What it is

The procedure for paying this incentive is confirmed by Article 191 of the Labor Code of the Russian Federation” dated December 30, 2001 N 197-FZ (hereinafter referred to as the Labor Code of the Russian Federation). According to this, the employee is entitled to receive quarterly payments. The fact of accrual of payments is the personal initiative of the employer: it may or may not accrue.

Information regarding whether a quarterly bonus will be accrued is reflected in:

- the employment contract that the employer concluded with the employee;

- local regulations that stipulate the relationships between the working collective of the organization (enterprise).

These documents define the employer’s obligations, which he has no right to violate. If a violation has occurred, the employee can contact the labor inspectorate for further proceedings and protection of his own rights.

Another authority that resolves such issues is the court. You need to contact the judicial authority where the employer is registered if he is an individual entrepreneur or a legal entity.

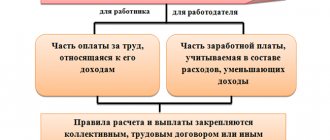

Simply put, a quarterly bonus is an income received by an individual. Therefore, incentives must be taken into account when forming the personal income tax tax base.

Part of the bonus is transferred to state extra-budgetary funds. When a tax inspection (audit) takes place, the inspector carefully studies the process of payment of remuneration at the enterprise (organization).

We bring to your attention a video that explains what a bonus is and how to calculate it correctly.

Normative base

The right to receive a quarterly bonus by workers is determined by Article 191 of the Labor Code of the Russian Federation. However, payment of such incentives is not mandatory.

If an employer applies this type of incentive to its employees, this fact must be reflected:

- in the employment contract concluded between the organization and the employee, in the collective agreement;

- in the employer’s local regulatory documents, such as the Regulations on remuneration or bonuses for employees.

Regulatory regulation

All types of additional payments to employees are divided into non-productive and production. For example, a monthly salary supplement is a production bonus, and payments to employees who raise children are non-production. Quarterly - directly related to work achievements, therefore it is production.

According to Article 129 of the Labor Code of the Russian Federation, salary is the main reward for work done. It also states that it is possible to financially stimulate an employee through a bonus.

The term “bonus” itself is disclosed in Article 191 of the Labor Code of the Russian Federation, which also states that payment is not mandatory.

Violation of employee discipline cannot be a reason for deprivation of bonuses, according to Article 193 of the Labor Code. At the same time, Article 135 of the Labor Code of the Russian Federation states that the last word in resolving such issues remains with the employer.

If a conflict arises, the situation is resolved in the manner specified in Article 381 of the Labor Code of the Russian Federation. The form in which remuneration is paid is reflected in Article 131 of the Labor Code of the Russian Federation.

Bonus upon dismissal

If an employee resigns of his own free will, then bonuses and wages are calculated in accordance with the amount of time worked on the date of dismissal. Unless otherwise provided by the employment contract, a quarterly bonus is still paid, but only for the time actually worked. Full payment of the employee is made on the day of dismissal.

There is also a controversial issue in this, which even in the courts is decided in favor of different parties. If an employee has fulfilled all the terms of the contract under which he is entitled to remuneration, but does not quit at the end of the quarter, when the order can be issued, there is a possibility that he will be left without remuneration, since the employee will no longer have an employment relationship with the organization at the time of the order.

It should be remembered that if dismissal occurs for other reasons, for example due to an employee’s violation of discipline, then no incentive is paid.

When is it paid?

The incentive is paid at the end of the quarter, that is, once every 3 months.

The question of when to list it often arises before accounting workers. The answer to this is contained in letter No. 14-1/OOG-8532 dated September 23, 2016 of the Ministry of Labor and Social Protection. According to this letter, bonuses should be paid only after a complete and objective assessment of the performance of the organization (enterprise) for the reporting period (quarter).

When calculating incentive payments, it is not necessary to be guided by the provisions of Part 6 of Article 136 of the Labor Code of the Russian Federation, which states that wages must be paid no later than the 15th day of the month following the reporting period.

Concept

The quarterly bonus is issued at a certain frequency - once every three months. This also applies to the bonus for the 4th quarter of 2021. It usually occurs when the organization fully achieves all its objectives.

