Indexation is the protection of the population from inflation by increasing payments (pensions, benefits, salaries for public sector employees) by the percentage by which prices increased due to inflation.

In the Russian Federation, pension accruals for citizens consist of the following parts:

- Basic (credited to all citizens: unemployed, homeless, everyone who has a passport is entitled to it).

- Insurance (depends on contributions to the Pension Fund).

- Cumulative (applies only to citizens born after 1967, depends on the results of investing contributions).

The size of the basic pension in 2021 increased twice - in February and in April.

This article is about how much state assistance should increase for working and non-working pensioners, about the basic pension in 2021 in Russia and about the government’s further plans for increasing them.

Concept of pension parts

During the reform process, the first wave of which took place until 2015, it was established that government payments to current pensioners would consist of three parts:

- Basic.

- Insurance.

- Cumulative.

The general basis of regular monthly income is its basic element. It is understood as a material amount that is intended for all persons who have reached the established retirement age and have a minimum work experience of a total of five years.

The basic pension for the subject of pension legal relations is fixed at the federal level at a single rate and is subject to indexation every year. The payment of the basic part of the labor pension is financed from the federal budget from the amounts of the unified social tax received by it.

The insurance part is based on the length of working periods and the amount of wages of a citizen during the period of his labor function.

Components of a labor pension

On behalf of each worker, the employer sends monthly contributions to the pension fund. It is these contributions that become the numerical value for the future determination of the insured share of pension payments.

Reference! The amount of insurance payments is calculated based on a simple formula, according to which the entire total of monetary contributions to the pension fund is divided by 19 (the average life expectancy of a citizen who has reached retirement age) and multiplied by the standard duration of the insurance period. This position is reflected in.

Calculation of insurance pension

The funded part refers to the material assets of compulsory pension savings, which are managed by professional market participants, in the interests of a person who will qualify for pension provision in the future.

How does the basic pension differ from the insurance and funded pension?

Since all these 3 elements (basic, insurance, savings) form the future basis of the monthly payments due, they have much in common in their content.

However, there are signs by which one can distinguish the components of pension provision.

- First of all, the insurance element of preferences directly depends on the person’s salary. The higher the established monetary rate, the greater the volume of deductions that goes to extra-budgetary state funds. This means that the final level of pension will differ significantly in size. While the basic part has no relationship with how much money a citizen received at his place of work before retirement. The base is expressed in clearly fixed dimensions.

- According to pension legislation, the basic part of the salary must be paid to employees immediately after reaching a specified age. A pensioner can receive the insurance component in full or in part, or may refuse to receive it altogether.

- The funded element of pension provision has similar distinctive features from the basic value, as does the insurance part.

Where does pension funding come from?

For the most detailed analysis, it is necessary to consider those aspects by which the insurance and savings parts are differentiated from each other, in isolation from the value of the base component.

What does it consist of?

The amount of the basic insurance payment is now called a fixed rate; it is determined by the state and paid from the local or state budget. It may depend on the category, which is determined depending on the type of work of an able-bodied citizen.

The basic payment is an echo of the past, then it was about some kind of “equalization”, when all pensioners received an almost equal amount. The fixed part has replaced it and is a guarantee of social security for pensioners. The size of the basic part is fixed , but you still need to obtain the right to have it credited to you.

A prerequisite is to obtain a joint venture. It, in turn, is paid only upon reaching a certain age and length of service.

How is the basic part of the labor pension recalculated?

Recalculation of pension indicators refers to actions through which, on the basis of an application from an authorized citizen, a change in the amount of the monthly compensation payment is made.

The legislation established four grounds when pension preferences may be subject to differentiated revision:

- A pensioner reaches the age of eighty.

- Transformation of the degree of limitation of the ability to work, both upward and downward.

- Change in the number of family members with limited working ability.

- Transformation of the category of recipient of labor compensation in the event of the loss of a breadwinner.

A revision of the value of the basic element of a labor pension in connection with a citizen reaching the age of eighty years is carried out from the day this subject reaches the designated age.

