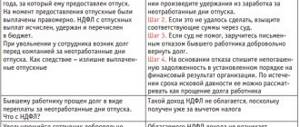

Answer

Account 209 “Calculations for compensation of costs” is used only if the employee does not agree with the amount of the debt and refuses to return the overpayment.

If the employee’s vacation pay was given in advance, then the debt that arose during recalculation as a result of dismissal must be transferred from account 302.11 “Payroll calculations” to account 206.11 “Payroll calculations”.

Transactions where an employee deposits arrears of wages into the institution's cash desk must be reflected through account 206.11, having previously reversed the accruals and adjusted the debit balance in account 302.11: Debit 2,401 20,211 Credit 2,302 11,730 - using the "red reversal" method - the amount of vacation pay issued is reversed in advance; Debit 2,302 11,830 Credit 2,206 11,660 - using the “red reversal” method - the overpayment debt was transferred to the advances account; Debit 2,201 34,560 Credit 2,206 11,660 - the overpayment amount was deposited into the institution’s cash desk.

Rationale

How to keep overpaid wages

Accounting

How to reflect in accounting the deduction of overpaid wages from an employee

If an employee’s salary was calculated and paid in a larger amount by mistake, make two transactions at the same time:

1. adjust excessively accrued amounts using the “red reversal” method;

2. transfer the debt to account 206.11 “Payment payments”.

Complete both transactions with an Accounting Certificate (f. 0504833). In it, indicate the number and date of the corrected transaction log, justify the corrections (clause 18 of the Instructions to the Unified Chart of Accounts No. 157n).

Transfer the overpayment from account 206.11 to account 209.30 “Calculations for compensation of costs” if:

the employee does not agree with the amount of the overpayment and refuses to return it;

during the year the employee did not repay the debt or was not retained on time. The fact is that overdue receivables for expenses in account 206.11 cannot be reflected in the Balance Sheet.

This follows from paragraph 220 of the Instruction to the Unified Chart of Accounts No. 157n, paragraphs 80, 86 of Instruction No. 162n, paragraphs 102, 109 of Instruction No. 174n, paragraphs 105, 112 of Instruction No. 183n and confirmed in paragraph 4 of the letter of the Ministry of Finance of Russia dated November 9, 2021 No. 02- 06-10/65506, paragraph 1.1.8 of the appendix to the letter dated February 2, 2021 of the Ministry of Finance of Russia No. 02-07-07/5669 and the Treasury of Russia No. 07-04-05/02-120, paragraph 1.1.5 of the letter dated December 30, 2015 Ministry of Finance of Russia No. 02-07-07/77754, Treasury of Russia No. 07-04-05/02-919.

In accounting for budgetary institutions:

Reflect the adjustment and deduction of overpaid wages with the following entries:

| № | Contents of operation | Account debit | Account credit |

| 1. | Excessively accrued wages reversed | Using the “red reversal” method | |

| – which forms the cost of services (work, finished products); | 0.109.ХХ.211 | 0.302.11.730 | |

| – which is immediately written off as expenses and does not form the cost of services (work, finished products) | 0.401.20.211 | 0.302.11.730 | |

| 2. | The overpayment debt was transferred to the advances account | Using the “red reversal” method | |

| 0.302.11.830 | 0.206.11.660 | ||

| XX – analytical code of the group and type of synthetic account of the accounting object. |

If the employee has not repaid the debt by the end of the year or disputes the amount of the overpayment, make the following entry:

| № | Contents of operation | Account debit | Account credit |

| 1. | Compensation for overpayment of wages | 0.209.30.560 | 0.206.11.660 |

When you withhold an overpayment from your next paycheck, make the following entries:

| № | Contents of operation | Account debit | Account credit |

| 1. | Deduction of overpaid wages reflected | 0.302.11.830 | 0.304.03.730 |

| 2. | Settlements with employee are closed | 0.304.03.830 | 0.206.11.660 0.209.30.660 |

| 3. | Salary paid for the next month minus the amount of overpayment: | ||

| 3.1. | – cash from the cash register | 0.302.11.830 | 0.201.34.610 |

| Increase in off-balance sheet account 18 (KOSGU 211, KVR 111) | |||

| 3.2. | – cashless transfer to the employee’s bank account | 0.302.11.830 | 0.201.11.610 |

| Increase in off-balance sheet account 18 (KOSGU 211, KVR 111) | |||

| XX – analytical code of the group and type of synthetic account of the accounting object. |

Such rules are established in paragraphs 73, 85, 102, 109, 128 of Instruction No. 174n, paragraph 4 of the letter of the Ministry of Finance of Russia dated November 9, 2016 No. 02-06-10/65506, paragraph 1.1.8 of the appendix to the letter dated February 2, 2017 of the Ministry of Finance of Russia No. 02-07-07/5669 and the Treasury of Russia No. 07-04-05/02-120.

