Our country has legally approved a system of universal insurance for workers in the event of illness, injury or other cases of disability.

To do this, employers transfer an approved percentage for each employee to the Social Insurance Fund (FSS). Sick time is paid from the total funds of the Social Insurance Fund.

Payment of sick leave in 2021: percentage of length of service

Payment of sick leave

The payment methods for sickness benefit reimbursement have not changed in 2021.

The main part is paid by the Social Insurance Fund. Full payment is made in the following cases:

- three pilot projects for payment from Social Insurance Fund accounts have been launched in experimental regions of the Russian Federation;

- in cases of liquidation of the organization at the time of payment;

- bankruptcy of the organization at the time of payment;

- insufficient insurance accruals to pay sick leave benefits;

- child care or quarantine in a child care facility;

- payment of maternity benefits for pregnancy and childbirth.

As a rule, the bulk of sick leave payments are made by the Social Insurance Fund.

Part is paid by the employer:

- the first three days of the employee’s incapacity for work;

- in case of industrial injury with violation of safety regulations.

Note! Funds paid for sick leave come from different sources and can be paid at different times. As a rule, the waiting time for funds from the Social Insurance Fund is longer.

Part of the sick leave payment is provided by the employer

Composition and structure

What does it consist of? The payroll includes the following elements:

- wage. It is paid for work performed;

- wages in kind, cost of production. The law provides for the possibility of paying for labor with the products of an organization or enterprise;

- all types of awards. Formed by the enterprise to encourage employees, engineering, technical and management staff;

- compensation. Related to working conditions, combination of jobs, overtime, etc.;

- cash costs for products, services, food, accommodation, etc. provided to the employee free of charge;

- spending on the purchase of things that are provided to the employee free of charge. For example, uniforms. Can be replaced by benefits for receiving it or cash payments for acquisition;

- expenses for vacations, both main and additional, maternity leave, including compensation for unused vacation;

- remuneration for teenagers' work;

- costs associated with undergoing medical and other examinations, fulfilling duties assigned by the state;

- compensation to employees during liquidation, reorganization;

- bonuses for length of service, continuous experience, long-term work in one place;

- expenses for vacations provided to students;

- compensation for forced absenteeism, transfer to a lower-paid job, for temporary disability (sick leave);

- payments for shift work, travel time, all kinds of delays beyond the employee’s control

- salaries of third party employees under contracts;

- remuneration for student labor;

- special types of pensions and a number of other types of payments.

- targeted payments and bonuses from special funds;

- bonus for the year;

- financial assistance of all types;

- some pension supplements;

- some compensation, for example, for price increases;

- gratuitous loans, payment for travel, vouchers, social benefits;

- dividend payment.

This is important to know: Application for initiation of enforcement proceedings: sample 2021

The structure of the wage fund at the enterprise table:

Deadlines for sick leave payments

In 2021, the rules for payment of benefits neither for the Social Insurance Fund nor for employers have changed. They are carried out in the following order.

Deadlines for employers

An employee can present a sick leave certificate no later than 6 months from its receipt. For relatives of a deceased employee while on sick leave, the period of provision is up to 4 months.

Note! The calculation period is given 10 calendar days from the date of granting sick leave.

The calculation is made taking into account the established rules at the enterprise and the timing of payment of wages.

Excerpt from Article 12 of Federal Law No. 255

Example: an employee brought a sick leave sheet, which indicates the dates of incapacity for work from February 1 to February 12, and they coincide with the attendance sheet. The employee starts work on February 13 and submits the sheet to the personnel department on February 14. With a payment schedule of 5 and 20 of each month, payments are accrued to him on February 24 by decision of management or on the general settlement day of March 5.

Terms of payments to the Social Insurance Fund

The Social Insurance Fund is required to calculate the amount of payments within 10 days from the date of receipt of sick leave.

Note! The payment date for sick leave is no later than the 26th of the next month.

Example: Let's consider for our case. The sick leave was received by the Social Insurance Fund on February 15, and it will be paid until March 26. And if sick leave is received after the first of March, the employee will receive the money until April 26.

Payment for sick leave is due by the 26th of the next month.

Is sick leave income?