If the company’s performance results turned out to be better than planned indicators, the quarterly bonus (we’ll tell you how to calculate it later) can be increased. Information about this possibility must be reflected in the employment contract.

When an organization does not achieve targets, the staff as a whole or employees of a specific department may be deprived of bonuses. Most employers tie their presence specifically to compliance with standards, since the latter determine the profitability of the organization. In this case, the manager cannot be held liable for non-payment of incentives.

The quarterly bonus is found both in commercial production and in the public sector.

Where does it apply?

The quarterly bonus needs to be understood that, first of all, this is a type of income for an individual, akin to wages. However, there are nuances that differ from salary:

- the employer establishes certain conditions, upon fulfillment of which it can be accrued;

- the format in which the payment will be accrued is decided solely by the employer. According to the law, it can be accrued in the form of: a certain percentage of the salary (a number of calculations are made, the basis for which is the size of the salary for the last 3 months);

- fixed amount (accrued using an order);

It is necessary to remember that there are categories of citizens who are not entitled to quarterly remuneration. These include:

- employees on parental leave for the entire 3-month period. In cases where the employee was on vacation for only part of the quarter, recalculation is necessary;

- employees who were subject to disciplinary sanctions for a specific reporting period.

The employer cannot deprive employees of bonuses at their own discretion. There must be a legal basis for this.

Nuances

Is it taken into account when calculating average earnings?

When calculating the average employee’s earnings, all bonuses that were accrued during the accounting period are taken into account.

So, the quarterly bonus is subject to accounting if the bonus period is included in the calculation period and is fully worked out.

The annual bonus is taken into account as part of the average earnings, regardless of the actual date of its accrual.

Is vacation pay included in the calculation?

Any type of bonus accrued to an employee is included in the calculation of vacation pay, since the remuneration system takes into account all types of cash payments to an employee (except for “holiday” incentives).

Thus, the bonus for the quarter also affects the amount of vacation pay. In this case, only the amounts of premiums accrued in the accounting period are taken into account.

In some organizations, bonuses are awarded depending on the quantity of goods sold or services provided, and therefore represent a significant part of earnings and greatly affect the amount of vacation pay.

What to do if not paid or deprived?

Labor legislation determines the list of citizens who should not receive a bonus based on the results of the quarter:

- persons on parental leave;

- employees who had disciplinary sanctions in a given quarter - it is important that this condition is reflected in the employer’s regulations.

If the deprivation of the employee’s quarterly bonus, in his opinion, was unfounded, this issue is considered by the Labor Dispute Commission or the judicial authorities.

You will find detailed information about depreciation of employees in our article. How to write an application for a bonus for the chief accountant? Find out here.

Is it valid after dismissal of an employee?

If the employment contract or local regulations indicate that the bonus is included in the salary, and the reasons why it may not be paid are indicated, these provisions are taken into account.

Salary with a bonus must be paid to the dismissed person in full, provided there are no misconduct or disciplinary sanctions.

In the staffing table, bonuses in this case are reflected as part of the salary.

Some organizations in their local documents stipulate the payment of incentives to resigning employees depending on the reason for dismissal.

If you resign at your own request, the bonus may not be paid.

It is issued only to employees who are dismissed due to circumstances beyond their control (for example, staff reduction, a medical certificate indicating the impossibility of further work).

All these conditions must be reflected in the contract or local regulations.

If an agreement is concluded with the employer to terminate the employment contract, this document indicates the procedure for paying the bonus.

If nothing is said about its payment, and the phrase “The employee has no material claims against the employer” is present, then the bonus payment may not be provided.

Do I need to pay a deceased employee?

This condition must be defined in the internal organizational regulations on bonus payments to employees.

Usually the bonus is paid in accordance with Article 141 of the Labor Code to the relatives of the deceased who lived with him.

When calculating the bonus, the actual time worked prior to the death of the employee is taken into account.

When should I pay personal income tax on such a payment?

In accordance with the Labor Code of the Russian Federation, a quarterly bonus, regardless of the reason for its payment and the form of calculation, is subject to personal income tax, just like the salary of an employee of an organization.

Is there a regional coefficient?

The bonus in the form of a regional coefficient is taken into account both when calculating the employee’s salary and when calculating quarterly incentive payments to him.