Accounting and tax accounting

As with all income, personal income tax is deducted from wages and transferred to the treasury by the employer acting as a tax agent at a standard rate of 13% for residents (persons living in Russia for more than 183 days a year without traveling) and 30% for non-residents ( not living within Russia for 183 consecutive days a year), as well as insurance contributions to extra-budgetary funds at a general rate of 30%.

The vacation itself is carried out at the expense of the company, the payment is included in the list of expenses to reduce the tax base for income tax.

And the dismissal of an employee before the end of the year entails an excess payment to him in the organization’s accounting department and the deduction of this amount. Consequently, it is necessary to change the amounts for taxes and insurance contributions to state funds.

Firstly, on the day of payment for vacation, the company did not make any errors in keeping records of operations, since the problem is not related to the vacation pay themselves, but to the termination of the employment contract before the end of the calendar year.

Data clarification for the time before the vacation and during the vacation is not carried out; there are no errors according to the law. Corrective actions are necessary during the period of dismissal itself.

If the salary is not enough

What if the employer did not withhold everything from the former employee? For example, at the time of his dismissal he was not entitled to a salary. Will he be able to recover the balance in court ? Most likely no. This conclusion follows from the ruling of the Judicial Collegium for Civil Cases of the Supreme Court of the Russian Federation dated 02/05/2018 No. 59-KG17-19.

The bottom line is this: the employer (department of the Ministry of Internal Affairs) could not withhold payment from the employee for unworked vacation, since at the time of dismissal she was not owed any payments . The woman did not want to voluntarily compensate for the excess, and the employer filed a lawsuit.

The first and second instances sided with the organization, but the Supreme Court supported the employee. The judges simply did not find legal grounds that would allow judicial collection of the debt under such circumstances.

That is, simply because the amount of payment upon dismissal turned out to be less than the debt, it will not be possible to collect the balance through the court. The only thing left for the employer in this case is to offer the employee to repay the debt voluntarily.

Tax nuances of vacation advance forgiveness

The debt forgiveness agreement signed by the parties automatically triggers the tax adjustments associated with this event.

For the employee, recalculation of tax obligations does not lead to material losses - the tax on his income in the form of a forgiven debt has already been withheld when he was paid vacation pay. Changing the status of the amount received from vacation pay to a bonus from the employer (debt forgiveness) does not have an impact on personal income tax obligations.

What to do with personal income tax if an employee voluntarily repays the debt on advance vacation pay, see the material “Personal income tax on unearned vacation pay is subject to return.”

The employer's situation is different. In connection with the “act of goodwill” in relation to the employee, the income tax will have to be recalculated. In this case, it becomes necessary to exclude from expenses the amount of unearned vacation pay (clause 1 of Article 252, clause 49 of Article 270 of the Tax Code of the Russian Federation). Tax officials consider such expenses to be economically unjustified (letter from the Federal Tax Service for the city of Moscow dated June 30, 2008 No. 20-12/061148).

With regard to the amount of unearned vacation insurance premiums accrued, it should be noted that there are no grounds for their recalculation - they were accrued within the framework of the labor relationship. The legality of their inclusion in tax expenses is not disputed by officials of the Ministry of Finance (letter dated April 23, 2010 No. 03-03-05/85).

Tax features

The need to recalculate accrued taxes and contributions depends on what the administration decided to do with excessively issued vacation pay. If these amounts are “forgiven” to the employee, then there is no need to recalculate personal income tax and insurance contributions. They are, first of all, payments to the employee, and therefore are subject to both personal income tax and insurance payments.

On the other hand, if you refuse to withhold the amount, it is necessary to adjust the base for calculating income tax - they must be excluded from expenses that reduce income.

When withholding, it is necessary to adjust the amounts of contributions and withheld personal income tax only at the time of dismissal. There is no need to make corrections on the day the payments themselves were made.

The amount of vacation pay that was issued in excess reduces the base for contributions to social funds in the month of their return by the employee. In this regard, the calculation of deductions will need to be made on a reduced base.

When a 2-NDFL form is drawn up, it is necessary to reduce the amount of earnings received for this month by the amount of withheld vacation pay, and the amount of accrued personal income tax by the amount of tax received during the recalculation.

Attention! The administration is obligated to inform the employee about this within 10 days when excessively withheld personal income tax amounts arise. The latter must apply for the return of these amounts.

The administration, after receiving this application, can reduce the amount of tax that needs to be transferred to the budget by the amount of tax submitted by the employee for refund.

Withholding excess vacation pay

In accordance with Art. 115 and 122 of the Labor Code of the Russian Federation, the organization is obliged to annually provide the employee with basic paid leave of 28 calendar days. The right to use vacation for the first year of work arises for the employee after six months of his continuous work in this organization. By agreement of the parties, paid leave may be granted to the employee before the expiration of six months.

If an employee quits before the end of the working year for which he has already been granted vacation, he will have a debt to the employer for unworked vacation days. The employer has the right to withhold the amount of debt from the money due to the employee upon dismissal. Deductions from an employee’s salary are made only in the cases specified in Art.