In accordance with paragraph 1 of Article 163 of the Tax Code, an employee’s income, taxable at the source of payment, is defined as the difference between the employee’s income accrued by the employer and subject to taxation, taking into account the adjustments provided for in Article 156 of this Code, and the amount of tax deductions provided for in Article 166 of this Code.

At the same time, paragraph 2 of Article 163 of the Tax Code determines that, unless otherwise provided by this article, employee income accrued by the employer and subject to taxation is recognized in the employer’s accounting records as expenses (expenses) in accordance with the legislation of the Republic of Kazakhstan on accounting and financial reporting, money to be transferred by the employer to the employee into ownership in cash and (or) non-cash forms in connection with the existence of an employment relationship.

What periods are included in the length of service?

Payment of sick leave for temporary disability directly depends on the employee’s length of insurance. According to the Federal Law “On Insurance Pensions”, it consists of all time periods when the employer or independently paid insurance contributions to the PRF for the employee.

It includes periods:

- military service;

- care for each child in the family, for a total of no more than 6 years;

- registration with the employment service, if confirmed by a document;

- detention with subsequent rehabilitation;

- care for persons over 80 years old, for disabled people of group 1, for disabled children;

- time of living with a spouse undergoing military service;

- time spent by the spouse in the diplomatic service;

- time of operational work on the task.

Various periods are included in the insurance period

Note! All time periods included in the length of service must be confirmed in the work book or other official documents certified by a notary.

What income is included in the calculation of sick leave in 2021

The main criterion by which an employee’s income is included in the calculation of sick leave is the fact that insurance premiums are charged on such income.

The procedure for calculating insurance premiums on employee income is regulated by Art. Chapter 44 of the Tax Code of the Russian Federation. According to Art. 420 of the Tax Code of the Russian Federation, the object of taxation with insurance premiums is income paid to an employee:

- within the framework of an employment contract;

- under a GPC agreement, provided that the subject of such an agreement is the performance of work, provision of services;

- under copyright contracts;

- under agreements for the alienation of the exclusive right to intellectual property results.

Thus, when calculating income to determine the amount of benefits due to temporary disability, the employer takes into account the following types of income:

- salary calculated on the basis of official salary, hourly/daily tariff rate, etc.;

- premium, bonuses accrued for the employee’s fulfillment (exceeding) of labor indicators;

- bonus for work in harmful/dangerous working conditions;

- additional payment for work on weekends, holidays, night time, overtime;

- certain types of financial assistance, which we will discuss in more detail below.

Please note that an employee’s income is included in the calculation of sick leave provided that it is accrued within the framework of an employment contract, that is, for the performance of job duties.

Financial assistance when calculating sick leave

The procedure for including the amount of financial assistance in the calculation of temporary disability benefits depends on the specifics of calculating payments.

Below we will consider what types of financial assistance are taken into account when calculating sick leave:

| No. | Types of financial assistance | Included/NOT included in the calculation of sick leave | The legislative framework |

| 1 | Financial assistance at the birth of a child | NOT included in the calculation of sick leave, provided that:

An amount exceeding 50,000 rubles is subject to insurance contributions in the general manner and is included in the calculation of temporary disability benefits. | Clause 8 art. 217 Tax Code of the Russian Federation, paragraphs. 3 p. 1 art. 422 Tax Code of the Russian Federation, art. 20.2 of Law No. 125-FZ |

| 2 | Financial assistance in connection with the death of a relative | It is not taken into account when calculating sick leave provided that the following has been paid:

| Clause 8 art. 217 Tax Code of the Russian Federation, paragraphs. 3 p. 1 art. 422 Tax Code of the Russian Federation, art. 20.2 of Law No. 125-FZ |

| 3 | Financial assistance in connection with an emergency | Financial assistance accrued to an employee who suffered from a fire, accident, flood, natural disaster, or other emergency is not included in the calculation of sick leave. The amount of payment in this case does not matter. | Clause 8.3 – 8.4 art. 217 Tax Code of the Russian Federation, paragraphs. 3 p. 1 art. 422 Tax Code of the Russian Federation, art. 20.2 of Law No. 125-FZ |

| 4 | Financial assistance in connection with vacations, weddings | If the company’s local regulations provide for the payment of financial aid for other reasons (vacation, wedding, etc.), then such payment is not subject to insurance contributions (and is not taken into account in calculating sick leave) provided that its amount does not exceed 4,000 rubles. in year. If the established limit is exceeded, insurance premiums are charged for the difference between the actual payment and the limit (4,000 rubles). This difference is included in the calculation of sick leave. | Clause 28 art. 217 Tax Code of the Russian Federation, paragraphs. 11 clause 1 art. 422 Tax Code of the Russian Federation, Art. 20.2 of Law No. 125-FZ |

What determines the payment of a percentage of the insurance period?