In other cases, recalculation is carried out from the first day of the month after which the subject’s application was received to revise the fixed amount of the pension upward.

Reasons for recalculating the basic part of the pension

Submission rules

Citizens of the Russian Federation can apply for the basic component of a pension upon loss of a breadwinner, disability, or reaching the appropriate age.

To do this, you need to contact the pension fund and provide documents confirming your membership in one of the listed categories.

Age

When it comes to a survivor's pension, the age of the recipient does not matter. An important condition is the child’s minority and incapacity to work. After age 18, payments automatically stop. The exception is full-time university study.

For women, the age for achieving the basic component of the pension is 55 years, for men – 60 years. In some cases, retirement age comes earlier (harmful working conditions, military experience, etc.).

It is important to know! At what age do you apply for a pension in Ukraine?

Experience

When calculating the base, an important condition is the number of days worked. If a person has not worked for 8 years, then he cannot apply for a base according to the law. The exception is disability.

For disabled people, it is enough to have one entry in the work book, where it is recorded that he worked for at least 1 day officially. The same scheme applies to calculating the base for the loss of a breadwinner.

If a citizen of the Russian Federation has not worked a day in an official job, he can apply for a social pension, which is calculated without taking into account the base.

Fixed payment

The concept of a fixed payment, like many other innovations, came to the Russian legal system in 2015. It refers to a specifically established figure, fixed at the legislative level, which is intended to be paid to a citizen who has reached retirement age.

It is worth noting that this terminology has come to replace the old-established definition of the basic part of the pension. Although the essence of the concepts, as well as the procedure for assigning payments, are similar to amazing accuracy.

The following persons have the right to receive this compensation:

- Citizens applying for pension benefits due to reaching a specifically established age.

- Citizens applying for pension benefits due to bodily dysfunctions that lead to disability.

- Citizens applying for pensions due to the loss of a breadwinner.

The final amount of the benefit depends on which classification group the recipient belongs to. The amount of money previously allocated to state funds does not affect the size of the fixed part of the preference.

Video - Savings and insurance part of pension

Requirements for recipients of fixed payments

Based on the current state of affairs, we can conclude that declaring monthly social payments later than the generally established retirement age is the most profitable from an economic point of view. For each annual period of later application, the insurance pension and fixed payment are increased by the corresponding coefficients.

However, in order to become eligible for two types of these compensations, you must initially meet a number of criteria in 2021:

- Cross the line of a certain age. For males it is sixty years, for the female half of the population it is fifty-five years.

- Have at least nine years of official work experience (as of 2019).

- Have 13.8 pension points (as of 2019). They are added based on salary.

In the near future, these requirements will be tightened. By 2025 it will take fifteen years and thirty points.

Estimated changes by 2025

Above we discussed the classic characteristics of persons who carried out labor activities on a general basis.

But there are also less socially protected segments of the population for whom privileged conditions are established:

- Citizens who have worked in areas with unfavorable climatic conditions for at least fifteen years are entitled to receive fixed payments regardless of age and points.

- For disabled people, the basic pension amount is established after a medical and social examination makes a decision on assigning a disability group.

- Dependents who have lost their breadwinner are entitled to a fixed payment from the day of the loss of the family breadwinner.

Also important is the fact that, depending on the capabilities of regional budgets, citizens may be assigned additional basic values. For example, a regional fixed payment for a dependent. All these preferences are subject to joint summation.

Pension formation

What was the basic pension in 2021

According to current legislation, social security cannot be less than the subsistence level.

In this case, values are taken into account both for Russia as a whole and in individual cities and regions.

For example, in Moscow the lower limit is 10,670 rubles, and in St. Petersburg – 9,617.9 rubles (figures are for 2021). That is, the pension in these cities cannot be less than the given values.

Submission rules

Law No. 400 provides for the possibility of assigning one of three types of pensions:

- according to the age;

- for loss of a breadwinner;

- on disability.