137 Labor Code of the Russian Federation. According to the norms of this article, deductions from an employee’s salary to repay his debt to the employer can be made: · to repay an unspent and not returned timely advance payment issued in connection with a business trip or transfer to another job in another locality, as well as in other cases; · to return amounts overpaid to the employee due to accounting errors, as well as amounts overpaid to the employee, if the body for the consideration of individual labor disputes recognizes the employee’s guilt in failure to comply with labor standards (Part 3 of Article 155 of the Labor Code of the Russian Federation) or simple work (Part. 3, Article 157 of the Labor Code of the Russian Federation); · when an employee is dismissed before the end of the working year for which he has already received annual paid leave for unworked vacation days.

Deductions for these days are not made if the employee is dismissed on the grounds provided for in paragraph 8 of Part 1 of Art. 77 or paragraphs. 1, 2 or 4 hours. 1 tbsp. 81, pp. 1, 2, 5, 6 and 7 tbsp.

83 Labor Code of the Russian Federation. Consider a situation where an employee resigns of his own free will. According to the provisions of Art. 138 of the Labor Code of the Russian Federation, the total amount of all deductions for each payment of wages cannot exceed 20%, and in cases provided for by federal laws - 50% of wages due to the employee. At the same time, the legislation does not contain any exception regarding the withholding of amounts of excessively accrued vacation pay.

The rest of the debt can be repaid by the employee voluntarily. If the employer for some reason does not withhold the amount due from the employee, then it is impossible to recover it in court in the future. This is indicated by Part 4 of Art. 137 of the Labor Code of the Russian Federation, according to which a penalty can be made only in case of a counting error, the employee’s fault for failure to comply with labor standards or idle time, as well as in the case of unlawful actions of the employee.

A similar rule is contained in Art.

1109 of the Civil Code of the Russian Federation, according to which wages and equivalent payments and other sums of money provided to a citizen as a means of subsistence are not subject to return as unjust enrichment, in the absence of dishonesty on his part and an accounting error. To calculate the amount to be refunded, you need to determine the number of calendar days of vacation that the employee rested in advance. And then multiply the number of days of unworked vacation by the average daily earnings to calculate vacation pay.

The employee got a job on August 1, 2006.

In March 2007, he was granted annual basic leave of 28 calendar days.

When paying for vacation, the average daily earnings was 1,000 rubles.

When deducting for unworked vacation days, it is necessary to recalculate all taxes and other mandatory payments: unified social tax, personal income tax, income tax, insurance contributions for compulsory pension insurance. Today, tax authorities take the position that overpaid vacation pay is a mistake.

And, referring to Art. 54 of the Tax Code of the Russian Federation, require the submission of updated tax returns.

But this position can be argued.

According to the letter of Rostrud dated June 23, 2006 No. 947-6, the Labor Code does not provide for the provision of annual paid leave of a certain duration in proportion to the time worked by the employee.

If there is a right to such leave, the employee has the right to receive paid leave of a specified duration.

The fact of recalculating vacation pay upon dismissal is not a correction of an error, since at the time the vacation was granted, the calculation was made correctly and the accountant did not know that the employee would quit before the end of the working year. The employee got a job on September 5, 2006.

In April 2007, he was granted annual basic leave of 28 calendar days. When paying for vacation, the average daily earnings was 900 rubles.

The salary due to the employee upon dismissal is 25,500 rubles.

Types of leave and reasons

An employee can take advantage of the following types of leave:

- regular paid;

- additional paid;

- study leave;

- maternity leave;

- Holiday to care for the child.

Based on average values, for each full month worked, an employee is entitled to 2.33 days of vacation (with 28 calendar days of vacation). After working 6 full months in the organization, the employee has the right to take a vacation of 14 days.

In this case, upon dismissal, the employee will not owe anything to the employer. If vacation is granted for a longer period, vacation pay is paid in advance.

Debt to the employer can only arise if the limit for the next paid leave is exceeded. Upon dismissal, the employer has the right to withhold the amount of paid vacation days that the employee had not paid at the time of dismissal.

This is determined by Articles 127 and 140 of the Labor Code of the Russian Federation.

An order is issued, which must contain:

- withholding amount;

- number of advance vacation days;

- final settlement date;

- a provision that the amount of withholding cannot be more than 20% of the total payment;

- familiarization of the employee with the order.

Vacation rights and responsibilities

Upon termination of the employment relationship, the employer must perform many mandatory actions regulated by labor legislation. Among them is the obligation to give the employee everything he earned by the time of dismissal.

Vacation payments are one of the elements of the final settlement with a resigning employee. Their composition depends on how many vacation days have been accumulated and whether the employee has exercised his right to vacation in the current period (Article 127 of the Labor Code of the Russian Federation).

For information on the circumstances affecting the calculation of vacation days upon termination of an employment contract, see the material “How to calculate the number of vacation days upon dismissal?”

In addition to this obligation, the employer has the right to withhold from the resigning employee’s income the amount of advance vacation pay (Article 137 of the Labor Code of the Russian Federation).

