We recommend entrusting your tax refund to a personal consultant in the online personal income tax service.

Every citizen of the Russian Federation who receives income taxed at a rate of 13% and has a child (children) to support has the right to contact the employer or the tax authority with an application for a standard deduction (Article 218 of the Tax Code of the Russian Federation).

If the parent is the only one and there is no second one, for example, due to death or for other reasons specified below, the standard deduction is provided in double amount (paragraph 7 of subparagraph 4 of paragraph 1 of Article 218 of the Tax Code of the Russian Federation).

It reduces the amount of income on which income taxes are withheld.

Example

You have one child. Salaries were accrued in the amount of 46,789 rubles in January 2021. Provided that you are the only parent, 2800 rubles are deducted from the specified amount (1400 is the standard double tax deduction for the first child).

It turns out 43989 rubles. - income on which tax is withheld at 13%. The further calculation is as follows: 43989 – 13% (5718.57 rubles) = 38270.43 + 2800 = 41070.43 rubles. It is in this amount that wages must be paid in person.

If an individual works for several employers, the deduction will be provided for one place of work, at the employee’s choice.

The reduction of income by the amount of the double deduction begins from the moment the right to it arises and ceases on a general basis, like the standard deduction, or from the moment the only parent marries.

Examples of calculations

The amount of a single deduction for the first and second heir is one thousand four hundred rubles, and for the third heir - three thousand rubles.

Table. Amount of benefit depending on the number of minor dependents

| Order number | Double deduction for a blood offspring, adopted child or children of a legal spouse, in rubles | Double tax refund for adopted children, in rubles |

| For the firstborn | two thousand eight hundred | two thousand eight hundred |

| For the second child | two thousand eight hundred | two thousand eight hundred |

| For the third, fourth, fifth, etc. | six thousand | six thousand |

| For a child officially recognized as disabled | twenty four thousand | twenty four thousand |

Example 1. Zaitseva V.V. two sons: one is 5 years old, the other is 9. Their father died in a car accident several years ago, so the mother is considered the only parent. The woman works at Stroysoyuz OJSC and receives a monthly salary of 40 thousand rubles, which are subject to taxation at the rate of thirteen percent. Zaitseva will receive a double tax deduction for her sons:

1400 * 2 =2800 p. per child

2800 * 2 = 5600 p. for both children.

Income tax will be calculated from Zaitseva’s earnings:

(40000 – 5600) * 13% = 4472 p.

In total Zaitseva earned:

40000 – 4472 = 35528 p.

If Zaitseva does not take advantage of the benefit guaranteed by the Tax Code, the company will calculate her earnings as follows:

40000 * 13% = 5200 p.

40000 – 5200 = 34800 p.

As a result, due to the tax refund, Zaitseva’s monthly earnings will increase by 728 p. (35528 p. – 34800 p.). The parent will only receive a tax refund for eight months, starting in January. Since in September her salary will exceed three hundred and fifty thousand rubles.

Example 2. The Orlovs have one newborn son and two daughters. The latter are working adults. The Orlovs can only get money for the youngest. Since he is the third in this family, the parent and parent will have their tax bases reduced by three thousand rubles. But Orlov P.E. I didn’t want to take the benefit and wrote a corresponding statement in favor of my wife. Thus, Orlova’s taxable amount will be reduced by six thousand rubles on a monthly basis. The return of finances will be carried out until her earnings exceed three hundred and fifty thousand.

Her salary is 50,000 rubles, so the accounting department will calculate her deduction as follows:

(50000 – 6000) * 13% = 5720 p.

And she will receive it in her hands

50000 – 5720 = 44280 p.

Instead of 43500 (50000 – 50000 * 13%)

Difference 780 p.