To assign one of them, documentary evidence may be required:

- accumulated experience;

- disability groups;

- the fact of reaching retirement age;

- lack of livelihood due to the loss of a breadwinner.

The calculation of the basic basis of pension provision will be carried out automatically, but taking into account all of the above factors.

Age

The fixed part of the benefit is assigned only upon reaching the established age, which is 60 years for men and 55 years for women.

At the same time, Article 30 of Law No. 400 defines a number of conditions under which payment of security can be assigned ahead of schedule (difficult and harmful working conditions). If a pension is to be provided in the event of the loss of a breadwinner or due to disability, then age does not matter.

Experience

The length of service affects the amount of pension benefits.

In addition, without a certain length of employment (in 2021 it was 8 years), an insurance pension will not be assigned at all.

Payments to disabled people are assigned if they have a minimum insurance period (1 day of official work is enough). This also applies to survivor benefits (the length of service of the deceased is taken into account).

In the absence of any length of service, citizens are assigned a social pension, which does not include the basic pension payment (Federal Law No. 166).

Fixed basic amount of old-age labor pension in 2021

The introduction of clearly fixed values has become one of the social guarantees of providing Russians with a minimum amount of compensation payments.

As of 2021, the basic portion for a worker who left his position due to reaching retirement age is 4,983.27 thousand rubles. From the analysis it follows that this amount in 2002 was 550 rubles per month. The positive fact of annual indexation of payments and their compliance with the minimum subsistence level is noted.

The described compensatory share of state preferences falls into the category of mandatory for all citizens of retirement age with more than five years of work experience.

Thus, after working for a period of average duration, it is possible to secure a certain amount of government compensation.

How to calculate the amount of an insurance pension

To whom is the basic part of the pension accrued?

The basic (fixed) part of the pension is accrued to all citizens of the Russian Federation, regardless of their length of service. All citizens of the Russian Federation apply for it, including those who, for one reason or another, have never worked.

Fixed payments are calculated in accordance with the following parameters: Old age.

- Old age.

- Disability.

- Maintenance of a dependent.

- Having northern experience.

- Work in agriculture.

- Living in the regions of the far north.

The size of fixed accruals must constantly increase, as stated in Article 16 of the Law “On Insurance Pensions”. The main provisions are:

- Fixed payments must increase annually. The amount of the increase must correspond to the percentage of inflation. Recalculation must occur no later than February 1. The percentage of inflation by which benefits should increase is taken for the previous calendar year.

- On April 1, the State Duma may decide on a second increase. The decision must be made in accordance with the financial capabilities of the pension fund.

The basic pension in 2021 was fully indexed, unlike in 2021. Then the inflation rate reached almost 13%, and old-age payments increased only by 4%. In order to somehow compensate for the shortfall, a decision was made to provide one-time assistance in the amount of 5,000 rubles. According to the Pension Fund, all pensioners, including those who continue to work, received this money.

Increase factor for late retirement

From modern statistical indicators it follows that Russians rarely delay the appointment of monthly payments, because the average life expectancy is not so high - 65.9 years for men and 76.7 years for women.

For each year of the latest application to state pension preferences, bonus coefficients are established:

- When applying for an insurance pension one year later, the fixed payment coefficient increases by 1.07.

- When applying for an insurance pension two years later, the fixed payment coefficient increases by 1.15.

- When applying for an insurance pension three years later, the fixed payment coefficient increases by 1.24.

- When applying for an insurance pension four years later, the fixed payment coefficient increases by 1.34.

- When applying for an insurance pension five years later, the fixed payment coefficient increases by 1.45.

Bonus coefficient table

This progression cannot continue indefinitely and its maximum score will be 2.11 - for people of retirement age performing a labor function.

The maximum score is no more than 3 - for persons of retirement age who perform a labor function and do not have a funded part of their pension.

Based on the above, we will formulate the advantages and disadvantages of late retirement:

- In case of delayed retirement, the final volume of fixed payments will increase by an increasing factor (+).