This right may not be exercised in all cases. If the dismissal of an employee occurs on the grounds listed in Art. 137 of the Labor Code of the Russian Federation, it will not be possible to withhold overpaid vacation pay from him. For example, such a prohibition on retention applies to the situation of dismissal due to staff reduction or closure of a company, as well as in other cases provided for by law.

In addition, the employer can deal with the employee’s debt in a different way - we’ll talk about this in the next section.

Rules

Deductions for unworked vacation days upon dismissal are calculated in all cases except the following:

- the employee’s refusal to transfer to another position required for medical reasons, or the employer’s lack of the required vacancy;

- liquidation of an enterprise, termination of the activities of an individual entrepreneur;

- reduction of staff of the organization, individual entrepreneurs;

- change of owner of the enterprise;

- conscription of an employee for military service;

- reinstatement of a person who previously performed work by decision of a court or state labor inspectorate;

- recognition of a person as incapacitated;

- death of an employee;

- the onset of emergency circumstances: military operations, catastrophe, natural disaster, major accident, epidemic.

If an employee who has been granted leave leaves work for any other reasons, deductions for unworked vacation days upon dismissal must be calculated.

Deduction of overpaid amounts from an employee's salary

It often happens that some amounts need to be withheld from an employee’s salary. This can happen for various reasons, for example, after the payment of wages, an error in the accruals is discovered or the employee becomes indebted due to damage to the enterprise. Please tell me what amounts are legally withheld from an employee’s salary under Russian law? How to properly withhold such amounts?

Deductions from wages can be different: at the request of the employee himself, according to executive documents, or by order of the employer. The latter, in turn, can occur in the case of:

(or) the employee causes material damage to the employer;

(or) payment of excess amounts to the employee within the framework of the employment relationship (hereinafter referred to as excess payments) (Article 137 of the Labor Code of the Russian Federation).

The procedure for withholding excess payments differs from the procedure for withholding amounts of damages. Let's see what constitutes excess payments, how they can be withheld from an employee, and what to do if this fails.

Can an employer sue?

A situation may arise when the calculation of unworked vacation days has been made, but the amount of earnings is not enough to repay the entire debt. If the employee refuses to pay the amount in cash, the employer bears losses.

In this case, there are two opinions that differ from each other. In the first option, they refer to Law No. 169, which expresses theses about regular and additional leaves. According to this legal document, the employer does not have the right to recover from the employee after his dismissal.

But many experts agree that this document contradicts a number of articles of the Labor Code. Therefore, any employer has the right to sue an employee.

How to calculate the amount of deductions for unworked vacation days

First, determine the number of months not worked before the end of the working year for which the employee was granted leave. Take fully worked months into account. Round the remaining days in months not fully worked to full months according to the rounding rules. Discard the remainder up to 14 calendar days inclusive, and round up the remainder from 15 calendar days or more to a full month.

This procedure is provided for in paragraph 35 of the Rules approved by the People's Commissariat of the USSR on April 30, 1930 No. 169. Despite the fact that this document was adopted a long time ago, it continues to be in force insofar as it does not contradict the Labor Code of the Russian Federation.

Example

The employee was hired by the company on June 16, 2014. The working year for granting leave is from June 16, 2014 to June 15, 2015. The employee took 28 calendar days of leave for this working year in December 2014. The employee resigns of his own free will on March 2, 2015.

The period from June 16, 2014 to February 15, 2015 is eight full months. From February 16 to March 2 – another 15 days. This month is taken as a full month. In total, the employee worked for nine months. This means that upon dismissal, the organization has the right to withhold from the employee the amount of vacation pay accrued for three unworked months (12 - 9).

Then calculate the employee's average daily earnings to pay for vacation.

Determine the total amount that needs to be withheld from an employee’s salary upon dismissal using the formula:

| Amount of deductions | = | Average daily earnings | X | Number of months not worked | X | (Duration of leave allotted to an employee per year/ | 12 |

The employee must reimburse the organization for the entire amount of unearned vacation pay. But you can keep no more than 20 percent of the amount in hand.

Example

An employee of Voskhod LLC, D.I. Sokolov, joined the company on December 15, 2014. From August 3 to August 29, 2015, he was on vacation for 28 calendar days (this is the amount of annual leave in the company).

In September 2015, Sokolov wrote a letter of resignation of his own free will and was fired. His last day of work is September 21, 2015. It turns out that in total he worked for the company for 9 months and seven days. This means that he must return part of the accrued vacation pay. The employee had the right to count on a vacation of 21 calendar days (28 days: 12 months × 9 months).

Therefore, he must be deducted vacation pay for 7 days of vacation (28 - 21), to which he was not entitled.

Let's assume that Sokolov's vacation pay was calculated based on the average daily earnings of 681.12 rubles. Thus, the employee is owed RUB 4,767.84. (681.12 rubles × 7 days).

For the days worked in September 2015, Sokolov was accrued 14,285.71 rubles. 20 percent of this amount is 2857.14 rubles. This is exactly how much an accountant can deduct from an employee.

