Is personal income tax withheld and paid on sick leave?

The answer to the question of whether sick leave is subject to personal income tax is contained in paragraph 1 of Art.

217 Tax Code of the Russian Federation. Temporary disability benefits are excluded from the list of payments not subject to personal income tax. Since the document confirming the employee’s incapacity for work is a certificate of incapacity for work, personal income tax is calculated from the sick leave. Let us recall payments that are not subject to personal income tax (Clause 1, Article 217 of the Tax Code of the Russian Federation):

- lump sum maternity benefit;

- monthly allowance for child care up to 1.5 years;

- monthly compensation for child care up to 3 years old.

A ready-made solution from ConsultantPlus will help you calculate and pay sick leave to employees, including in unusual and difficult situations. Get trial access to the K+ system and immediately see expert recommendations. It's free.

Personnel accounting and payroll calculation in 1C 8

Hello dear zup1c visitors. In today’s article we will talk about one of the most frequently asked questions on the topic of applying deductions and calculating personal income tax in 1c ZUP 8.3 in relation to the preparation of 6-personal income tax. The question of today's publication boils down to the following: why is the deduction doubled when calculating personal income tax in the Hospital (in inter-account accrual) ? I will try to explain with a specific example what the reason is, whether it is right or wrong, and I will also analyze how this affects filling out section 2 of the 6-NDFL form .

It turns out the following: at the time of accrual of sick leave, we still do not have a single taxable accrual for June , because The salary for April has not yet been accrued, nor for July . Therefore, the program applies the deduction for 2 months at once : for June - it has not yet been applied, and for July - since the payment occurs on July 10.

We recommend reading: If You Were Not Given A Place In Kindergarten At 3 Years Old

Is income tax taken from sick leave in 2020-2021 or not?

Are sick leave subject to personal income tax? Yes, and the personal income tax rate for this type of payment has not changed: in 2020-2021, as before, it is 13%.

Since sick leave is subject to personal income tax, the tax base for calculation is the amount of temporary disability benefits in full (letter of the Ministry of Finance of Russia dated June 17, 2009 No. 03-04-06-01/139).

Important! Starting from 2021, the employer accrues and pays sick leave only for the first 3 days and only pays personal income tax from this amount. The remaining portion of the benefit is paid directly to the employee by the Social Insurance Fund. He also withholds personal income tax from her. In cases where the FSS issues 100% of the benefit, it withholds tax from the entire amount. For more details, see our memo on the new rules for paying benefits from 2021.

Accountants sometimes have doubts whether to withhold personal income tax from sick leave as when assessing wages, or are there differences? Please note that deductions here are carried out in a special manner, different from deductions from an employee’s salary.

The difference is that sick pay is included in taxable income in the month of payment (clause 1 of Article 223 of the Tax Code of the Russian Federation). There are also differences in the procedure for paying personal income tax from sick leave to the budget. But more on that below.

In business practice, there are circumstances in which employees working at the enterprise fell ill after concluding civil contracts with them. A reasonable question arose: is personal income tax paid on sick leave for such employees? It should be borne in mind that employees with whom civil contracts have been concluded should not be paid sick leave. Accordingly, there is no need to accrue or pay personal income tax.

Is tax paid for sick leave paid from the Social Insurance Fund?

If a specific region of the Russian Federation participates in the official FSS pilot project (Order of the FSS of the Russian Federation No. 578 of November 24, 2021), then the following rule is applied: the first three days of illness are paid from the fund of a specific enterprise, and all the rest - from the FSS.

Personal income tax is withheld in both the first and second cases. Read also: Sale of an LLC with debts

Sick leave is paid for at the expense of a specific amount of funds from the Social Insurance Fund already in the first days in the following situations:

- when caring for a child;

- in the event of a specific accident at work;

- during prosthetics in a hospital;

- in the event of an occupational disease;

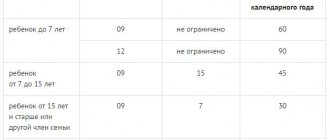

- when the employee himself, or 1 or several of his children under 7 years old who go to kindergarten, etc., go into quarantine.

Regardless of the validity period of a specific certificate of incapacity for work, only the employer - a specific company - is considered a tax agent when paying personal income tax. Personal income tax is withheld and transferred to the Federal Tax Service of the Russian Federation from the entire amount of benefits under this medical certificate.