Is there a probationary period?

An employee who is undergoing testing in an organization has the same rights as other employees of the organization in accordance with Article 70 of the Labor Code of the Russian Federation.

His activities are subject to the norms prescribed in the local regulations of the organization; the provision on bonuses is no exception, and an employee on a probationary period has the right to an incentive payment.

Will they pay me if I was on vacation?

This provision is also prescribed in local standards. If a condition is stipulated here for the payment of bonuses in proportion to the time worked, then incentives for the vacation period are not paid.

Attention!

- Due to frequent changes in legislation, information sometimes becomes outdated faster than we can update it on the website.

- All cases are very individual and depend on many factors. Basic information does not guarantee a solution to your specific problems.

That's why FREE expert consultants work for you around the clock!

- via the form (below), or via online chat

- Call the hotline:

- 8 (800) 700 95 53

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

Awards

How to calculate

Bonuses are usually awarded to each employee individually, as a percentage of their salary.

It is calculated as follows:

(amount of accrued salaries for 3 months / 3) * established percentage - 13% personal income tax

When making calculations, the employer should rely on the bonus provisions. This act establishes how quarterly bonuses should be calculated. In addition, there may be periods during which they should not be paid.

If the size of the premium is fixed and agreed upon, then the calculation will be carried out slightly differently:

((fixed bonus amount + salary) * district coefficient - 13% personal income tax) - advance

Another way to calculate bonuses for enterprises, which, when calculated, are based on the actual amount of output. In this case:

(amount of production for the reporting period * agreed percentage + wages) * regional coefficient - 13% personal income tax

In organizations that practice hourly wages, the calculation also takes into account the number of hours worked according to the plan.

How to calculate

There are several ways to calculate a bonus: for actual time worked, a percentage of salary, based on points, and others. The calculation procedure, as well as the indicators for bonuses, are prescribed in the salary regulations and the collective agreement of the organization. Main calculation methods:

- In a fixed amount - the employer sets the absolute indicators of periodic bonuses.

- As a percentage - monetary incentives are defined as a share of the salary, tariff or average salary.

- For actual work time - the actually worked time of each employee is calculated and the amount of payments is determined based on this indicator.

- The share of revenue (plan) is a fixed percentage by which the amount of transactions carried out or contracts concluded for the quarter is multiplied. This is the employee's bonus.

- Points. The point system provides for the accumulation of points over the period of work. Each point has a monetary value. The bonus payment is calculated as the product of the total number of points for the period and the cost of one point.

These are not all calculation methods. The organization has the right to provide one of the above or develop a specific mechanism for quarterly bonuses. The main requirement is to consolidate order in local labor standards.

How to write an order (sample)

An order to assign bonuses to employees can be issued in two ways:

- according to unified forms T-11 and T-11a, which were approved on January 5, 2004 by the State Statistics Committee of the Russian Federation;

- in any form, on a form that was developed and approved within a specific enterprise or organization.

Documents for download (free)

- Unified form N T-11

- Unified form No. T-11a

Orders drawn up in any of these ways will have legal force. From October 1, 2013, the unified form is no longer mandatory. But the same requirements for the volume of information remain.

The order must indicate:

- Title of the document;

- the date it was compiled;

- name of the enterprise (organization);

- Full name of the employee who needs to be encouraged;

- position and structural unit in which the employee works;

- the reason for which the incentive is awarded;

- the form in which the promotion will be given;

- The amount of the bonus payment;

- who provides;

- signature of the person responsible for registration, as well as his position and full name;

- signature of the director (manager) of the enterprise (organization).

The Letter of Rostrud dated February 14, 2013 N PG/1487-6-1 “On the requirements for the preparation of primary documents” confirms the right to use free form documentation for organizations that are not state-owned. But the data listed above must be present.

How are premium payments calculated?

A bonus is a payment that stimulates conscientious work and high-quality performance of work, which is awarded to employees at the discretion of the employer in the manner and conditions stipulated in the employment contract, collective agreement, and regulations on remuneration. The law does not oblige company owners to pay bonuses even if employees successfully complete complex tasks.

If the employer's obligation to pay a bonus is specified in the employment agreement, it is mandatory to pay the bonus.