Situation: what to do if it is impossible to withhold vacation pay issued in advance from an employee’s salary

Invite the employee to voluntarily return the amount of vacation pay for unworked vacation days. In case of refusal, the organization, of course, has the right to apply for recovery to the court (Article 391 of the Labor Code of the Russian Federation).

The legal norm that previously prohibited employers from collecting such vacation pay in court has become invalid (Order of the Ministry of Health and Social Development of Russia dated April 20, 2010 No. 253). However, in this case, the courts, as a rule, are on the side of the workers (see the ruling of the Voronezh Regional Court dated December 6, 2011 No. 33-6954, the ruling of the Supreme Court of the Russian Federation dated October 25, 2013 No. 69-KG13-6).

How to calculate the amount of overpaid vacation pay upon dismissal

Calculation of withholding for leave upon dismissal is made using the following formula:

UDNO = (FEFD − DOS) × WHSD,

Where:

UDNO - deduction for days of unused vacation;

DFO - the number of vacation days actually taken;

DOS - the number of vacation days allotted in accordance with the vacation record;

ZSD - average daily earnings calculated at the time of payment of vacation pay.

Stages of calculating intermediate indicators:

- To calculate the DOS indicator, you must divide by 12 the number of vacation days stipulated by law or employment contract for the working year (minimum 28 days). Then the resulting value should be multiplied by the number of months actually worked. If the resulting number of days turns out to be a fractional number, then it is rounded in favor of the employee (letter of the Ministry of Health and Social Development “On the procedure for determining the number of vacation days...” dated December 7, 2005 No. 4334-17).

- WHSD is calculated in the manner specified in Part 4 of Art. 139 of the code, taking into account the adjustment for the time actually worked, if it does not reach 12 months (clause 6 of the regulation, approved by the government decree “On the specifics of the procedure for calculating average wages” dated December 24, 2007 No. 922).

So, deduction for vacation used in advance but not worked is made in the amount of no more than 20% of the earnings paid upon dismissal. The amount of debt that exceeds the amount of actual withholding is repaid by the dismissed individual or collected by the employer through the court. It is important to remember that in some cases there is a ban on making deductions upon dismissal (for example, due to the liquidation of the employer).

How to determine average daily earnings

To calculate the vacation debt, the accountant must determine the average daily earnings (Article 139 of the Labor Code of the Russian Federation). But there is no need to separately calculate this indicator as of the date of dismissal. Use in the calculation the amount that was on the start date of the employee’s vacation. This procedure is due to the fact that the company retains the money that the employee received previously.

How to calculate the number of unworked months

In addition to average earnings, the accountant determines how many months the employee did not work in a year, during which he already had time to take vacation. When calculating, use two rules.

This is also important to know:

Article 77 of the Labor Code upon dismissal: grounds for terminating an employment contract

The first rule is that the accounting year is not equal to the calendar year, that is, it does not have to start on January 1 and end on December 31.

An employee has the right to annual paid leave every year (Article 122 of the Labor Code of the Russian Federation). It is equal to 12 months and starts from the date of hiring (letter of Rostrud dated June 14, 2012 No. 853-6-1). Moreover, the length of service for calculating vacation includes (Article 121 of the Labor Code of the Russian Federation):

- days the employee worked;

- annual leave, days of incapacity, holidays and weekends;

- days that the employee took at his own expense. But no more than 14 calendar days per year are taken into account.

The second rule is that if an employee, in addition to whole months, also has unworked days, then they are rounded up to full months. The main thing to remember here is that a balance of 14 days or less is not taken into account. And days starting from 15 are rounded up to a full month.

For example, an employee has 4 months and 17 days left unworked. Then the accountant will take into account the deduction of 5 months.

How to find out how many vacation days an employee is entitled to per year

Typically, vacation is 28 calendar days (Part 1, Article 115 of the Labor Code of the Russian Federation). For most employees, this is the value that the accountant will take to calculate compensation and deductions for unused vacation upon dismissal. However, there are exceptions.

For example, if your employee is under 18 years old, then he should have 31 calendar days of vacation (Article 267 of the Labor Code of the Russian Federation). For teachers, the formula uses 42 or 56 days (Article 334 of the Labor Code of the Russian Federation). The specific value depends on the position of the teacher (Resolution of the Government of the Russian Federation of May 14, 2015 No. 466). Disabled people have the right to 30 days (Article 23 of the Federal Law of November 24, 1995 No. 181-FZ).

How much can be withheld from an employee for vacation used in advance upon dismissal?

Of the payments due to an employee upon dismissal, the accountant has the right to withhold no more than 20 percent of the amount that remains after deducting personal income tax (Article 138 of the Labor Code of the Russian Federation). Anything above that, the employee has the right to pay off voluntarily.

Example

The manager started working on August 22, 2021. He retires on June 19, 2021. In December 2021, the manager took 28 calendar days off. The average daily earnings was 501 rubles.

The manager's working year begins on August 22, 2021 and ends on August 21, 2021. The unworked period is two months and two days. According to the rules, we round this value to two full months.