The total amount of insurance experience determines what percentage will be included in the calculation of disability benefits from the employee’s average earnings. Social insurance reimburses only well-founded, error-free calculations for payment of sick leave benefits. Average earnings are calculated from total payments for the last two years of work.

The amount of sick leave payments depends on insurance payments and the size of the official salary

In 2021, the percentage of the official insurance period has not changed. Let's look at it in the table below.

Table No. 1. Calculation of insurance period

| n\n | Insurance experience (years) | % of payments | In which cases |

| 1. | 8 or more | 1 | Officially employed, making contributions to the Pension Fund. |

| 2. | Does not matter | 1 | For pregnancy and childbirth. |

| 3. | From 5 to 8 | 0.8 | Officially employed, making contributions to the Pension Fund. |

| 4. | Up to 5 | 0.6 | Officially employed, making contributions to the Pension Fund. |

| 5. | Doesn't matter | 0.6 | Former employees upon receipt of sick leave for 30 days if they are unemployed. |

| 6. | Less than six months | Minimum wage | Total experience less than six months. |

Sick leave, according to the tax code, is subject to personal income tax - 13%

Sick leave payments are subject to personal income tax

What is income

Income of individuals (population) is the income of citizens received in the form of wages, scholarships, pensions, various benefits, payments, compensations. Also, income includes money from the sale of various goods, regardless of whether you produced it yourself or bought it cheaper and sold it more expensive. Also, income arises from the provision of services, from the sale of large movable and immovable property: apartments, cars, houses, etc. Thus, income includes funds from the rental of any property. Very often, low-income mothers have a question: is alimony income? Of course, this money is your income, you will show it in a certificate for the bank for issuing a loan, in a certificate for social services for calculating subsidies for utility bills or child benefits. But alimony, as well as child benefits, lump sum payments at the birth of a child, and maternity benefits for sick leave are not taxed. But they are income!

All income of legal entities and individuals in the country is subject to various types of taxes. And taxes are the state's revenues. Of course, the range of income received by the state is very large, but taxes make up a significant part of it. All taxpayer money forms the state budget, which makes it possible to maintain and finance state structures - police, education, medicine, roads, culture and much more. Budget revenues are contributions from enterprises of all forms of ownership, sizes, types of activities, as well as individuals. In addition to taxes, the state income includes duties, payments for internal and external trade transactions with real estate, natural resources, national cultural values and much more.

In what situations is sick leave paid?

Situations when sick leave must be paid:

- it was received personally by the sick employee during an appointment with a doctor;

- if it is necessary to care for a sick child, a disabled person of group 1;

- during pregnancy and childbirth and in case of complications thereof;

- when caring for an infant up to 3 months, in case of adoption or guardianship;

- when undergoing rehabilitation in sanatoriums and resorts;

- in dental prosthetics.

In order for sick leave to be paid, it must be filled out correctly.

Who is entitled to sick pay?

Categories of citizens who may qualify for sick leave:

- employees working in government agencies: teachers, doctors, librarians, etc.;

- civil servants, state and municipal officials;

- workers and engineers working under an employment contract, regardless of their form of ownership;

- military, contract soldiers serving military service;

- employees of the Ministry of Internal Affairs, Ministry of Emergency Situations, FSB, inspectors of tax, fire services and units.

How to correctly calculate sick leave payments?

An employee who has missed work days for one of the above-mentioned valid reasons, and who has received a stamped sick leave certificate completed and signed by the attending physician in a standard manner at a medical institution, submits it to the accounting department.

An example of a correctly completed sick leave form

The accountant, within a period not exceeding 10 days, must calculate payments for sick leave and submit it for payment.

The accounting calculation consists of several parts.

- Determine the calculation period, which consists of the last two calendar years before the illness. It is always 730 days, and no days are excluded from the calculation (Article 14 of Federal Law 255, Part 1.2).

