Sberbank mortgages on the secondary market are a tangible help in purchasing home ownership for many citizens.

Purchasing a home is a difficult task for many families, especially young ones. Due to low incomes, the vast majority are unable to purchase housing immediately. Therefore, people often have to pay rent for a rented apartment, and this pushes the dream of owning their own living space even further away.

A mortgage loan makes it possible to acquire your own living space, while you have to pay a monthly amount that is almost identical to the rent for someone else’s square meters. Therefore, the popularity of mortgages is only increasing every year. In addition, the conditions for obtaining it are constantly being simplified and, thanks to various government programs, overpayments are being reduced.

Rates and conditions

Before submitting an application, it is recommended to find out what percentage Sberbank has for a mortgage for secondary housing. The initial interest rate at Sberbank for mortgage products today is 9.5% per annum. The interest rate for loans falling under the share of young families is set at 9.1%.

There are additional additions to these basic sizes:

- + 0.3% if the apartment was not selected by the Domclick.ru service.

- + 0.2% if the down payment ranged from 15% to 19.99% of the total loan volume.

- + 0.5% for salary recipients not through Sberbank.

- + 0.8% if proof of regular income and permanent employment was not provided.

- + 1% for refusing health and life insurance through Sberbank.

Sberbank's base mortgage rate for secondary housing for participants in regional and federal mortgage programs will be 9.3%. The surcharge for a small down payment (up to 20%) will be charged at the rate of 0.2%; for refusal of insurance, 1% will be added.

Interest surcharges

When calculating the interest rate on a Sberbank mortgage, both basic values and individual characteristics of the client are taken into account: his solvency, the size of the down payment, time for payment, etc. In addition, the organization has provided some allowances:

- 1% – if the borrower refuses personal insurance;

- 0.8% – if the borrower does not receive his salary into a bank account;

- 0.3% – if the borrower cannot confirm his income and official employment;

- 0.1% – if the borrower refuses to register electronically.

The bank also cooperates with some municipalities and entire regions. Such programs provide a fixed rate on Sberbank mortgages, which currently amounts to 9% per annum.

Even more attractive conditions can be found with developers cooperating with the bank. The list of programs with reduced mortgage rates in Sberbank is currently posted on the official website.

Requirements for the borrower

Sberbank's conditions for potential borrowers depend on the volume of funds requested, the duration of the loan agreement, the presence or absence of collateral and a guarantee under the agreement ().

An adult citizen over 21 years of age can take out a mortgage from Sberbank for a secondary home. The maximum age of the borrower at the time of full repayment of the debt should be no more than 75 years. This maximum applies to all borrowers and co-borrowers; based on a specific decision made, the age can be adjusted.

The applicant must have a total working experience of at least six months at his current job and he could not have worked for no more than four years out of the last five. For clients who receive earned funds through Sberbank, these conditions are not relevant, since all the necessary data is already available in bank information databases.

The length of continuous work experience indicates the solvency and reliability of the borrower.

Important conditions for a Sberbank mortgage for secondary housing when deciding to issue a loan are the client’s solvency and credit history. To check solvency, the following are studied:

- salary certificates();

- availability of property;

- trips abroad;

- relatives' wealth.

Credit history is affected by arrears on previous loans, the presence of unpaid obligations at the moment (total monthly payments), the presence of already repaid mortgages or car loans, and the frequency of applying for ordinary small loans.

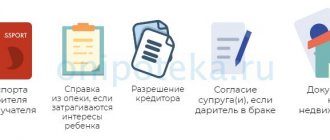

The client's spouse is a co-borrower without fail (ground - and). This requirement does not apply only if there is a marriage contract concluded between them (), where the other half is not a possible potential owner. Another reason for refusing a spouse to be a co-borrower is the lack of Russian citizenship.

No more than three capable citizens of the Russian Federation can be co-borrowers of the loan. Their combined income affects the maximum loan amount issued.

Interest reduction options

In reducing the possible overpayment on a mortgage at Sberbank, some conditions can play a significant role:

- mortgage for secondary housing in Dom Click from Sberbank;

- receiving earnings through this bank;

- life insurance offered by the lender;

- apartment registration through Sberbank;

- eligibility for benefits under the program for young families.