For June 2021, the manager was credited 25,000 rubles. He has no deductions for personal income tax, so the tax is 3,250 rubles. (RUB 25,000 x 13%). Amount to be issued – 21,750 rubles. (25,000 rub. - 3,250 rub.)

You can withhold no more than 4,350 rubles. (RUB 21,750 × 20%).

The debt for vacation provided in advance is 2,338 rubles. (501 rubles × 2 months × 28 days: 12 months). The accountant can withhold the entire amount of the debt from the salary.

Example 1. Calculation of the withheld amount of excess payment for vacation pay upon dismissal

A.V. Ostrov worked at Vasilek LLC from December 1, 2015. His working year was supposed to last until November 20, 2021. During this period, he was granted leave of 28 days. The average employee's earnings were 230 rubles. But A.V. Ostrov resigned on June 30, 2016. The amount to be withheld is calculated.

| Data for calculation | Calculations |

| Number of vacation days - 28; number of months in a year - 12; number of unworked months of the dismissed person - 5 | Unworked vacation time (by days): 28 / 12 (months) = 2.3 days; 2.3 (days) * 5 (number of months not worked) = 11 days (rounded) |

| The unworked part of the vacation is 11 days; average earnings are 230 rubles. | Retention amount: 11 days * 230 rub. = 2,530 rub. |

It turns out that the fired person did not work for 5 months. This means that he was paid an extra amount of vacation pay, which should be returned to the cash desk of Vasilek LLC. So, Vasilek LLC withheld 2,530 rubles. from the amount of salary paid to the dismissed A.V. Ostrov when calculated on the last day of work.

Example 2. Withholding of excess vacation pay upon dismissal of an employee, standard account assignments

P. V. Smirnov worked at Zorka LLC from January 15, 2016. He was granted leave from July 15, 2016 for a period of 12 days. After his vacation, P.V. Smirnov worked until August and resigned by agreement of the parties on August 15, 2016. Thus, he did not work until the end of the working year for 5 months.

Since the dismissed person took 12 days of vacation for a full working year, and did not work for 5 months, the employer has the right to return the excess payment of money for 5 days (12 / 12 = 1 day; 1 * 5 = 5 days). On the last day of work, P.V. Smirnov was given the payments due, from which the amount for the 5 unworked days of vacation pay was withheld. The accounting department used the following basic account assignments:

- DT 20 (26, 44, etc.), CT 70 - crediting salary upon dismissal;

- DT 20 (26, 44, etc.), CT 69 - contributions to the Pension Fund;

- DT 70, CT 68 - personal income tax calculation;

- DT 20 (26, 44, etc.), CT 70 - reduction of expenses by the amount of excess vacation pay payments;

- DT 20 (26, 44, etc.), CT 69 - correction of PFR;

- DT 70, CT 68 - personal income tax correction;

- DT 70, CT 50 - salary issued.

Calculation of the amount

To convert the resulting number of days into monetary terms, the average annual salary of the employee is required.

Mechanism for determining the average salary:

For example, you need the value of average annual earnings. The number of working days of the year is required. In 2021 it is 247 days.

An employee's salary, for example, is 30 thousand rubles.

Average salary per day: 30,000 rubles * 12 months / 247 days = 1,457 rubles.

Therefore, this number is multiplied by the number of days received in the previous calculation. The result is advance leave.

If, according to the mathematics of vacation pay, it turns out that the sum of unworked days exceeds the number of days in the last vacation - for example, the calculated advance vacation is 12 days, and the actual final one is 10 days - then the company’s accounting department needs to examine the average salary of the last year and vacation.

As a result, the deduction for the last actual vacation is calculated based on the average salary during this period, and for the difference - 2 days - based on the average salary of the previous vacation period.

If an employee decides to quit

However, controversial issues begin to arise if an employee who took leave for an unworked period decides to quit. It’s worth noting right away that the employer cannot keep him at the enterprise. HR department employees should also not refuse to hand over a work book, as this would be illegal.

There are two ways of peaceful settlement. In the first case, the employer simply withholds the amount that was written out for unworked time. This situation is possible when dismissal occurs at the end of the month in which all days were worked. In this case, there will be enough funds to repay the entire amount. The second option is also to pay off the debt, but in cash to the company’s cash desk.

It is worth noting that some people mistakenly believe that an employer cannot withhold more than twenty percent of accrued wages. In this case, they refer to Article 138 of the Labor Code. But it should be understood that here we are talking specifically about salary. Withholding for the unworked period is regulated by Article 137. Therefore, the employer can withhold the entire amount of wages after calculating the tax.

It is worth noting that the calculation of vacation days can only be rounded towards the employee. That is, the employer cannot make a deduction for three days instead of 2.33. And in two whole days - maybe. This is enshrined in the Labor Code.

Debt repayment

For accounting purposes, it is necessary to calculate the amount of amounts not withheld for advance leave. However, if this amount is insignificant and the clarifications in the reporting are not worth this amount, the employer can “forgive the debt” - not withhold it and not declare repayment (for this, a forgiveness agreement is drawn up), and after the expiration of the limitation period - 3 years - determine write it off as hopeless.