- Determine the total earnings for the second accounting calendar year:

- it includes all payments for which SSF contributions were calculated (Article 14 Federal Law 255, Part 2);

- All non-taxable amounts are excluded: state benefits, financial assistance up to 4,000 rubles, compensation payments (Tax Code, Article 422);

- You can determine the average earnings for one day using the formula: Average daily earnings = Earnings for the billing period: 730 days

Note! Regardless of the length of the working week or part-time work, calculations are made in the same manner for all employees.

Calculation of sick leave payments is the same for all employees

Then the total labor and insurance experience is determined. The amount of payments to an employee on sick leave depends on the length of his work experience from the first days of his work, which is noted in the work book, employment contract or certificate.

Next, the period is calculated when the length of service was subject to mandatory social insurance tax in case of disability, illness, or maternity.

Periods of other activities subject to social insurance are included:

- business activities: private notaries, detectives, tutors, security guards and others,

- law office,

- collective farmers,

- members of cooperatives.

The calculation takes into account the length of insurance, time spent on sick leave according to the BiR, etc.

First, the experience is summed up for whole years, then added for whole months. All remaining days are summed up and converted into months of 30 days, and they are converted into years of 12 days. The result will be the total number of complete years and months.

Example No. 1 : An employee went on sick leave from May 15, 2021 to May 25, 2021.

Calculation of work experience.

| n\n | Name of place of work | Beginning of internship | End of internship | years | months | days |

| 1. | LLC "Ritual" | 15.03.2015 | 25.10 2017 | 2 | 13 | 40 |

| 2. | LLC "Pamyat" | 30.10.2017 | 14.05.2019 | 2 | 15 | 49 |

| 3. | Calculation of experience | 4 | 28:12=2,4 | 89:30=2,96 | ||

Result: Total work experience will be = 6 years + 7 months

In 2021, when calculating the insurance period, the total length of service is taken into account.

If an employee works in two places at the same time, the length of service is taken into account only for one place of work of his choice.

The calculation takes into account the total length of service

Note! The length of service up to the last day is taken into account, including the day before the opening of sick leave.

The average amount of sick leave benefits per day also depends on the established maximum and minimum limits. Letter of the Ministry of Labor No. 17-3/326 dated February 26, 2013 defines the procedure for calculating benefits taking into account the assigned limit base, which should not exceed the calculated daily base. The payment for 2018 had a limit value. In 2021, there is a maximum value of average daily earnings, which should not exceed the value obtained from the formula.

Table. Calculation of the average daily earnings limit

| Limit for 2021 | Limit for 2021 | Sum | Calculation for every day | Limit on daily earnings in 2021 |

| 775000 | 815000 | 1590000 | 1590000 : 730 | 2150.68 rub. |

When calculating the accrual of benefits for sick leave in 2021, the average daily earnings of an employee cannot exceed the received value - 2150.68 rubles. This means that the total payment of all earnings for the last two years, divided by the number of days 730, cannot exceed the base for which the limit amount is taken.

The calculation takes into account the daily earnings limit

Note! If an employee worked simultaneously in two different organizations, then they calculate the average daily salary based on their accrual amounts. The total figure for the Social Insurance Fund from two organizations may exceed the estimated limit for 2021.

The minimum average daily amount should not be less than the minimum wage approved by the government for 2021 - 11,280 rubles. per month. When calculating using the formula, we get:

11280 (rub.) x 24 (months): 730 (days) = 370.85 rubles.

It is necessary to take into account the minimum wage when calculating the SDZ

When is the minimum wage taken into account when calculating sick leave benefits?

Let's list the cases:

- during the billing period the employee had no earnings due to unemployment;

- the employee’s average earnings for two calendar years are below the minimum wage;

- The employee has a total length of service of less than six months.

The calculation of the final benefit to the employee based on the sick leave provided is calculated for all days of illness using a formula.

Formula for calculating sick leave benefits.

Sick leave benefit = Salary for two calendar years in rubles. : 730 days x Percentage based on length of service (100%; 80%; 60%) x Days on sick leave

You can calculate using a special formula

Differences in calculations may arise in the event of disability associated with a work injury or resulting from an accident, as well as pregnancy and childbirth. The final calculation includes 100% regardless of the insurance period.

The employee must provide salary data if he has previously worked for another organization for two years.

The calculator below will help you calculate the amount of sick leave benefits.