What is the down payment for a mortgage at Sberbank for all programs?

In order to reduce potential risks, many banks in Russia have refused to issue mortgage loans without a down payment. Sberbank was no exception here. You can get a mortgage in it only if you pay a set share of the cost of the purchased property.

Information on how much the down payment on a mortgage at Sberbank is in the context of all existing programs is presented in the summary table below.

IMPORTANT! For borrowers who have not confirmed their solvency and employment with documents, the minimum contribution cannot be less than 50%.

It is also important to understand that some mortgage programs have their own characteristics regarding the payment of mandatory payments. For example, a military mortgage requires a down payment of 15 percent. But it is paid not from the serviceman’s own savings, but by transferring funds from the state budget accumulated in his personal account for 3 years.

The “Mortgage + Maternal Capital” program also requires a contribution of at least 10%, which means state aid funds that can be used to pay part of the cost of the purchased housing.

The maximum first payment is typical for loans, the purpose of which is the purchase/construction of non-standard objects - houses/townhouses and a garage or parking space.

Necessary documents for a Sberbank secondary mortgage

When applying to this bank for a housing loan, you must submit the prescribed list of documents.

If income from employment is not planned to be confirmed, then the established form is drawn up and the applicant’s passport is presented. The second required document may be a driver’s license, a military service member’s or law enforcement officer’s ID, an international passport or SNILS. Sberbank's mortgage for secondary housing for salary clients does not oblige them to confirm income and place of work.

Recommended article: Mortgage for employees of the Russian Guard

When confirming the details of the work and payment for it, a different one is presented. It includes:

- application in the form of a survey;

- Russian passport with permanent registration on the territory of the Russian Federation (or other proof of registration);

- certificates from the accounting department from the place of work ().

When applying for a secured loan, you will additionally have to submit documents describing the collateral property, proving the applicant’s ownership of it and the absence of encumbrances.

Participants in a Sberbank mortgage for a young family for secondary housing additionally submit a document confirming marriage and the birth of a child, documents confirming their relationship with the other co-borrowers (if necessary).

When Sberbank mortgages on the secondary market with the involvement of maternity capital finance, documentation is additionally required about its availability and the remaining limit on it.

Co-borrowers and guarantors are required to submit a similar list of documents for a secondary mortgage with Sberbank, without exceptions. Thanks to the bank's resolution, the contents of the package of documents can be changed.

Is it possible to get a mortgage without a down payment?

As of today, Sberbank does not offer mortgages without a down payment. However, there are several working schemes with which you can purchase an apartment without providing initial capital. The first way is to apply for a cash loan for a large amount secured by a car or real estate owned by the client. You can provide guarantors and also receive cash on credit to purchase a home. The second way is to inflate the market value of the property by the amount of the down payment (by 10% -20%). The borrower will not need to contribute his own funds, since the bank will finance him for the full cost of the property. This method can only be used after a personal agreement between the buyer and the seller. The seller must write a receipt confirming receipt of the down payment and provide it to the bank.

Design nuances and possible risks

Inflating the cost of housing in order to avoid paying a down payment is used when purchasing real estate on the secondary market. In this case, the apartment or house must be owned by the seller for more than 3 years. In the case of purchasing real estate in a new building, there are many more nuances with the down payment. The advantage is that no assessment is required. But, on the other hand, the developer needs to register the first payment in accounting.

Using maternity capital as a contribution

Maternity capital funds can be used to pay the down payment on a mortgage. If a family wants to increase the size of its existing living space, then it will have to prove this need with documents. If you don’t have your own home, buying an apartment with a mortgage with maternity capital will be much easier. Military citizens can get a preferential mortgage from Sberbank. The state pays the first installment for them. When deciding to purchase real estate with a mortgage, rely on your income and financial capabilities. If you want to calculate your mortgage parameters, contact employees at any Sberbank branch. You will receive qualified assistance there.

Secondary housing upon presentation of two documents

This offer is suitable for individuals who do not want to collect a lot of documents and can make a down payment of 50% of the entire mortgage amount.