- While the subject of pension legal relations is working, the employer sends deductions of insurance contributions to state extra-budgetary funds for him and, consequently, the amount of insurance payment increases (+).

- The indexation of pension benefits for pensioners who continue to work has been canceled since 2016 (-).

- Low average life expectancy of the Russian population (-).

Thus, late retirement has both disadvantages and advantages. Each pensioner should proceed from the current individual situation.

Video - What is an insurance and funded pension?

Who is entitled to the basic pension?

You can apply for the basic component in the following cases:

- A person has lost the ability to work due to the development of a disability.

- The child has lost his breadwinner and needs additional financial assistance to support himself until he reaches adulthood.

- There is a need for retirement according to length of service , when the total length of work in production allows you to apply for a pension benefit.

- Reaching the age when the basic pension is due by law.

- The person who wishes to receive a pension is supported by dependents.

The size of the basic component depends on many factors and will differ for different categories of the population.

What to do if there are reasons to increase your pension?

The bodies of the pension system of the Russian Federation carry out an annual recalculation of mandatory payments based on the reasons for their increase. This privilege can be exercised in two ways:

- Increasing your insurance pension without an application. In these cases, the territorial administration of the Pension Fund increases the individual pension coefficient of the worker from August 1 of each year. Thus, under these circumstances, the interested party does not need to take any action. In most situations, the competent authorities themselves must identify the reasons for increasing monthly payments and establish them.

- The application form for increasing the fixed amount of pension benefits is reflected in the following cases:

- the appearance of disabled dependents for a citizen of retirement age. The number of no more than three people will be taken into account. Such people must be on long-term or permanent financial support from a pensioner;

- stay in territories north of the Arctic Circle and areas similar to these areas. The increase in pension payments will occur in accordance with regional coefficients for the entire period of residence in the above-described zones;

- the occurrence of the required calendar work experience in the regions of the Far North and areas similar to these areas.

How is the pension amount calculated?

During the application procedure, the interested entity will need to fill out a form to the Administrative Regulations, a sample of which is contained on the official website of the Pension Fund.

The application shall indicate:

- Passport data (series, number, who issued it, date and place of birth, etc.).

- Addresses of actual location and place of registration.

- Phone number.

- Insurance number of an individual personal account.

- Information about citizenship.

If the stated requirements are met, the increase in pension benefits will occur from the first day of the month following the calendar month in which the above-described application was considered.

Who can count on an increased payment

Certain categories of citizens can count on an increased amount of pension benefits. These include:

- Elderly people over 80 years of age . Pensioners who are over the age of eighty can count on a pension fund that is twice the base amount. In 2021, it is 10,668.38 rubles for them.

- Pensioners with dependents . Dependents should be understood as persons who are financially dependent on the pensioner and who do not have the opportunity to find employment. These include minors until they reach the age of 18.

The status of a dependent can be maintained after reaching the age of eighteen if the citizen is studying full-time at an educational institution. In accordance with the law, for each dependent, in addition to the already accrued payments, an additional allowance is given in the amount of 1/3 of the FV (1,778.06 rubles). The maximum number of dependents is no more than three.

- Previously worked in the Far North . “Northerners” can also count on an additional bonus. Thus, persons who have worked in the KS districts for at least 15 years receive an increase of 50% of the FV. Those who have worked for at least 20 years at the ISS have the right to count on additional payments in the amount of 30% of the FS.

- Citizens who have periods of labor activity in agriculture. If a pensioner has worked for at least 30 years in the agro-industrial complex, then he has the right to receive a bonus in the amount of 25% of the FV, but only on the condition that at the time of receiving the pension he lives in a rural area. If he moves to the city, the right to additional material support ceases.

What if the pension is below the subsistence level?

Old-age insurance pensions, the amount of which is below the pensioner’s subsistence level, will increase in January 2021 in accordance with the new indexation mechanism.

It provides an increase in payments even if the pensioner is entitled to a Social Supplement.

How does indexing work in this case?

