. The entire month Since the employee does not have any time worked on vacation, his wages are not accrued or paid.

Source: https://02zakon.ru/primer-vyplaty-avans-esli-rabotnik-prinyat-v-seredine-mesyatsa/