Go to calculations

Example. Let's calculate the benefit amount for the option already discussed above.

The employee went on sick leave from May 15, 2021 to May 25, 2020:

- the total salary for 2021 was 478,800 rubles;

- the total salary for 2021 was 653,000 rubles;

- total work experience will be = 6 years + 7 months, based on 80%;

- days on sick leave – 11.

Let's make the calculation:

| Sick leave benefit | = | Salary for two calendar years in rubles. | : | 730 days | X | Interest based on length of service 0.8 | X | Days on sick leave |

| 4843.61 | = | 478800 + 653000=1131800 Less than 1590000 | : | 550.41 | X | 440.33 | X | 11 |

The amount of sick leave benefits depends on the length of service

Are sick leave included in the payroll?

Remuneration is a mandatory remuneration that a person receives for carrying out labor activities at an enterprise.

Payroll – Payroll Fund, it represents all the amounts that employees of an enterprise receive in the course of their activities. With the help of payroll, expenses are kept track of for a certain time period. It includes expenses for staff salaries, as well as allowances, vacation pay and all types of social benefits.

Payroll calculation is carried out taking into account a certain time period, for example, a month or a quarter. At the legislative level, a minimum level of payment is established, and the maximum is not limited and depends only on the employee himself.

The payroll changes depending on the situation in the services market, the level of inflation, labor costs and other factors.

Examples of calculations

Example. Calculation of sick leave benefits according to the minimum wage

Employee Petrov A.A. works on the basis of Salut LLC for workers, brought a sick leave note, which noted the days of illness from February 15 to February 24, 2021. He returned to work on February 25, 2021.

On the basis of Salyut LLC Petrov A.A. He has been working since July 2021, and his earnings amounted to 182,000 rubles; he did not provide information about earnings from his previous place of work. The total insurance period is 10 years; a regional premium of 20% applies in the region.

Calculation of benefits for sick leave.

| Sick leave benefit | = | Salary for two calendar years in rubles. | : | 730 days | X | Interest based on length of service (100%) + 20% R.C. | X | Days on sick leave |

| 4 450,20 | = | 162000 Less than 1590000 | : | 221.92 Less than 370.85 according to the minimum wage | X | 445.02 = 370.85x100%x20% | X | 10 |

In some cases, the minimum wage is taken into account when calculating

For the first three days, Petrov A.A. The employer pays sick leave benefits - 1335.06 rubles, and the remaining funds are paid from the Social Insurance Fund.

Example. Calculation of sick leave benefits when the limit on the maximum base is exceeded.

Lopatina N.N. works on the basis of Salut LLC as a warehouse manager, brought a sick leave note, which noted the days of illness from February 19 to February 24, 2021. She returned to work on February 25, 2021. The total insurance period is 6 years; the regional supplement does not apply in the region. In 2021 Lopatina N.N. had a total earnings of 856,000 rubles, in 2021 the total earnings amounted to 916,000 rubles.

Calculation of sick leave benefits when the limit on the maximum base is exceeded.

| Sick leave benefit in rubles. | = | Salary for two calendar years in rubles. | : | 730 days | X | Interest based on length of service + 20% R.C. 0.8 | X | Days on sick leave |

| 10,323.26 rubles (2150.68 x 6 days x 80%). | = | 856000+916000 = 1772000 Over limit 1590000 | : | 2,150.68 per limit | X | RUB 10,323.26 = 2150.68 x 80% | X | 6 |

For the first three days Lopatina N.N. The employer pays sick leave benefits in the amount of 6,452.04 rubles, and the remaining funds for three days are paid in the amount of 6,452.04 rubles.

If the amount obtained is greater than the limit, then the maximum possible amount according to the limit is paid

Example. Calculation of sick leave benefits for an employee caring for a child under 7 years old.

Features of the calculation in this case:

- the child is under 7 years old, the employee is paid one sick leave benefit for the entire period of illness;

- the total number of days on sick leave in the current year cannot exceed 60 days.

Kazakova A.M. works at Salut LLC as a merchandiser, brought a sick leave certificate for caring for a 5-year-old child, which noted the days of illness from January 15 to January 24, 2021 - 10 days. She returned to work on January 25, 2021. The total insurance period is 6 years; the regional supplement does not apply in the region. In 2021 Lopatina N.N. had a total earnings of 406,000 rubles, in 2021 the total earnings amounted to 502,000 rubles, which does not exceed the limit base for these years - 1,590,000 rubles.