Order of the Federal Insurance Service of the Russian Federation dated November 24, 2017 N 578 “On approval of the forms of documents used for the payment of insurance coverage and other payments in 2012 - 2021 in the constituent entities of the Russian Federation participating in the implementation of a pilot project providing for the appointment and payment of compulsory social insurance coverage to insured persons insurance in case of temporary disability and in connection with maternity and for compulsory social insurance against accidents at work and occupational diseases, other payments and expenses by the territorial bodies of the Social Insurance Fund of the Russian Federation"

What period and date of personal income tax withholding are established for sick leave and vacation pay?

The deadline for paying sick leave tax is no later than the last day of the month in which the benefit was paid.

The withheld personal income tax must be shown in the 6-NDFL report. ConsultantPlus experts explained how to determine the date of actual receipt of sick leave income for calculating 6-NDFL. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

By the way, a similar procedure and payment deadline is provided for personal income tax on vacation pay: the tax should be withheld and transferred to the budget no later than the last day of the month when the vacation pay was issued.

About the deadline for paying personal income tax

Temporary disability benefit – personal income tax and additional payment up to average earnings

If, when calculating temporary disability benefits, an additional payment is made up to average earnings, then the corresponding personal income tax on sick leave is paid in the general manner (Articles 217, 226 of the Tax Code of the Russian Federation). Both officials and judges came to this conclusion (letters from the Ministry of Finance of Russia dated 05/06/2009 No. 03-03-06/1/299, dated 02/12/2009 No. 03-03-06/1/60, dated 12/24/2008 No. 03- 03-06/1/720, resolution of the Federal Antimonopoly Service of the North-Western District dated 07.07.2008 No. A26-2542/2007).

Thus, to the question posed at the beginning of the article, whether personal income tax is withheld from sick leave, the answer will be unequivocal: undoubtedly, yes.

Personal income tax for sick leave (deduction for a child if the employee was on sick leave for three months

At the same time, the Federal Tax Service indicates that if the employment relationship is not interrupted and if in certain months of the tax period the employer did not pay the taxpayer income subject to personal income tax, then in its opinion, standard tax deductions are provided for each month of the tax period, including those months in which there were no income payments. To substantiate their conclusion, tax authorities refer to Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 14, 2009 No. 4431/09, which confirmed the right to a deduction for a resident employee even in those months in which he did not have income subject to personal income tax at a rate of 13 percent. Deductions for these months are accumulated and summed up with the deduction that the employee is entitled to for the month in which he again began to receive such income. Similar explanations were given by financiers (see letters from the Ministry of Finance of Russia dated October 22, 2014 No. 03-04-06/53186, dated May 6, 2013 No. 03-04-06/15669, dated February 6, 2013 No. 03-04-06/8-36 , dated January 13, 2012 No. 03-04-05/8-10).

Glavbukh_Elena, I quote the Letter you provided: Thus, the standard tax deductions established by subparagraph 4 of paragraph 1 of Article 218 of the Code are provided by the tax agent to the taxpayer for each month of the tax period by reducing the tax base in each month of the tax period by the corresponding established amount of the tax deduction.

We recommend reading: Scholarship for First-Year Secondary Students

Results

Payment for sick leave, with the exception of maternity benefits, is subject to personal income tax, regardless of the source of its payment (employer or Social Insurance Fund).

The employer's personal income tax on sick leave benefits must be withheld upon payment and transferred to the budget no later than the last day of the month in which the benefits were paid. When paying benefits for sick days, starting from the 4th day, the Social Insurance Fund will withhold and transfer it to the budget independently. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to show it in documentation?

The amounts of tax deductions applied in the calculation are reflected in section 4 of the 2-NDFL certificate and section 1 of the calculation in form 6-NDFL.

- In the 2-NDFL certificate in the table of section 4, the code of the deduction received and its amount are indicated in the appropriate columns. For standard deductions for children, codes 114-125 are provided, depending on the basis for their use; several codes can be used simultaneously.

- In form 6-NDFL, only the amounts of applied deductions are indicated in field 030.

If symptoms of the disease are detected, there is no need to delay contacting the clinic, since the doctor will not issue a certificate of incapacity for work for the past period and you will not be able to receive sick leave to care for your children. Read our articles about how to issue such a ballot, in what cases it is issued and whether the father, grandmother or grandfather can take it, as well as whether sick leave is due during vacation, quarantine in a kindergarten or school, after dismissal and how it is paid.

The correct calculation of disability benefits associated with child care, taxes and insurance premiums levied on it, and timely submission of reporting are necessary primarily for the employer. This will allow timely reimbursement of benefits paid to the employee and avoid additional attention from regulatory authorities.

If you find an error, please select a piece of text and press Ctrl+Enter.