Tax Code of the Russian Federation. Excerpts from Article 218. Standard tax deductions

Example 3. The Mikhalkov couple have a common son, Kirill. Also, Sergei Petrovich Mikhalkov has two heirs from his previous marriage, and his wife had no children before her marriage. Mikhalkova Anna Andreevna voluntarily unsubscribed from the fiscal benefit in favor of Mikhalkov S.P. Her husband can count on the usual deductions for the first two children and double for Kirill. This will happen:

1400 p. (for the 1st) + 1400 p. (for the 2nd year) + 3000 p. * 2 (double for III third) = 8800 rubles

His salary is 20,000 p. Mikhalkov S.P. will receive benefits for all 12 months, since his earnings do not exceed the limit.

(20000 – 8800) * 13% = 1456 p.

The following will be transferred to the husband’s card:

20000 – 1456 = 18544 p.

If the Mikhalkovs do not apply for benefits, the husband’s earnings will be calculated differently:

20000 – 20000 * 13% = 17400 p.

Example 4. Egorov R.N. - single father. He has an only son - a disabled person of the second group. He is eighteen years old. Every month Egorov receives a salary of 35,000 p. He is entitled to deduction only in the first ten months of the year. His earnings will be calculated as follows:

(35000 – 24000) * 13% = 1430 p.

35000 – 1430 = 33570 p.

If Egorov does not exercise his legal right to the benefit, his income will be:

35000 – (35000 * 13%) = 30450 p.

The difference is 3120 p. (33570 – 30450).

Double tax deduction calculator

Go to calculations

Who is eligible for this income tax benefit?

There are several situations provided for by law when an employee has the right to take advantage of a double benefit. At the same time, the amounts expected by the standard tax deduction for personal income tax are doubled. Not all parents can take advantage of this form of preferential taxation .

The standard double deduction for income tax is provided:

- Single parent , foster parent, guardian or adoptive parent who has the status of a single parent;

- To one of the parents when the other renounces his right to a tax deduction for personal income tax.

Sizes in 2021

The standard form of personal income tax benefits for children provides for fixed amounts of standard deduction:

- for the first child – 1400 rubles ;

- for the next born child – 1400 rubles. ;

- for the third and each younger person - 3000 rubles .

Deductions are applied until pupils reach the age of majority, including children with physical disabilities, students of secondary schools and other educational institutions, graduate school, internship, residency, as well as students and students of military universities under 24 years of age.

If the deduction is double, then the above amounts should be multiplied by 2 .

When can I start receiving benefits?

A resident can apply for benefits for the first time from the moment when:

- baby was born;

- official adoption has occurred;

- the contract on the placement of a minor in foster care has entered into force;

- guardianship/trusteeship was approved.

The benefit ends when:

- a child who is not registered as a student at a higher educational institution has reached the age of majority;

- a child who is receiving higher education full-time has reached twenty-four years of age;

- the contract for placing the baby in a family has expired;

- the contract for placing a child in a family has become invalid.

A single mother (father) stops receiving a double refund after marriage registration.

In addition, a single parent or single father loses the opportunity to receive tax benefits due to the death of an offspring or the wedding of a son/daughter.

What documents are needed?

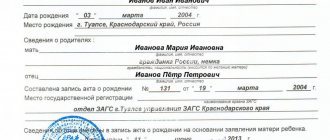

In the case where a double deduction is assigned to a single parent, the following documents are attached to the application:

- birth certificate , where in the column about the second parents there is a dash;

- if the father is indicated according to the mother, it is necessary to provide a certificate from the registry office in form No. 25 confirming this fact;

- death certificate of the second parent;

- a court decision recognizing the other parent as missing or deceased;

- a document confirming that the applicant is not married (copy of the relevant pages of the passport).

- Documents establishing the right of guardianship (trusteeship) over the child;

- If the application is submitted during employment, it is necessary to submit a 2-NDFL certificate from the previous place of work;

- For a child who has reached the age of 18 but is studying full-time - a certificate from the place of study ;

- If a child has a disability, an ITU document .