Calculation of sick leave benefits for caring for a child under 7 years old.

| Sick leave benefit in rubles. | = | Salary for two calendar years in rubles. | : | 730 days | X | Interest based on length of service 80% | X | Days on sick leave |

| 9950.72 (1243.84 x 80% x 10). | = | 406000+ 502000=908000 Less than the limit 1590000 | : | 1243.84 | X | 995,072. = 1243.84 x 80% | X | 10 |

Personal income tax in the amount of 13% is deducted from the calculated benefit amount - 9950.72 x 13% = 1294 rubles.

It is important to remember that the amount in hand will be less due to the deduction of personal income tax

As a result, it turns out that Kazakova A.M. child care will be paid for all 10 days of sick leave benefits. Its amount will be 9950.72-1294=8656.72 rubles, these funds are paid in full by the Social Insurance Fund.

Example. Calculation of sick leave benefits for an employee during pregnancy and childbirth.

Features of the calculation in this case:

- when calculating maternity benefits, the government has approved maximum payment amounts for 2021: minimum - 51,919 rubles, maximum - 301,095.20 rubles;

- the total duration of issuing sick leave is determined: maternity leave for the duration of pregnancy and childbirth with complications is at least 156 days, maternity leave for the birth of two or more children is 194 days;

- Personal income tax is not withheld from maternity payments for pregnancy and childbirth;

- All maternity benefits are paid at the expense of the Social Insurance Fund.

Antonova I.T. The secretary at the Salut LLC base provided the management with a sick leave certificate issued by the Women's Consultation for the period of pregnancy and childbirth for a period of 140 days. Her total salary for 2021 was 174,000 rubles, and for 2021 - 196,000 rubles. The amount for two years turned out to be (174,000 + 196,000) = 370,000 rubles.

To determine average earnings, divide the amount for two years by 370 days a year - 370,000/730 = 506.85 rubles.

Sick leave according to BiR is paid in full - personal income tax is not withheld

A manual for Antonova I.T. for pregnancy and childbirth for 140 days will be 506.85x140 = 70959 rubles.

Example. Calculation of sick leave benefits for an employee with less than 6 months of service.

Features of the calculation in this case:

- for a full month, the amount of the estimated salary does not exceed the payment according to the established minimum wage;

- the average salary will be the minimum wage for the number of days in a month of paid sick leave.

Commodity expert Ivanova M.M. has only 3 months of work experience at Salut LLC. She provided a sick leave sheet, which noted the days of illness from January 15 to January 24, 2021 - 10 days. She returned to work on January 25, 2021. Ivanova started working in November 2019.

Considering that the employee has less than 6 months of work experience, earnings in the amount of the minimum wage are taken into account - 11,280 rubles. Divide by 31 days in January: 11280/31 = 363.87 rubles.

If the work experience is less than 6 months, the minimum wage is taken into account

The amount for 10 days of sick leave benefits is calculated taking into account the coefficient for length of service: 60%. And it will be 363.87x10x60% = 2183.22 rubles.

Taking into account personal income tax, 13% accrual to Ivanova M.M. will be 2183.22 x 13% = 1899.22 rubles

For the first three days Ivanova M.M. The employer pays sick leave benefits in the amount of 3x363.87x60% = 654.97 rubles, and the remaining funds for seven days: 7x363.87x60% = 1528.25 rubles, are paid at the expense of the Social Insurance Fund.

Example. Calculation of sick leave benefits for an employee in case of non-compliance with the treatment regimen.

Features of the calculation in this case:

- the employer conducts an investigation into the reasons for the note on the sick leave about the employee’s non-compliance with the treatment regimen established for medical institutions;

- if it is determined that the employee had valid reasons for the violations, he is paid sick leave benefits on a general basis.

- if it is determined that there are no compelling reasons and the employee violated the sick leave regime unreasonably, the first part of the benefit, before the violation is noted, is paid on a general basis, and the second part after the noted day of violation is paid in accordance with the established minimum wage.