In order for the accountant not to get confused in the methods of calculating bonuses, he needs to decide what kind of bonus payment should be calculated. Today there are the following varieties:

- Bonuses assigned based on the results of a certain period (month, quarter, half-year, year).

- One-time bonuses assigned suddenly when a special occasion appears, for example, completion of work on a large project, exceeding the quota, connecting to the services of a large client, proposing an innovative idea, etc.

- Bonuses directly related to success in work and not related to work in any way (for example, an anniversary bonus).

The bonus is transferred to the employee’s bank account or paid in cash simultaneously with the salary. Compliance with this procedure is most important if there is a bonus provision in the employment contract.

After calculating the amount of the bonus, you need to issue an order on its assignment (on Form T-11, if it is paid to one employee, and on Form T-11a, if the bonus is assigned to a group of employees), otherwise you may receive claims from the tax inspectorate, since they are not properly filed premiums cannot be taken into account when calculating the taxable base for income tax.

Quarterly bonus for civil servants and employees of ordinary enterprises

Civil servants, as well as employees of ordinary enterprises, are subject to the Constitution of the Russian Federation.

It states that each citizen has the right to count on remuneration for the work done. Remuneration includes, among other things, a quarterly bonus. But to receive it, even for civil servants, it is necessary that the payment be specified in a separate clause in the employment contract. Some civil servants have a special place. Separate legal acts have been developed for them. For example, the accrual of quarterly bonuses to employees of the Ministry of Internal Affairs is regulated by Order of the Ministry of Internal Affairs of Russia dated December 19, 2011 N 1257 (as amended on January 31, 2013) “On approval of the Procedure for paying bonuses for conscientious performance of official duties to employees of internal affairs bodies of the Russian Federation.”

Each of these acts specifies the grounds that may cause non-payment of bonuses. Will not be credited if:

- an employee goes on parental leave to care for children less than 3 years old;

- upon temporary removal of an employee from his position;

- in the presence of disciplinary sanctions;

- if the employee was fired under the article.

When calculating quarterly bonuses for civil servants, one must proceed from the Decree of the Government of the Russian Federation of December 24, 2007 No. 22 “On the specifics of the procedure for calculating average wages.”

Quarterly award in 2021

When is it paid?

The bonus to the employee at the end of the quarter is paid if he fulfills the conditions prescribed by the employer in internal regulatory documents.

Typically, the employer rewards the employee for fulfilling the tasks assigned to him in the reporting period, as well as for exceeding the plan for any indicators.

Conditions may also be specified under which bonuses will not be accrued for the quarter. For example, if the scope of work provided for in the contract with the employee is not completed.

How is it charged and calculated?

When calculating a quarterly bonus, it is important to know how to calculate this payment in accordance with current legislation.

When deciding to reward its employees with quarterly bonuses, the employer independently chooses the form for calculating this type of payment:

- a fixed fixed amount of money (for example, 10,000 rubles);

- a bonus calculated as a percentage of the employee’s earnings (for example, 15% of salary).

Order and rules

This type of material incentive for employees is accrued once per reporting period (quarter).

The timing of the payment of the bonus coincides with the timing of the payment of wages: the bonus must be transferred to the employee along with the salary or in advance.

Failure to pay the bonus within the period established by the contract is considered an administrative violation on the part of the employer.

You can learn how to correctly draw up an order for a bonus from our article. Who signs the 2-NDFL certificate to the chief accountant? Read here.

Revenue code

In certificate 2 of personal income tax, according to the letter of the Federal Tax Service dated August 7, 2021, codes 2002 and 2003 can be used to reflect accrued premiums:

- If the bonus was paid based on the results of production activities (this can include a bonus for the quarter), or for the execution of particularly important orders, it is advisable to use code 2002.

- Code 2003 is used when issuing bonuses based on net profit that do not depend on the employee’s performance (for example, anniversary bonuses).

Minimum and maximum size

The amount of the quarterly bonus to the organization's employees is determined by the local regulations of a particular employer.

The legislation of our country does not impose restrictions in this matter. So, an employee’s bonus may exceed his salary.

There are restrictions on the maximum bonus amount only for heads of government agencies, whose salaries cannot exceed the average salary of other employees by more than eight times.

