What regulations govern sick pay in 2021?

In ch.

2 of the Law “On Compulsory Social Insurance...” dated December 29, 2006 No. 255-FZ, information is disclosed on cases when insured persons have the right to count on sickness benefits, as well as on the conditions and procedure for paying sick leave. We remind you! From 2021, new rules for paying money for sick leave will apply. For more details, see our memo.

Calculating sick leave after maternity leave in 2021 has certain features related to the lack of income in previous years. When calculating sickness benefits after maternity leave, in addition to the law dated December 29, 2006 No. 255-FZ, you should also take into account letters from the Social Insurance Fund dated November 30, 2015 No. 02-09-11/15-23247 and the Ministry of Labor of the Russian Federation dated August 3, 2015 No. 17 -1/OOG-1105. The main idea of these clarifications is that the insured persons should be compensated for their real earnings, but only that which was before the occurrence of the insured event, and not that which was many years ago. This means that the calculation period for calculating disability benefits cannot be any, but must be determined taking into account the established rules.

If you have access to ConsultantPlus, check whether you calculated the benefit correctly if the employee was on maternity leave during the billing period. If you don't have access, get a free trial of online legal access.

Read about the acceptable amounts of disability benefits in the material “Maximum amount of sick leave in 2021 - 2021” .

Why are years replaced?

Sometimes a situation arises when a woman, while on maternity leave, takes out maternity leave again.

The current rules for determining maternity benefits assume that their amounts are determined based on the employee’s salary data for the previous two years. If a person working for the company was on vacation at that time, then she does not have the salary amounts for the specified period necessary to calculate the benefit. This leads to the fact that maternity payments must be made on the basis of the minimum wage.

However, if an employee worked before maternity leave and has a salary in the previous years, then she can increase the amount of payment received by replacing years. To do this, she needs to bring an application to the accounting department to change the year when calculating maternity benefits.

As a result of this action, salary information will be included in the calculation, which will allow the employee to receive benefits above the minimum.

Attention! Employees must remember that an application for changing years for calculating sick leave can only be drawn up when determining sick pay, maternity benefits or care benefits for up to one and a half years.

If there is a change of years, then the employee’s statement about this is a mandatory document that must be attached to the general package of forms for applying for benefits. It must be stored along with other documents for determining the benefit, since the FSS specialist, when calculating, will consider the legality of calculating the benefit on the basis of the application.

Calculation period for sick leave after maternity leave

According to paragraph 1 of Art. 14 of Law No. 255-FZ, the periods for calculating sick leave can be replaced if the employee has had no income for 2 years due to maternity or child care leave. Social Insurance, in a letter dated November 30, 2015 No. 02-09-11/15-23247, explained that it is possible to replace the years for calculation only with the years immediately preceding maternity leave.

It should be borne in mind that this procedure for calculating sick leave is not the responsibility of the employer, but the right of the insured person. Therefore, it is important to receive a statement from the employee, which will indicate his will and an indication of those years that will relate to the new billing period. As a result, sick leave benefits in the current period should increase, otherwise this calculation procedure cannot be used.

The Social Insurance Fund also indicates the right to choose the year that was not fully worked (this could be the year of leaving maternity leave or the year in which maternity leave began). Non-consecutive years can also be used as a calculation period if, for example, the employee worked during the year between 2 maternity leave.

Example

The employee was on maternity leave from March 2021 to November 2020, after which she returned to work. In May 2021 she goes on sick leave. For previous years her income was as follows:

- 2016 - 115,000 rubles. (full year worked);

- 2015 - 379,000 rubles. (full year worked);

- 2018 (before going on maternity leave) - 84,000 rubles;

- 2019 - no income;

- 2020 (after leaving maternity leave) - 34,000 rubles.

The employee understood that if the earnings of 2021 and 2021 were taken to calculate her benefits, then as a result she would receive sick pay based on the minimum wage. Therefore, she compared her earnings for the years preceding her maternity leave, combining them in different combinations.

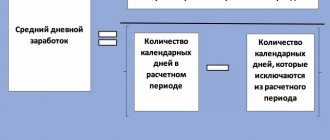

NOTE! When calculating the average earnings for temporary disability benefits, we always divide the salary for the billing period by 730. No periods are excluded from the calculation, and the denominator does not change, including if there were leap years (Part 3 of Article 14 of Law No. 255- Federal Law).

| Period | Calculation of average earnings | Average earnings amount |

| 2016 and 2021 | (115 000 + 379 000) / 730 | RUB 676.71 |

| 2017 and 2021 | (379 000 + 84 000) / 730 | RUB 634.25 |

| 2018 and 2021 | (84 000 + 34 000) / 730 | 161.64 rub. |

Having found out that the highest average earnings would be received if 2021 and 2021 were used as the calculation period, the employee wrote a statement indicating this particular period.