In the case where the applicant claims a double deduction due to the refusal of the other parent to apply this tax standard benefit, it is necessary to provide a statement from the second parent that he refuses to receive a deduction for children and a 2-NDFL certificate from his place of work confirming what is indicated in statement.

Such a certificate is submitted monthly in order to track a possible excess of the limit of the taxable base to which the benefit applies (350,000 rubles).

A standard personal income tax benefit can be applied for not only by contacting the employer, but also through the tax authorities . This happens in two cases:

- If the employer did not apply the tax deduction or did not apply it in full.

- If the taxpayer receives income taxed at a rate of 13% under self-employment conditions.

Documents are submitted to the tax authority within the framework of the declaration campaign, that is, before April 30 of the year following the reporting year. In the event that the employer has overpaid tax, the documents specified above (confirming the benefit) are submitted. These will be added:

- 3-NDFL, it can be filled out for free in the program from the Federal Tax Service;

- Certificate 2-NDFL from the place of work for the past year;

- Application for transfer of the overpayment to the applicant’s bank account indicating his details.

In the second case, the taxpayer independently calculates income tax taking into account the application of standard deductions, declares it and submits it to the tax office along with all documents establishing the right to tax preference.

Do I need to apply every year?

An application for this benefit must be written only once - when applying for a job or from the moment such a right arises. There is no need to re-write it every year.

An exception is made if circumstances have arisen that change the grounds for assigning a tax deduction. This could be the birth of another child, marriage, divorce from a spouse, or the death of a spouse or child.

Registration procedure

First of all, you need to submit a complete set of documents either to the accounting department of the organization in which you work, or to the nearest fiscal department.

Documentation

Prepare the following papers:

- declare your income on the Z-NDFL format;

- papers that will confirm that you have a legal right to a tax benefit (see list above);

- make a written request for a deduction indicating an account in a Russian bank in order to transfer money to it;

- a document about the sources of your cash income, their amount and the amount of taxes withheld (can be obtained from the organization where you are employed);

- domestic Russian official identification document;

In addition, you may need:

- certificate of absence of legal marriage;

- a document from an educational institution that the child is receiving full-time education;

- document on salary at the previous job if there was a change in the employer company.

Prepare duplicates of the papers listed above. You may also need real ones for verification.

At work

If you want to receive benefits at the company where you work, in addition to the application, provide a complete set of papers. Such documents include:

- birth registration certificates for all your children;

- if you have adopted a child, you will need a supporting document;

- a court order that you regularly pay alimony (in case of divorce);

- an agreement appointing you as obligated to pay child support on an ongoing basis;

- a document confirming that your heir has a disability group;

- a receipt from another person with whom the child lives that you are transferring money.

Let's consider a situation where a citizen needs to receive a tax refund if during the year he worked first in one organization and then moved to another. In this case, a document on the salary level must be provided not only from the current, but also from the previous job.

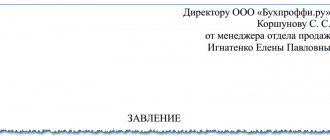

Example of an application for an employer

Take a piece of paper for your application. At the top right, enter:

- what is the name of the organization;

- information about the head of the organization;

- your details - last name, first name, patronymic, what position you hold;

- your IHH;

- your address.

On the next line, place the word “statement” (in lower case) in the middle. Next, state your request in a concise manner. Next, list the attached papers. Finally, include your autograph, last name and initials, as well as the current day, month and year.

Application example

At the fiscal service department

This method of receiving benefits is suitable for those who, for some reason, did not have time to submit papers during the tax period (year). Or he was not able to return the entire amount due. In this situation, you should choose the branch that is closest to your home. The fiscal service can provide a deduction only when the reporting year ends. The procedure for processing a refund through the tax authorities is as follows:

- At the end of the year, fill out a declaration in the Z-NDFL form specially designed for this purpose. This must be done before the thirtieth of April next year. So, if you are reporting for 2021, you must submit it before April thirtieth, 2019.