Calculation formula

Each employer independently determines the procedure for calculating bonuses for the quarter, fixing it in the documentation, so there cannot be a single formula for calculating this monetary incentive.

If the employer takes into account bonus indicators (in value terms) when calculating, then he can develop a formula for assessing the employee’s contribution to the result of the enterprise’s activities.

Algorithm for calculating quarterly bonuses for actual hours worked:

Tariff rate / Standard time per month * Time actually worked (days)

For actual time worked

The incentive payment to a conscientious employee is calculated in proportion to the actual time worked.

The employer can decide how to calculate this payment: depending on the number of days worked per month, or on the number of months worked per quarter.

From salary

If the organization uses salary calculation as a percentage, then the amount of the bonus payment may change with a change in its value, as well as with a change in the value of regional allowances.

How much percentage of the salary will be paid to the employee as a bonus is specified in local documents.

Civil servants

Federal Law No. 79 regulates incentive payments to government employees. They have the right to receive bonuses: based on performance, one-time or monthly.

There are no quarterly bonuses for this category of employees.

On July 26, 2010, the Russian Ministry of Defense issued an order (No. 1010), according to which incentive payments are provided for both civil servants and military personnel.

Civilian employees receive bonuses quarterly, while military employees receive bonuses annually.

In a budget organization

Budgetary institutions must determine the type and amount of bonuses for the quarter, focusing on the rates and salaries provided for by the Unified Tariff Schedule, limited by allocated budget allocations.

Bonus conditions are also prescribed in collective agreements, agreements and other local acts of the organization.

Examples

An example of calculating bonuses as a percentage of salary:

Khimik LLC entered into an employment contract with Mikhailov Nikolai Nikolaevich, according to which he is entitled to a quarterly bonus in the amount of 15% of his salary, which is 20,000 rubles.

Premium calculation:

- Determination of income for 3 months: 20,000 * 3 = 60,000 rubles

- Determining the amount of the bonus: 60,000 * 15% = 9,000 rubles

- Remuneration is accrued in the month following the reporting month: 20,000 + 9,000 = 29,000 rubles

- The amount minus 13% personal income tax is subject to delivery to the employee: 29,000 * 13% = 25,230 rubles

An example of calculating bonuses for hours actually worked:

The organization has set the bonus amount for the quarter at 40% of the salary amount. In the second quarter of 2021, engineer Anton Pavlovich Sidorov (salary 150,000 rubles) worked 40 days instead of the required 55.

In such a situation, the amount of the incentive is calculated as follows: 150,000 * 50% / 55 * 40 = 54,545.5.

From this amount it is necessary to deduct 13% personal income tax; the amount to be issued next month is: 47,454.6 + (50,000 * 13%) = 90,954.6.

Documenting

The decision to pay bonuses to employees, after being reflected in the local acts of the organization, is necessarily accompanied by the execution of the corresponding order:

- Form T-11 “Order of the manager to encourage an employee.”

- Form T-11a - in case of incentives for a group of employees.

Free form bonus order: Sample bonus order

Employees of the organization must confirm with their signature that they have read the order.

Data on the accrual of quarterly bonuses should not be entered into the work book, since these payments, in accordance with the contract, are of a regular nature.

Accounting

| Debit | Credit | Operation |

| 20, 23, 25, 26, 08, 44, 86 | 70 | Reward amount accrued |

| 70 | 50, 51 | The bonus was issued to the employee from the organization’s cash desk / credited to the card |

| 70 | 67 | Personal income tax deducted |

| 91-2 | 69-1 | Insurance payments accrued |

| 08 (91-2) | 69 | Amounts of contributions to extra-budgetary funds have been accrued |

| The date of accrual of the quarterly premium in accounting is recognized as the date of its payment, therefore, insurance premiums are calculated on the same day and does not depend on the actual payment date. | ||

How is it reflected in 6-NDFL?

Form 6-NDFL has been used in the Russian Federation since 2021. It was developed for the purpose of quarterly reporting to the Tax Service on personal income tax. All income subject to income tax is shown here: wages, other payments, and bonuses.

Quarterly bonuses paid are initially reflected in Section 2 of the form and then summarized in Section 1.