Under the terms of this product, it can be used by a citizen of the Russian Federation who has funds for a Sberbank mortgage on a secondary home for an initial payment of 50% of the total volume (). The loan period is possible up to 30 years.

The percentage of mortgages for a secondary mortgage in Sberbank before this offer (from 8.4% to 10.1%) will depend on the method of processing the transaction: when registering through the MFC, the rate may be lowered, refusal of insurance will increase the interest rate.

For salary recipients through Sberbank, credit interest is reduced, as is the case when taking out comprehensive insurance.

To apply for this offer, you will need a Russian passport, a completed application in the form of a questionnaire, and a second document of the applicant’s choice. Among them may be:

- international passport;

- rights;

- military man;

- SNILS;

- document of a law enforcement officer.

To apply for a housing loan with a minimum of documents with collateral, you will need to additionally present.

Each application is considered individually, therefore the conditions for each specific product can be changed by the lender at its discretion.

Minimum down payment amount

To know how much personal savings a borrower should have when applying to Sberbank for a mortgage, you need to familiarize yourself with the terms of all existing mortgage lending programs and choose the one that is most suitable in a particular case. Today, Sberbank offers its clients a choice of only eight programs:

- mortgage with state support for families with children (a new mortgage program that the bank launched just this year);

- loan for the purchase of a finished apartment (purchase of a home on the secondary real estate market);

- promotion for the purchase of living space in new buildings (participation in shared construction, that is, the purchase of an apartment at the initial stages of construction of an apartment building);

- lending for the purchase of residential premises using maternity capital funds (maternity capital acts as a down payment or a certain part thereof);

- mortgage construction (loan to finance the independent construction of a residential building - a private house, cottage, etc.);

- a loan for the purchase or independent construction of country houses (dacha and other buildings for consumer purposes);

- mortgage lending to military personnel (including retired ones);

- non-target mortgage (loan issued on the security of real estate for various personal purposes).

Mortgage lending to families with children with state support

This is a new loan product that recently appeared among other Sberbank offers. Families in which a second or third child will be born between January 1, 2021 and December 31, 2022 can become its consumer. This lending program offers the lowest interest rates compared to other loan products - from 6%. The maximum loan amount can be 8 million rubles, and the term can be up to 30 years. Sberbank has set the minimum down payment for this mortgage program at 20% of the loan amount.

Purchasing secondary housing with a mortgage

Sberbank has been lending for the purchase of apartments on the secondary market for quite a long time, so the conditions of this program are much better and more profitable than in other banking institutions. The down payment for this loan product will be from 15%, and the minimum mortgage rate will be 8.6%, but this offer is valid exclusively within the terms of the program for young families and subject to online approval of the selected apartment on Sberbank’s partner website DomClick.

Promotion for the purchase of housing during the construction phase

This is one of the most profitable mortgage programs operating at Sberbank. The size of the down payment according to the terms of this loan product is from 15% at a rate of 7.4%. The most favorable conditions apply to those who receive government subsidies to improve their living conditions. But beneficiaries (subsidy recipients) can apply for a loan on special terms only for a period of up to 12 years, if longer, then on a general basis.

Purchasing a mortgaged apartment using funds from mother capital

Each family, when the second, third, fourth, etc. appears. the child has the right to receive maternity capital.

Important! According to Russian law, maternity capital can only be obtained once in a lifetime. Therefore, if a family has already applied for this state assistance once, then it will not be able to receive it again.

The minimum down payment under this program is 15% of the cost of the purchased residential property. Maternity capital can be used as payment for the down payment or some part of it, if the amount of maternity capital is not enough to make the first payment. If the amount of state financial assistance exceeds 15%, you can contribute more, thereby reducing the loan amount and its total cost.

Loan for the construction of a private residential building

Living in a private house has many advantages compared to a city apartment, which is why citizens often prefer this type of housing. But finding and buying a ready-made house with the optimal layout and all the necessary amenities is very problematic. Therefore, building a house from scratch according to your own design is a wise decision in this situation. Sberbank provides loans for the construction of residential buildings on special terms. The down payment on a mortgage under this program cannot be less than 25% of the construction cost, since in this case the risks are much more significant both for the bank and for the borrower himself.