To learn about the nuances when calculating average earnings, read the article “Average daily earnings for calculating sick leave .

Find out how to determine the billing period after parental leave in the Typical Situation from ConsultantPlus. Get trial access to the system and proceed to the calculation example for free.

For what years can maternity leave be replaced?

Is it possible to choose the years for which maternity leave is replaced at will? Law No. 255-FZ does not give an exact interpretation of exactly what periods the retired one or two years can be replaced with. However, there is a ruling of the Supreme Court dated 02/12/18 No. 309-KG17-15902, which states that these years can only be replaced by those immediately preceding them. So, when calculating payments for sick leave received in 2021, instead of 17 and 18, you need to use 16 and 15. If at that time the insured person was also on maternity leave or on parental leave, then they can be replaced with an even earlier one, provided that this will lead to an increase in average earnings!

How is sick leave calculated and paid after maternity leave?

According to the standards for paying sick leave, the average earnings for the previous 2 years are used. But young mothers who have recently returned from maternity leave may have no income during these periods. As stated above, the period can be replaced. But if for some reason replacement is impossible or earnings are below the minimum wage, or even non-existent, then payment must be made according to the minimum wage.

Check the current minimum wage in this material.

There are situations when, of all the possible periods that can be used to calculate before maternity leave, the employee only had income in one year. In this case, the average earnings indicator will still be calculated by dividing the amount of wages for one year worked by 730. And if the result turns out to be less than the average earnings calculated using the minimum wage, then the benefit will have to be paid based on the average earnings calculated using the minimum wage .

The legislation does not provide for the replacement of one year with zero earnings with payment according to the minimum wage.

Example

An employee got her first job in 2021 immediately after graduating from college. For 2021, her earnings amounted to 376,000 rubles. In January 2021, she went on maternity leave, after which she wrote an application for maternity leave for up to 3 years. In March 2021, the employee returned to work, ending her vacation early. But in July 2021, she was forced to go on sick leave. Since there was no income in 2021 and 2021 due to maternity leave, 2021 and 2018 can be taken as the calculation period. In this case, the average earnings will be:

(0 + 376,000) / 730 = 515.07 rub.

It is necessary to compare this earnings with the minimum wage, which from 01/01/2021 is 12,792 rubles:

12,792 × 24 / 730 = 420.56 rubles.

Obviously, in the first case, the average earnings calculated from real income turn out to be significantly higher. It will be used to calculate temporary disability benefits, but taking into account the employee’s insurance experience.

If the employee does not exercise the right to postpone the calculation period at the time of accrual of benefits, then she can apply for recalculation later by writing an application.

Replacing years for calculating B&R benefits: examples

Let's look at examples of the features of calculating the B&R benefit when the payroll period is shifted for an employee who has been working in an organization for 10 years and is going on maternity leave for 140 days.

The size of the minimum SDZ (calculated according to the minimum wage) at the time of maternity leave is 398.79 rubles. (12 130 x 24 : 730).

From January 1, 2021, the minimum wage is set at RUB 12,130.

Example 1

In 2021 and 2021, Stepanova was not on leave for labor and labor and child care. Therefore, we do the calculation without transferring years. In 2018, the employee spent 5 days on sick leave, for which she received a benefit in the amount of 15,000 rubles.

Stepanova’s income in 2021 amounted to 580,000 rubles, in 2021 - 540,000 rubles. The total amount of income for the billing period (2018 and 2021) amounted to RUB 1,105,000. (580,000 – 15,000) + 540,000). The maximum base for contributions to the Social Insurance Fund in 2021 is 865,000 rubles, in 2021 - 815,000 rubles.

The maximum average daily earnings for the specified billing period (2018 and 2019) will be 2,301.36 rubles. (865,000 + 815,000) : 730.

The duration of the billing period is 365 + 365 = 730 days. From it we subtract 5 days of sick leave in 2021: 730 – 5 = 725.

The average daily earnings will be 1,524.14 rubles. (1,105,000: 725), which is less than the maximum possible and more than the minimum permissible.

When going on maternity leave in 2021, Stepanova will receive benefits in the amount of 213,379.60 rubles. (140 x 1,524.14).

Example 2

In 2021 and 2021, Stepanova was on maternity and child care leave. In 2021 and 2021, she worked and did not go on sick leave. You can use these years for calculations.

Stepanova’s income in 2021 is 510,000 rubles, in 2021 - 480,000 rubles. The maximum base for contributions to the Social Insurance Fund in 2021 is 755,000 rubles, in 2021 - 718,000 rubles.