Why can they be deprived?

This type of premium is prescribed as a separate clause in the contract or a separate agreement is drawn up. In some cases, an employer has the right to deprive an employee of his enterprise (organization) of benefits. The conditions of deprivation must also be indicated in the contract.

Therefore, if the contract states that the bonus is paid without fail, regardless of certain conditions, then the employer will break the law if it does not pay. Under such circumstances, the employee has every right to appeal to the courts. But the statistics are very ambiguous. Therefore, before going to court, you need to study all the legislative acts.

The process of calculating bonuses for a quarter is quite complex. To feel confident in these matters, you need to prepare in advance.

Calculation of fixed premium

If the bonus for the quarter is set in a fixed form, the salary to be paid should be calculated according to the rules:

- bonuses are added to the salary, the resulting amount is increased taking into account the coefficient;

- Withhold personal income tax and advance payment from accrued earnings.

Let's calculate bonuses based on the following information: an employee of Parus LLC receives a salary of 25,000 rubles, the bonus for the quarter is 10,000 rubles. upon reaching planned production.

- 25000 + 10000 = 35000 rub. — bonuses accrued;

- 35000 – 13% = 30450 rub. — salary to be paid minus personal income tax.

Calculating vacation pay

Accounting for quarterly bonuses in vacation calculations is more than a hot topic. For staff in many commercial establishments, the basic salary consists of various types of incentive payments. For example, when a bonus is awarded for the number of sales or services provided.

When an employee has fully worked out the estimated time, when calculating vacation pay, the quarterly figure is always taken into account on a general basis. In situations where the design interval has not yet been sufficiently developed, the following occurs:

- the bonus, which is assigned in proportion to the period worked, is taken into account in the amount of the full amount;

- the quarterly bonus, which is calculated in a fixed equivalent, is added in strict accordance with the hours worked.

It is also worth paying attention to the months that fall within a specific time period, which is calculated. For example, in bonuses for the third quarter, in situations where only November is taken into account at the beginning of the calculation time, the payment is fixed only for two months.

As part of the calculation of vacation pay, do they take into account the quarterly bonus that is paid for the period that is not the calculated period? When calculating vacation pay, you should take into account only those quarterly bonuses that were strictly assigned within the appropriate period of time.

The bonus structure in various institutions makes it possible to motivate employees, since thanks to this they become directly interested in the results and fruits of their work activities.

Example

As part of the example of calculating a bonus, we should consider the case of its accrual for an individual employee. For example, the salary of an employee of a certain institution for one month will be equal to forty thousand rubles. The internal Regulations established a bonus of seventy percent of the total salary. In the first quarter, the employee worked forty-five days, but, according to the schedule, their number turned out to be fifty-six. In such a situation, the payment amount will be calculated as follows: 40 thousand x 70% / 56 x 45 = 22.5 thousand. Income tax is deducted from the final amount. Transfers to various funds are considered exactly the same.

In the same way, it is also possible to accrue bonuses to any employee. It is only important to know the established percentage of time, the number of days worked and their number according to the schedule. The quarterly bonus in 6-NDFL is displayed.

Monthly bonuses

Monthly bonuses, as well as those that were made over a period of more than a month, are always taken into account differently when calculating average earnings. Thus, the average income can include quarterly payments accrued for the billing period.

If the specified time has not yet been fully worked out, then the quarterly incentive when finding an intermediate indicator is taken into account in full, subject to the following conditions being simultaneously met:

- the period for issuing bonuses is included in the settlement period;

- Incentives are accrued for actual working hours.

When the calculation period is completely exhausted, the quarterly payment is taken into account regardless of the factors that include in the calculation period the time for which the bonus money was accrued.

Hourly wage

For hourly paid employees, bonuses are calculated as follows:

- the average earnings for the last three months are multiplied by the percentage of the bonus payment;

- wages ready for payment are added, as well as the necessary regional coefficients;

- the amount of income tax is deducted;

- the salary amount is obtained taking into account the quarterly bonus.

A rather convenient way is to calculate a quarterly bonus for the personnel of a specific organization, or one employee, through the use of 1C software. A patch to this tool called “Salary and HR Management” is especially suitable for such purposes.