Purchasing a country house with a mortgage

For those who are planning to buy a summer house or build a garden house on their own, Sberbank offers a special loan program “Country Real Estate”. According to the terms of this mortgage, as in the case of a mortgage for the construction of a private house, the down payment must be at least 25% of the value of the real estate. If the contribution is less than this amount, the bank will refuse to issue a loan.

Mortgage loans for military personnel

Military personnel are a separate category of citizens for whom Sberbank has developed a special loan product - “Military Mortgage”, which is provided to them under special conditions. According to the terms of this program, military personnel can borrow up to 2.33 million rubles for a period of up to 20 years at an interest rate of 9.6%. The minimum down payment is 15%. This is enough to confirm the borrower's solvency. The bank does not require any other forms of confirmation from the client.

Important! Sberbank practices issuing mortgages to clients who have not documented their solvency, as well as to those who do not have a very exemplary credit history. But for these categories of borrowers, the down payment amount is set at 50% of the cost of the purchased property or more.

Mortgage without down payment

Not everyone can take advantage of this offer from Sberbank. This opportunity is available to several categories of applicants:

- participants of various federal programs;

- those on a waiting list for free housing;

- military personnel participating in a special program;

- individuals who contribute maternity capital funds as mortgage payment;

- clients included in the program to help young families;

- borrowers wishing to refinance the balance of the loan with another bank.

Taking out a mortgage without a down payment for a secondary home from Sberbank is available only to Russian citizens who have a systematic income of at least average. Its confirmation is the most important point when planning a mortgage without a down payment.

Monthly earnings are preferably 50%-60% higher than the expected monthly mortgage payment. In this case, the bank is more loyal to clients who receive salaries here and to participants in federal programs.

Important to know: Where is it more profitable to get a mortgage without a down payment?

Maternity capital as a down payment on a mortgage

Down payment on a Sberbank mortgage. What it is

Almost all citizens of the Russian Federation who, at least once in their life, have applied for borrowed funds in the described banking structure know that in order for you to be given a large loan to buy a car or an apartment, you will need to deposit your money in the form of an initial payment.

It is necessary to understand that the reason for the need to make the described contribution is that before transferring a large amount of funds to the borrower, the banking structure needs to make sure that the client has a sufficient level of income to repay the loan on time. In such a situation, it is the initial payment that is a kind of indicator of the client’s solvency.

The size of the initial payment can be quite different. First of all, the size of the payment depends on what kind of loan you plan to get, as well as on the policy pursued by the banking structure. According to available statistics, most often the required initial payment is in the range of ten to thirty percent of the amount of borrowed funds that you plan to receive. Thus, the larger the amount of borrowed funds you plan to borrow, the more money you will need to pay for the down payment.

Stages of obtaining a mortgage from Sberbank for secondary use

The first step is to choose the type of mortgage loan that is suitable for a particular borrower. First you need to decide on the required amount, term and possible interest. It is recommended to study all possible mortgage offers from Sberbank and choose the most suitable one. Find out information about possible preferential programs, bonuses and penalties.

To apply for a home loan, you can fill out, or contact the institution’s office. In the bank department, the credit manager will answer all your questions, introduce you to offers that are suitable for a particular client, announce the mortgage rates for secondary housing in Sberbank, advise the best option and help you fill out an application. The application is reviewed within 1-5 business days.

It is very important to take into account that after preliminary approval of the loan, upon subsequent examination of the submitted documents, the bank may change its decision. Therefore, the next stage is more important than submitting an application.

Following the approval of your application for a mortgage loan, you need to go through several more stages of obtaining a secondary mortgage from Sberbank before finally receiving the loan amount. If housing has not yet been finally chosen, then this must be done first. Since the preliminary decision is only valid for three months, you will have to hurry.

We recommend that you read : The procedure for obtaining a mortgage for the purchase of an apartment on the secondary market

Buying a secondary apartment with a mortgage: step-by-step instructions

For the bank to approve the client’s choice, the housing must meet all the lender’s requirements. Therefore, it is better to first familiarize yourself with the conditions and choose an apartment as a secondary home with a Sberbank mortgage in accordance with them. The conditions for the purchased housing are as follows:

- The house should not be in disrepair, no more than 50 years old (for the capital) and 65 years old (for the province), with a degree of deterioration of up to 70% by the period of full repayment of the loan.