The average daily earnings limit will be RUB 2,017.80. (755,000 + 718,000) : 730

The duration of the billing period is 365 + 366 = 731 days.

The average daily earnings will be 1,354.30 rubles. ((510,000 + 480,000) : 731), which is less than the maximum possible and more than the minimum acceptable.

Stepanova’s B&R benefit will amount to RUB 189,602. (140 x 1,354.30)

Example 3

In 2019-2017, Stepanova was on maternity leave. In 2021 she worked, in 2015-2013 she took leave for employment and childcare, but in 2012 there were no such leaves. Taking into account the possibility of transfers, the years 2021 and 2012 can be taken for calculation.

Stepanova’s income in 2021 amounted to 480,000 rubles, in 2012 - 400,000 rubles. The maximum base for contributions to the Social Insurance Fund in 2021 is 718,000 rubles, in 2012 - 512,000 rubles.

The limit on average daily earnings for the billing period (2012 and 2016) will be 1,684.93 rubles. (718,000 + 512,000) : 730. The duration of the billing period is 366 + 366 = 732 days.

The average daily earnings will be 1,202.18 rubles. ((480,000 + 400,000) : 732), which is less than the maximum possible and more than the minimum acceptable.

The B&R benefit will amount to RUB 168,305.20. (140 x 1,202.18).

Results

Sick leave after maternity leave in the absence of income in the previous 2 years is calculated according to special rules. At the request of the insured person, the periods of earnings used to calculate benefits can be replaced, but only for the years preceding the insured event. As a result of such a replacement, the employee should be in a more advantageous position. It must be remembered that the possibility of changing the billing period is only the right of the insured person, therefore it is unacceptable to change the period without a corresponding application.

Sources: Federal Law of December 29, 2006 No. 255-FZ

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Let's sum it up

- The procedure for calculating benefits for BiR is almost identical to the procedure for calculating benefits for temporary disability, with the exception of certain nuances.

- When calculating the SDZ for the B&R benefit, the actual number of days in the years that are included in the calculation is taken into account. And when calculating sick leave, the duration of the calculation period is always fixed - 730 days.

- When replacing years in the calculation period, the maximum base for contributions to the Social Insurance Fund (for calculating the SDZ limit) is taken for those years that are included in the calculation.

If you find an error, please select a piece of text and press Ctrl+Enter.

Why submit such an application?

The amount of disability benefits is calculated based on data on the employee’s income for the two years preceding the year in which the sick leave was issued (Article 14 of Federal Law No. 255-FZ of December 29, 2006). Only payments under the employment contract from which social insurance contributions were paid are taken into account. If there have been no payments or they are small, payment of the certificate of incapacity for work is made based on the minimum wage.

In order to increase the benefit, it is permissible to change the calculation period - 1 or 2 years. But the right to change years when calculating sick leave in 2020 is not granted to all employees. To do this, the employee submits a corresponding application. Changing the time period for calculation by decision of the employer and without filing an application by the employee is prohibited.

conclusions

On the topic of filling out an application to change the billing period for calculating benefits for certificates of incapacity for work, the following main conclusions can be drawn:

- Citizens who were on maternity leave or caring for a small child during the billing period have the right to choose;

- Changing years is permitted when it is beneficial for the employee;

- To make a replacement, you must provide the employer with a special application;

- If the insured person applies for benefits to the social insurance fund, then the application is submitted to this authority;

- There is no special form established by law. The document is filled out in free form;

- It is better to write 2 pieces: one for the employer, the second for the insured person with a note of acceptance.

What years are allowed to replace

It is possible to change either both years or only one year, but the employee has the right to choose not any years for replacement, but only those that preceded going on maternity leave or parental leave. Changes are allowed if the calendar year period:

- fell completely during maternity leave or parental leave, when the employee did not work a single day;

- partly worked out, and partly due to maternity leave or parental leave.

ConsultantPlus experts discussed how to replace the billing period when calculating sick leave. Use these instructions for free.

Example

The employee has been working for the organization since 2010. In June 2021, she went on maternity leave and then on maternity leave. She returned to work in July 2021. In November 2021, she fell ill and filed for sick leave. As usual, benefits will be calculated based on 2018 and 2021. The employee has the right to replace one or both and choose the following options:

- 2014 and 2015;

- 2015 and 2021;

- 2015 and 2021;

- 2016 and 2021

To determine which option is more profitable and whether the replacement will reduce the amount of benefits calculated in the usual manner, it is necessary to calculate the payment based on income data in the standard calculation period and based on income data with changes.