If the treatment regimen has been violated, the amount of sick leave benefits will be less

Commodity expert Suslova M.M. has 9 years of work experience at Salut LLC. She provided a sick leave sheet, which noted the days of illness from January 15 to January 24, 2021 - 10 days; she returned to work on January 25, 2021. The doctor made a note on the sick leave that the treatment regimen was violated. On January 23, the patient did not show up at the appointed time to see the therapist without a good reason.

The employee’s salary for the previous two years was 239,000 rubles. in 2021 and 186,000 rubles. in 2021. The amount was (239,000 + 186,000) = 425,000 rubles, which is less than the limit base.

The average earnings for one day are: (239000+186000): 730 = 582.19 rubles, where 730 are billing days for two years.

Payment of sick leave benefits is divided into two calculations: 8 days before the fact of violation of the treatment regimen and 2 days after.

In case of violation of the treatment regimen, payment is divided into two parts

Calculation of sick leave benefits for non-compliance with treatment regimen.

| Sick leave benefit in rubles. | = | Salary for two calendar years in rubles. | : | 730 days | X | Interest based on length of service 100% | X | Days on sick leave |

| 4657.52 = 8 x 582.19 | = | 239000+186000= 196000 Less than the limit 1590000 | : | 582.19 | X | 582.19 | X | 8 |

| 741.7 = 2 x 370.85 | = | 11280 minimum wage | : | 370.85 | X | 370.85 | X | 2 |

The total sick leave payment as a result of addition will be 4657.52 +741.7 = 5399.22 rubles. From this amount, personal income tax is deducted 13% = 701.9, and in total the following will be paid: 5399.22 - 701.9 = 4697.32 rubles.

For the first three days Suslova M.M. The employer pays sick leave benefits 3x582.19 = 1746.57 rubles, and the remaining funds for seven days are paid 5399.22 - 1746.57 = 3650.65 rubles at the expense of the Social Insurance Fund.

Part of the money is paid by the employer, part by the Social Insurance Fund

How is sick leave benefit calculated for child care?

Sick leave issued to parents to care for a child is paid entirely from the Social Insurance Fund.

Sick leave received by a parent during his next vacation is not paid, and the vacation is not extended.

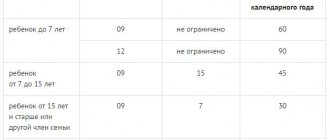

A child under 7 years of age is entitled to sick pay for up to 60 calendar days for the entire current year.

A parent has the right to take sick leave if a child is ill

For a child aged 7 to 15 years, parents are paid sick leave for each disease for up to 15 days, but not more than a total of 45 days per calendar year.

For children over 15 years of age, 7 calendar days are paid for each illness, but not more than 30 days per year.

Note! Every parent has the right to sick leave to care for a child, and payment is provided in the same way for each.

For a family with two or more children, the calculation rules apply separately for each child.

If there is more than one child in a family, the calculation rules apply to each

The amount of the benefit depends on where the child is treated:

- for outpatient treatment (the child is at home), the first 10 calendar days are paid to the parent in full, and for all subsequent days - 50% of earnings;

- When caring for a sick child in a hospital, the parent is paid the full sick leave benefit.

If a child becomes seriously ill, the duration and number of sick leaves is not limited.

So, sick leave can be paid in different ways: it all depends on how long the employee has, how long he was on sick leave and for what reason. In the article, we provided examples of various calculation options that should help you calculate the amount of unemployment benefits.

How are employee benefits calculated?

The amount of payment will depend on the number of years of employment:

- Full payment of sick leave requires at least 8 years of insurance coverage;

- compensation in the amount of 80% is assigned to workers with work experience from 5 to 8 years;

- Those working for 5 years are entitled to compensation of 60% of their earnings.

If a citizen has no earnings for the last two years, he will be accrued according to the minimum wage. All calculations must be carried out within 10 days after the certificate of incapacity for work is provided.

Money for sick leave is paid along with the next salary. The Social Insurance Fund reimburses the organization for expenses, with the exception of the first three days when it comes to disability due to injury or illness. Compensation for other cases is carried out using FSS funds from the first day.

The law provides for deprivation (partial compensation) of benefits for citizens who:

- violation of the treatment regimen (hospital, outpatient);

- missing a doctor's examination.

Payments stop starting from the day the violation was recorded.

In accounting practice, accruals and calculations for days of incapacity for work are carried out similarly to wage transactions.