First, the pensioner’s income, including pension and other social benefits, is brought by the Social Supplement to the Pensioner’s Subsistence Minimum in the region of residence, and then an increase is established to this amount based on the results of indexation.

Thus, all non-working pensioners who are entitled to indexation receive an increase in payments in January.

Questions and answers

Citizen N. has been raising a daughter from her first marriage for 10 years. Her ex-husband, with whom she had not maintained any relationship for the last 5 years, died. Previously, he worked on temporary jobs and did not have a permanent job. Citizen N. herself is in a civil marriage and does not work due to a difficult pregnancy. Is she entitled to receive a survivor's pension and how to apply for it? – If a woman is unemployed and has a dependent minor child, she can receive a survivor’s pension, even if her ex-husband did not officially work. In this case, a social benefit is assigned, which is equal to the size of the basic component. If a woman proves that her family is on the verge of poverty, then she can apply for a similar pension for her own maintenance.

Citizen I. is dependent on four minor children. What amount of the basic component is he entitled to if he plans to retire before his children come of age? – at the legislative level, pension supplements are established in the presence of dependents, in the amount of 1/3 of the base for each disabled family member, but not more than for 3 family members. Therefore, the size of the basic component in this case is calculated using the formula: 4982.9+(1661×3)=9965.9 rubles.

Pension calculation by period

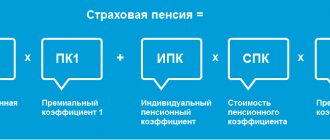

The algorithm for calculating a pension comes down to determining the number of points (individual pension coefficients, IPC) for the period of a person’s activity, depending on length of service and salary. The number of points is then multiplied by the cost of one.

The value of a point varies from year to year and depends on the year of retirement. In this case, amendments are applied due to the conditions of formation of experience and salary. The calculation method for periods is not the same.

Calculation for periods before 2002

Pension savings for the specified period are initially calculated in monetary terms, then transferred to the IPC. This takes into account the valorization and indexation of pensions. To calculate future payments, it is necessary to calculate the estimated pension (RP) and the amount generated due to valorization.

The estimated pension is calculated based on the length of service until 2002 and the average salary for 2000–2001. Or, at your choice, 5 years of continuous work until 2002 (which is more profitable).

Accounting for experience until 2002

Experience is not taken into account in full, but using the experience coefficient (SC):

- Continuous service until 2002 is equal to or exceeds 25 years for men, 20 years for women. In this case, SC = 0.55. For each year exceeding 25 (20) years, one hundredth is added. For example, a man has 28 years of experience, SC = 0.58 (0.25 + 0.03). The limit value is limited to 0.75.

- Continuous experience less than 25 (20) years. In this case, the coefficient is 0.55 no matter what.

How is length of service before 1991 taken into account?

The rules for accounting for length of service in this period do not differ from those for the period before 2002. The exception is valorization. This is a one-time increase in pension savings formed in 2002. Its size is 10%. In addition, savings up to 1991 increased by 1% annually.

Most of today's pensioners earned their seniority in Soviet times

How is salary calculated?

The calculation takes into account the average salary for 2000-2001, or for any 5 years of continuous service until 2002 (the more profitable one is selected). Here, the coefficient of average monthly salary (AMS) is applied, equal to the ratio of the real average salary of a person per month for a specified period to the statistical average salary at the same time.

If 2000–2001 is selected, then the SFC is equal to the average salary divided by 1.494.5 (the accepted average salary for these years). If a five-year calculation is used, it is necessary to divide the real average salary of a citizen for 5 years by the established amount for the same period.

RMS cannot be more than 1.2. Only for residents of the Far North is excess allowed. They, depending on the region, have an upper limit of 1.4-1.9.

Methodology for calculating the estimated pension until 2002.

The estimated pension is calculated using a special formula that takes into account the length of service coefficients and the earnings ratio. RP is displayed in rubles; different formulas are used for citizens with different coefficients.