- From the accounting department of the company where you are employed, you will receive a certificate indicating the amount of your earnings.

- Prepare your documents. Be sure to make copies. The fiscal service employee will also need the original papers for verification.

- Give the employee a complete set of necessary papers:

- a document on the amount of salary accrued for the time period from January to December (filled out on form 2-NDFL, issued by the employer);

- declared information on cash receipts filled out in the Z-NDFL format;

- a written request to return tax money paid in excess;

- documents that confirm that you have the right to return funds (see list below).

After you hand in all the papers, tax service employees are required to check them. This is called a “desk check”. This procedure takes quite a long time. But within ninety days you will receive an answer. Thirty days after a successful desk check, money should arrive on the card whose number you indicated.

If necessary, a person can apply for a partial deduction from the employer, and pick up the rest at the fiscal department.

Example. In August, Nikolai Fedorovich Artakov began receiving deductions for his son Roman Nikolaevich Artakov. Until this moment, the parent was not able to apply for the benefit due to the lack of several certificates. Artakov can return what is missing if he contacts the fiscal authority when the year ends.

What if the documents were provided late?

By law, the deduction is provided to the employee from the moment the application is written. As a rule, this happens when applying for a job. If the employee has not drawn up this document, then the accountant has no right to make a deduction on his own initiative.

In practice, a situation may arise that an employee may fill out an application and provide supporting documents not immediately, but after some time. In such a situation, the deduction is also provided to him either from the moment he starts working in the organization, or from the beginning of the calendar year (if it was issued last year).

The need for such action was indicated by the Ministry of Finance in a letter issued on April 18, 2012 No. 03-04-06/8-118. In connection with the provision of a deduction, the tax will also need to be recalculated.

Attention! However, if an employee registered in one calendar year, but provided documents for the deduction in the next, then the company will no longer be able to recalculate the tax. In this case, you will need to independently prepare a 3-NDFL declaration, a package of necessary documents and submit them to the tax office.

Important points

Please consider the following important points:

- If the mother/father has lost parental rights through a court order, the parents are still required to provide financial support to their children. If the mother/father does not shirk their responsibilities, they can count on a child deduction.

- Parents do not lose the right to the benefit if their student child has applied for academic leave at the educational institution.

- Even if you send your heir to live or study in another country, you will not lose the opportunity to return taxes. But the fact of residence in another state must be documented. Supporting documents can be issued by the local government office of the country in which the children study or live.

There are situations when the mother or father, for one reason or another, did not work for some time. The reasons may be different: illness, dismissal, vacation, etc. There are several possible scenarios for the development of events:

- The benefit is not issued if a person has stopped earning money within a year and until January of the next year he had no payment for work or other cash receipts.

- If payments resume before January of the next year, a tax refund can be made. The money is returned to the citizen when the next earnings are issued, which is subject to taxation.

How is the child benefit calculated?

To understand how the calculation is done in practice, we will give a clear example. The family has four children. The eldest child just turned 15 years old, and the youngest is 5. The mother’s monthly income is 40,000 rubles. The parent submits a petition to the employer for partial reimbursement.

As mentioned above, the first and second child are entitled to 1,400 rubles each. And for the third and subsequent ones, 3000 each. In total, the total amount will be 8800 rubles. Every month, subject to registration of the return of the deduction, the employer from 8800 will return 13% to his employee. Such a refund will remain in effect until taxable income reaches 350,000. Then, starting next year, the partial refund will resume again.

If the mother of four children does not submit a petition, she will deduct 5,200 of her income to the treasury every month. But thanks to the submitted application, you can save about 1,500 rubles. It is worth noting that if a single parent is raising children, the deduction amount can be doubled. For these purposes, you need to contact the service at the place of registration for more detailed information.

How to return money to a single parent?

A mother or father can count on this state benefit if his child is natural, adopted or adopted.