- Brick, cement or stone foundation of the building, only metal or reinforced concrete floors.

- All building communication systems provided must be in working order.

The lender will carefully check the subject of purchase against all criteria. The purchased housing is pledged by law to the bank until the loan is fully repaid, so this collateral must be liquid in case the borrower fails to repay the loan.

A mandatory requirement of Sberbank will be an independent assessment of real estate by a specialist at the borrower’s expense.

Important to know: Real estate valuation for mortgage in Sberbank - list of accredited appraisers, price, terms, procedure

The general package of necessary documentation consists of three parts: real estate documents, the applicant’s package, and the seller’s package.

- For the purchased housing, the following must be presented: a certificate of ownership of the seller, where this right came from (purchase, donation, inheritance, privatization, technical passport for the premises, evidence of absence of rent arrears, information about registered residents, appraisal certificate.

- Personal documents of the seller: Russian passport, consent of other owners and spouses (if necessary), permission from the guardianship authority (if there are minors in the transaction).

- Buyer's documents: passport, personal documents of other potential owners (if any), confirmation of the availability of the required amount for the down payment, consent to purchase from the spouse.

If the bank approves all submitted documents:

- sign a mortgage (loan) agreement;

- pay a down payment;

- sign and submit for registration documents for the purchase of real estate.

Important to know: How to confirm a down payment on a mortgage

Mortgage loan agreement: what to look for when signing

Purchase and sale agreement with a mortgage - important points for the seller and buyer

How does a mortgage transaction work - frequently asked questions

The entire amount of the cost of the apartment is transferred to the seller within 5 days from the moment the sale agreement is signed. A mandatory clause stated in the mortgage agreement is insurance of the purchased living space.

Step-by-step instructions on how to get a mortgage from Sberbank

The lender pays special attention to explaining each stage of the transaction. The terms of the loan are described in detail on the pages of the official website, and the assigned branch manager is required to provide complete information about the process of concluding a mortgage transaction.

Step 1 - choosing a mortgage program

You can take out a mortgage from Sberbank for an apartment or residential building. Whatever program the client chooses, the mortgage transaction should begin by choosing the optimal program option, paying special attention to the possibility of applying benefits or subsidies from the state. Even a half percent discount offered by Sberbank on mortgages results in tens and hundreds of thousands of rubles in savings.

You can reduce the overpayment by 1.0% if, before applying for a loan, you work for at least six months with an employer who pays wages to a Sberbank card.

If you intend to buy a comfortable apartment, it is better to study the offers of developers and objects on the Dom.Click website. This will help you get a discount of 0.3%, and the lowest rates apply to new buildings.

Step 2 - collecting the necessary documents

During the loan approval process, 3 packages of documentation must be prepared:

- For initial approval of the application. A minimum of documents is required - a passport of a citizen of the Russian Federation, a completed application form, and a salary certificate. Additionally, the bank may request SNILS, INN, and marriage certificate. The employer may be required to provide a certified copy of the work record. If you have children, prepare copies of birth certificates.

- After the loan is approved, documents for the transaction are prepared, selecting an object according to the required parameters. Most of the documents are prepared by the seller: technical passport, cadastral passport, USRN extract. Additionally, they prepare a certificate about the residents registered in the living space (an extract from the house register) and papers confirming the absence of debts for housing and communal services. The bank will check the liquidity of the property, the degree of technical wear and tear, and the absence of encumbrances.

- At the final stage, the borrower prepares an independent expert’s opinion on the valuation of the property and takes out insurance.

When preparing documentation, you need to remember that some certificates have a limited validity period. For example, salary certificates and an extract from the house register are valid for no more than a month.

Step 3 - submit an application to the bank

To submit an application and receive approval for your application, you do not need to visit a bank office. Most transactions are carried out online by registered users of Sberbank Online. The request processing time directly depends on the selected program and method of request. For example, for users of the Dom.Click service, the review period is no more than 24 hours.