- SC is more than 0.55. The estimated pension is equal to the product of the length of service coefficient and the salary ratio multiplied by 1671. 450 is subtracted from the resulting amount. RP as of 01.2002 = SK × KSZ × 1671 – 450. The minimum amount is limited and cannot be less than 250.

- SC is less than 0.55. This means that less than 25 (20) years of work have been completed, depending on gender. In this case, the desired result is multiplied by a coefficient equal to the number of years worked over a period of time divided by 25 (20). RP as of 01.2002 = (0.55 × KSZ × 1671 – 450) × (Experience before 2002 ÷ 25) for men; RP as of 01.2002 = (0.55× KSZ × 1671 – 450) × (Experience before 2002 ÷ 20) for women. The final amount is the amount of the estimated pension.

Calculation of the amount of IPC earned before 2002.

Pension capital until 2002 consists of the amount of the estimated pension and the amount of valorization and indexation. Periods before 2002 were indexed until 2015, as of this date the total indexation coefficient, equal to the product of all annual coefficients, is 5.6148.

Consequently, the amount is equal to the amount of the estimated pension and income from valorization, multiplied by the total indexation coefficient. The resulting result, divided by the cost of a point in 2015, is the number of points accumulated in the period before 2002. For 2002, the cost of a point is 64.10 rubles.

Total: IPC until 2002 = (estimated pension + valorization amount) × indexation coefficient ÷ 64.10.

Calculation for the period from 2002 to 2015.

In this period, calculations are carried out immediately in points. The number of points is affected by the amount of mandatory insurance contributions paid by the employer to the Pension Fund for the employee, defined as a fixed percentage of wages.

In 2021, it is 22%. 16% is converted into points, and a fixed payment is formed from the rest. The maximum taxable base is 912,000 rubles. If the annual salary is more than this amount, no contributions are collected from the excess portion.

Individual entrepreneurs pay an annual fixed contribution in the amount of 32,448 rubles. per year, plus 1% on income over 300,000 per year.

The sequence of actions for calculation is as follows:

- The amount of insurance premiums paid for each year in which insurance premiums were paid is multiplied by the indexation coefficient in the same year.

| Year | Indexation coefficient |

| 2002 | 1,307 |

| 2003 | 1,177 |

| 2004 | 1,114 |

| 2005 | 1,127 |

| 2006 | 1,16 |

| 2007 | 1,204 |

| 2008 | 1,269 |

| 2009 | 1,1427 |

| 2010 | 1,088 |

| 2011 | 1,065 |

| 2012 | 1,101 |

| 2013 | 1,083 |

| 2014 | 1,101 |

The results obtained are summarized.

- Total amount paid for 2002–2015 contributions, taking into account indexation, are divided by the period of expected pension payment (survival period). This is an estimated value equal to 228 months in 2021.

- The desired result is divided by the value of the pension point in the year of retirement; in 2021 it is equal to 64.10 rubles. As a result, we get the number of points earned in the specified period.

Total: number of points = amount of contributions with indexation ÷ 228 ÷ 64.10.

Period since 2015

The point system has been used since 2015. The methodology for calculating pensions for the period after 2015 is identical to that used for the period 2002-2015. The cost of the point and the conditions for retirement changed annually in accordance with the reform. Certain categories of citizens are awarded points without paying insurance premiums. Including:

- military service – 1.8 points;

- caring for one child – 1.8 points, two – 3.6, three – 5.4;

- caring for a disabled person or a person over 80 years old – 1.8 points.

How to convert the number of points into rubles

To calculate a future pension, you need to sum up all accumulated IPC over different periods, multiply by the cost of the point in the year of retirement and add a fixed payment. It means a monthly cash payment that does not depend on the amount of insurance premiums paid and is guaranteed by the state. At the beginning of 2021, the amount of the fixed payment to the old-age insurance pension is 5,686.25 rubles . Upon reaching 80 years of age, the amount doubles.

Insurance pension = number of points accumulated over all periods × cost of a point in 2021 (93 rubles) + fixed payment (5686.25 rubles).