However, at the request of the parties, it is possible not to withhold overpaid vacation pay and arrange for debt forgiveness according to the established procedure:

an agreement is formed between the parties to repay the debt for overpayment for unworked vacation; the agreement contains the will of both parties, signatures and details; tax accounting is adjusted - in the case of an employee, there are no changes in the taxpayer’s position, and the organization is obliged to clarify the amount of income tax, expenses for unwithheld payments of vacation days are deduced from it. No changes are made to insurance premiums.

How much can be withheld from your salary upon dismissal?

In accordance with Article 138 of the Labor Code of the Russian Federation, withholding when paying salary cannot exceed 20% . If the amount of overpaid vacation pay is less, then it can be withheld without restrictions. But no more, even if the employee quits. There is an explanation on this matter - letter of the Ministry of Labor of the Russian Federation dated October 22, 2018 No. 14-1/OOG-8142.

In the same letter, the department reminds employers that they are not required to withhold excess vacation pay. They decide this issue at their own discretion. If an employee receives extra money, no one, naturally, will punish her for this.

Complications

A more thorough and complicated formula is used when, while this employee was on vacation, the company increased the salaries of the entire staff or the department in which he was registered.

In such a situation, an increasing factor is applied for the period from the increase in earnings to the end of this vacation.

To do this, unworked vacation days are calculated from the beginning to the last day of vacation. Then the ratio of days before and after the salary increase is determined. For example, the vacation lasted from September 20 to October 9. The number of unworked days is 9. The salary in the employee’s department was increased on October 1. Therefore, the number of unworked days with an increasing coefficient is 9.

Next, the following mathematical formula is used: the number of unworked vacation days before the increase * the average vacation salary + the number of unworked vacation days after the increase * the average vacation salary * increasing factor.

For example, the salary was increased by 10%. The average salary is 1,500 rubles per day.

Calculation: 9 * 1500 + 9 * 1500 * 10%.

The result will be the sum of days of unworked vacation.

Personal income tax and contributions

How are contributions withheld when paying vacation pay calculated? It all depends on whether the amount of the last salary is enough to collect. If the funds due are sufficient to pay off the debt, then the following actions are performed.

1. The accounting system reflects the calculation of wages. In this case, deductions for unworked vacation days upon dismissal are not calculated. Personal income tax, contributions are calculated according to the standard scheme. Excess amounts withheld will be reversed if the annual statements have not yet been signed. Otherwise, you will have to correct the data in the balance sheet.

2. When paying vacation pay, personal income tax is transferred to the budget. Excess amounts must be returned to the employee. In order for the amount to be recalculated, you need to provide the Federal Tax Service with a clarifying certificate 2-NDFL and reflect all calculations in it. The date of receipt of salary upon dismissal is considered to be the last day of work. Therefore, the last salary in the report for the current year should be reflected in the month of dismissal. The organization is not obliged to submit clarifications of the RSV-1 Pension Fund for the period in which the employee was on vacation. Contributions were calculated without errors, there is no need to update the data.

Deductions from the employee: vacation paid, but not worked out

The employee has used his vacation in advance and quits. Vacation pay was paid, but the vacation itself, it turns out, was not spent. What should I do? Does the employer have the opportunity to return funds to which the employee was not actually entitled? And if so, how to calculate the worked and unworked part of the vacation? Let's figure it out.

From this article you will learn:

- what is the procedure for granting leave to an employee

- does the employer have the right to withhold part of the payment for the vacation provided if it is not worked out?

- in what cases the employer cannot withhold vacation pay

- how to correctly calculate the amount of deduction for unworked days upon dismissal of an employee

As a general rule, an employee who has worked at a new job for six months receives the right to use annual paid leave. In this case, the employer is obliged to provide him with leave of full duration, i.e. 28 calendar days (Article 115 of the Labor Code of the Russian Federation). By agreement of the parties, vacation can be used by the employee before the expiration of six months of work (i.e., provided in advance). Moreover, labor legislation does not contain rules that would allow an employee to be granted annual leave in proportion to the time he worked and other periods included in the length of service giving the right to leave in accordance with Part 1 of Art. 121 of the Labor Code of the Russian Federation (Letter of Rostrud dated June 23, 2006 No. 947-6). For the second and subsequent years of work, vacation may be granted to the employee at any time of the working year in accordance with the vacation schedule approved for the next calendar year (Article 122 of the Labor Code of the Russian Federation).

Five main news of August that will change the work of the HR department

For example, an employee was hired on December 22, 2009. His working year for vacation is the period of time from December 22, 2009 to December 21, 2010 inclusive. The employee will have the right to use leave of 28 calendar days from June 22, 2010.

Issue of the magazine as a gift!

In the event that an employee quits before the end of the working year for which he has already been granted leave, the employer has the right (but not the obligation) to withhold part of the payment for this leave corresponding to the days not worked, except in cases where withholding is prohibited (para. 5 part 2 article 137 of the Labor Code of the Russian Federation).

When is the ban on withholding vacation pay applied?