Step 4 - registration and signing of the contract

When all documents are prepared and the terms of the transaction are agreed upon, a transaction date is set. Along with the loan agreement, a pledge agreement is signed. On the eve of signing the contract, purchase an insurance policy and make a down payment. After signing the agreement, documents are submitted to register the transfer of ownership to Rosreestr.

Registration costs

When applying for a mortgage loan, you must take into account that money will be required not only as payment for the purchase to the seller, but also for other expenses.

- Independent assessment of purchased housing.

- State fees for services when registering real estate.

- Buyer's purchase and life insurance.

- Real estate services, if necessary. Is it worth getting a mortgage through realtors? The pros and cons are discussed in the next article.

- Registration of permits and certificates for an apartment will have to be done through Sberbank until the loan is repaid in full. All these services are also paid.

Online calculator: calculate a Sberbank mortgage for secondary housing

You can calculate a mortgage from Sberbank for secondary housing, like any other loan, on the website using an online calculator. It makes it possible to see all the parameters of a future loan before completing an application.

To calculate a Sberbank mortgage for secondary housing using a calculator, you need to go to the lending page and enter the selected parameters in the appropriate windows.

- Decide on the purpose of the mortgage.

- Indicate the price of the purchased property.

- Enter the amount of the possible down payment.

- Set the desired loan term.

- Select and enter additional loan terms.

- After filling out all the selected conditions and checking the entered data, click - Calculate mortgage.

After all the manipulations, Sberbank’s online mortgage calculator for secondary housing will display the results of preliminary calculations:

- minimum monthly payment;

- the total amount of payments for the entire period of using the loan;

- amount of overpayment;

- proposed percentage;

- the salary level required for the specified parameters.

Here you can clarify the documents required for collecting a mortgage.

How to apply to Sberbank for a mortgage for secondary housing

There are two ways to submit an application to take out a Sberbank mortgage for secondary housing. Submit an application online on the official website of the lender () or contact the office of a banking organization.

To apply for an online Sberbank mortgage for a secondary home, you need to go to the Sberbank website and follow the link Get a loan. Select the Housing Loan section, familiarize yourself with the lending programs presented on the page and choose the most suitable one.

After selecting a program, the link redirects the client to an online calculator . After all the calculations, the calculator takes the visitor to a page with a questionnaire - an application to Sberbank for a mortgage for secondary housing, which must be carefully filled out. The service automatically redirects the client to the Domklik website, where they can select options for further actions and finalize the mortgage application.

How Sberbank checks a secondary apartment with a mortgage

Sberbank, like all lenders working with mortgage offers, checks every piece of real estate presented for purchase. The purpose of this process is to confirm its declared value, to verify the accuracy of the data offered to the bank on the subject of purchasing a secondary home with a Sberbank mortgage.

It is important for a banking institution to be able to sell mortgaged property in the event of non-payment of the loan debt by the borrower. Therefore, the purity of the acquisition, the absence of encumbrances and the market value of the real estate purchased with his money are no less important aspects than the client’s solvency.

If we are talking about applying for a mortgage at Sberbank for secondary housing, then the banking service checks all the technical documentation of the building. They study the entire ownership history of the living space, documentation on previous sales or other reasons for changing owners, and the presence of hidden applicants for housing. The features of this check for a Sberbank mortgage on a house as a secondary home (or apartment) can be identified as follows:

- Determination of the degree of wear of the structure.

- Confirmation of the further use of the building (it is not planned for demolition and is not recognized as unsafe).

- The location of the object and the surrounding infrastructure are considered.

- The internal condition of the housing, room area, surface finish, and layout are studied.

- Availability and serviceability of utilities.

- Basements or ground floors of a building are usually not considered by the bank.

First, all documents submitted by the borrower for a Sberbank mortgage on secondary housing are checked. Then documents for this property are requested from the seller. The documents may be different; the bank independently decides on the required package. If all documents requested by the lender are not provided, or if there are suspicions of attempted fraud by either party, the bank will immediately refuse the mortgage.

When studying the documentation, the following is taken into account:

- Whether the apartment is free, the presence of registered strangers or children who have refused privatization is not allowed in it.

- Absence of any types of encumbrance.

- No debts on utility bills.