A double return of funds is possible only if there is documentary evidence that the second holder does not have parental rights. A person who is married cannot apply for the benefit, even if the spouse is not the natural parent of the baby.

Confirmation of your right to a refund may be:

- a document stating that the second holder of parental rights is no longer alive;

- a court decision on the disappearance of the second holder of parental rights;

- a certificate of registration of the fact of the birth of a baby, in which the symbol “—” appears next to the word “father”.

- a document stating that the father did not recognize the child and when filling out the certificate, the mother named the father’s name (format No. 25, issued by the registry office).

Marriage of a single parent is a reason to stop paying double deductions

How to write an application correctly

One of the main documents, without which it is impossible to carry out the income tax refund procedure, is an application.

To correctly compile this document, the following recommendations should be taken into account:

- It is imperative to state in the document that actions are carried out strictly within the law, guided by the provisions of Article 218 of the Tax Code. The application must also indicate from what date it is planned to receive monetary compensation.

- Indicate information about the child for whom monetary compensation will be issued.

- Indicate the type of deduction. Enter information that the application is being submitted specifically for a double discount.

- Indicate the reason why increased compensation is due.

- List the list of documents that are attached to the application. Depending on the specific situation, the list of papers may be supplemented.

The other parent refuses the deduction

Only the following can write a waiver of tax refund in favor of the second parent:

- relatives mother or father;

- adoptive parents.

Neither trustees, nor adoptive parents, nor guardians have such a right.

In order for the second natural parent/guardian to receive a double return of funds, it is necessary that the parent/guardian who wrote the refusal receive income from which a thirteen percent tax is calculated. The benefit will be accrued until the income of the second parent/guardian exceeds RUB 50,000. (cumulatively from the beginning of the current annual period).

It is important that the parent who unsubscribes from the deduction has the rights to this state benefit. For example, if the baby’s mother is on maternity leave, she is not entitled to a deduction. Therefore, she will not be able to refuse it, and the father will not be able to receive double benefits.

To unsubscribe from additional funds, you must submit a written request to your employer. The company's accounting department should provide documentation that the deduction was not issued. You also need to get 2-NDFL from the accountant. The other parent should go to their employer, armed with these two certificates.

Sample application for waiver of deduction in favor of the other parent

A certificate of income of the refusing parent must be presented to the second parent's company every month. This is necessary so that the employer can track in which month the income of the second parent exceeds the limit of three hundred fifty thousand rubles.

Example. The father refuses the deduction in favor of the child's mother. His salary exceeded three hundred and fifty thousand in May. And the mother’s salary reached this mark in November. Thus, she will receive a double tax deduction from January to April, and a regular one from May to November. In the last month of the year, no personal income tax refund will be calculated.

Amount of deductions

The amounts of deductions and the procedure for their provision are determined in the Tax Code of the Russian Federation.

For a healthy child

If the child is healthy, then the single parent or the parent in whose favor the other one refused the deduction receives double tax benefits.

| Child | Benefit amount |

| First | 2800 rub. |

| Second | 2800 rub. |

| Third and subsequent | 6000 rub. |

For a disabled child

In this case, the child will qualify for two benefits at once - directly for the child, and also due to disability. Previously, only one benefit was provided. However, with the release of clarifications from the Ministry of Finance, as well as due to the practice of court cases on this issue, benefits are subject to summation.

| Child | Benefit amount |

| The first disabled child is being raised by parents | 26800 rub. (2800+24000 rub.) |

| The second child is disabled, raised by parents | 26800 rub. (2800+24000 rub.) |

| The third and subsequent disabled child is being raised by his parents | 30,000 rub. (6000+24000 rub.) |

| The first disabled child is being raised by a guardian | 14800 rub. (2800+12000 rub.) |

| The second disabled child is being raised by a guardian | 14800 rub. (2800+12000 rub.) |

| The third and subsequent disabled child is being raised by a guardian | 18,000 rub. (6000+12000 rub.) |