The employer may withhold excess paid vacation pay for vacation received in advance from the resigning employee’s salary, with the exception of a few cases. So, according to para. 4 hours 2 tbsp. 137 of the code, deduction upon dismissal for leave provided in advance cannot be made if the employee quits due to:

- refusal to transfer to another job for medical reasons or because the employer does not have such an opportunity;

- reduction of staff at the employer or its liquidation, as well as a change of owner, which led to the dismissal of the company’s management;

- reinstatement by decision of the court (labor inspectorate) of an employee who previously worked in this position;

- conscription for military service (including alternative);

- recognition of an employee as incapacitated for medical reasons;

- the occurrence of force majeure, recognized by the Russian government as such and not allowing further continuation of work;

- death of the individual employer.

If at least one of the above grounds occurs, the employer does not have the right to withhold vacation pay upon dismissal. If an employee quits for other reasons, then the employer has every reason to make a deduction for the vacation used from his salary upon dismissal. Retention, in accordance with Part 3 of Art. 137 of the Code must be made within a month after the end of the period specified for the employee to repay the debt incurred in the form of overpaid vacation pay.

If we talk about deduction for unused vacation upon dismissal, then it is not made, since vacation pay in this case was not paid to the employee. Moreover, before dismissal, the employee is provided with appropriate compensation, calculated according to the rules on regular and additional leaves, approved by the People's Commissariat of Labor of the USSR on April 30, 1930 No. 169 (hereinafter referred to as the Rules).

According to Art. 28 of the Rules, compensation is paid:

- For the entire vacation, if the employee worked for 11 or more months or worked for more than 5.5 months and was dismissed due to the liquidation of the employer company, conscription for military service, or recognition as unfit for medical reasons.

- Proportional to actual time worked.

That is, when calculating compensation for vacation that was not used before dismissal, overpayment of vacation pay is not possible, since they were not previously paid, while compensation payments are calculated based on actual data.

Free legal consultation

We will answer your question in 5 minutes!

Free legal consultation We will answer your question in 5 minutes!

Ask a Question

Ask a Question

It is also not allowed to withhold compensation for unused vacation upon dismissal, for example, in the event of subsequent reinstatement of an employee in position, since neither the Labor Code nor any other regulatory act contains such grounds for deduction from salary. Moreover, previously paid compensation does not give the employer the right to refuse to grant leave to the reinstated employee.

Deduction for used vacation in advance upon dismissal

Any employee receives the right to full vacation six months after employment, Art. 122 Labor Code of the Russian Federation. The same article also lists those categories of workers who may not wait for the expiration of this period:

- pregnant women before maternity leave or after maternity leave;

- adoptive parents;

- minors.

Whether they will work until the end of the year is a big question, but the amount of vacation pay is paid three days before the vacation in full. What an employer should do in the event of sudden dismissal of a rested employee is described in Art. 137 Labor Code of the Russian Federation. In it, the law allows excess vacation pay to be withheld from the last salary. Article 138 of the Labor Code limits the amount of such withholding to 20% of paid earnings. Even the written consent of the resigning employee will not help increase the percentage.

The fact of reducing the amount of payments upon dismissal must not only be announced to the employee, but also agreed upon with him. If an employee objects and does so in writing, then the accounting department has no right to withhold vacation pay accrued in advance. In this case, the dispute, after the employee has been dismissed, can only be resolved by the court.

Under no circumstances is an enterprise allowed to claim a refund of vacation pay received in advance if the employee is dismissed at the initiative of management and through no fault of his own, as well as due to circumstances beyond his control. Even if the leave is taken in advance, no one will make a decision in favor of the employer. Moreover, the employer does not have the right to force the employee to work until the end of the working year and postpone the date of dismissal.

When do unearned vacation pay appear?

The following example will help you understand the mechanism by which unearned vacation pay appears.

Technical University graduate P. N. Ptichkin got a job at a helicopter plant on July 1, 2020, and in January 2021 he received the right to go on vacation (paragraph 2 of Article 122 of the Labor Code of the Russian Federation) and took advantage of this opportunity. The duration of his vacation was 28 calendar days (Article 115 of the Labor Code of the Russian Federation).

Find out more about the provision of leave and its duration from the article “Annual paid leave under the Labor Code (nuances).”

During his vacation, he received a more lucrative job offer and immediately after returning from vacation, he quit the plant.

Thus, by the time of his dismissal, P.N. Ptichkin had earned only half of his legal leave: 14 days (6 months × 28 days / 12 months), and used all 28 days. There were 14 vacation days unworked at the time of dismissal (28 – 14).

Since the employee received the full amount of vacation pay before going on vacation, by the time of dismissal he had a debt to the company for the 14 days of vacation paid in advance.

IMPORTANT! The right to vacation for the first working year arises after six months of work in the organization (Article 122 of the Labor Code of the Russian Federation). Subsequent vacations are issued according to the approved schedule.

What the lack of a vacation schedule in a company can lead to, see the material “Unified Form No. T-7 - Vacation Schedule” .