- It is unacceptable for one of the owners to be wanted.

- Has the six-month period expired in the event of the owner's death to prevent new claimants from appearing?

The verification period is not regulated by documents, so it can last as long as necessary for the credit institution to obtain confirmation of the purity of the future transaction. Most often, the entire process takes from a couple of days to several weeks.

on mortgage lending regulates the basic requirements that apply to collateral when purchased on the secondary market. Sberbank independently establishes requirements for purchased housing and is guided by the law on consumer rights.

Mortgage for individuals in Sberbank: rate, conditions

The interest rate is set in accordance with the purpose of the program. The most popular offer for the purchase of an apartment in a new building from Sberbank has an interest rate of 10.4%. This minimum percentage is explained by a new promotion that will be valid until the end of this year. For other programs the following minimum rates are established:

- purchase of finished housing – 10.25% (this minimum is relevant for young families);

- with maternal capital – 12.5%;

- for building a house - 12.25%;

- suburban real estate – 11.75%;

- military mortgage – 10.9%.

In practice, the average client can count on a mortgage from Sberbank at 14-15%. All applications are considered individually.

Interest rate for pensioners

Pensioners at Sberbank are not considered a category of persons who are granted benefits under mortgage offers. The very fact that this type of loan is provided to pensioners from this bank is already a certain benefit. In many other banking organizations it is not possible to get money for an apartment or before, as a pensioner. Therefore, a large number of pensioners can receive a loan at 10.4% or a higher percentage.

Sberbank’s main requirement for pensioners is that the client be no more than 75 years old at the end of the contract.

Registration procedure

According to the rules, Sberbank mortgages for individuals are issued at the place of registration of the borrower or at the location of the property. An individual can submit a preliminary application for a mortgage through his personal account or through the official website.

The application review period is 2-5 working days. During this time, the client will be called back and informed about the bank’s decision. If the answer is positive, the future borrower will come to the branch with the required package of documents. All that remains is to select a property, draw up a contract and start paying off the debt monthly.

You can also apply for a mortgage in person by filling out an application at the bank. The chances of a positive response are the same both during a personal visit and when registering via the Internet.

You can easily apply for a loan for any need by filling out the form at the bottom of the page.

List of documents

To apply for a mortgage at Sberbank for individuals, the following basic documents are needed:

- application in the form of a questionnaire;

- passport with registration;

- one more document to confirm your identity;

- documents on financial status and employment.

When issuing mortgages to individuals, Sberbank pays the greatest attention to a certificate of income. It is important that the person receives an amount sufficient to repay the debt and support the family. The time spent working in the last place is also taken into account. It must be at least six months.

How to apply for maternity capital?

The procedure for obtaining a mortgage at Sberbank for owners of maternity capital remains standard: a package of documentation is submitted, a property is selected, and an agreement is signed. The last stage is registration of the right to the object.

The main requirement for obtaining a mortgage against maternity capital at Sberbank is the presence of a state certificate of receipt of funds and a document stating that they have been deposited into the account. The latter is issued by the Pension Fund.

Conditions and interest rate for secondary housing

The conditions for the purchase of secondary housing for individuals and pensioners are as follows:

- debt repayment period – up to 30 years;

- amount provided – from 300 thousand rubles;

- interest rate – 10.75%.

The minimum interest rate for an apartment in an old building is relevant when submitting an application electronically. The base rate is set at 11.25% for individuals. Read more about the offer in the article:

Mortgage without down payment in Sberbank

The down payment is a confirmation for Sberbank of the solvency of an individual. Therefore, today there are no programs with a zero down payment. But instead of a contribution, you can use money from maternity capital. The same 450 thousand rubles provided by the state to families with 2 or more children will be enough to obtain a housing loan at minimal interest. The registration procedure and list of required documents will remain the same. You can find out more about the offer by following the link:

With state support

To consider the conditions for obtaining a mortgage with state support from Sberbank, let’s take as a specific example a family with a certificate for maternity capital. With a loan term of 5 years and an amount of 1.7 million rubles, the monthly payment will be slightly more than 39 thousand rubles. This payment is explained by the 13.5 percent rate, which is the average for mortgages with state support for individuals.