Fictitious deal

During tax control activities (inspection activities) in relation to the taxpayer, the tax authority may come to the conclusion that the person being inspected has carried out fictitious transactions or business transactions with a certain circle of counterparties. What do tax authorities mean by a fictitious transaction today? From the point of view of tax authorities, a fictitious transaction is a transaction made by a taxpayer without pursuing any economic purpose. In other words, these are transactions or other business transactions that were carried out by the taxpayer and his counterparty solely for the purpose of reducing the tax base.

Such conclusions of tax authorities are quite fraught for taxpayers and can lead to very serious consequences - additional taxes, penalties, fines, sometimes equal in size to the annual revenue of the taxpayer’s company. The most unfavorable outcome for the taxpayer may be the transfer of tax audit materials to the investigative authorities for the initiation of a criminal case on the facts of intentional evasion of taxes and fees by the taxpayer. Moreover, if the taxpayer himself carries out his activities under absolutely legal conditions, this does not mean that charges cannot be brought against him for violating tax laws, since those companies whose counterparties are already on the so-called “check mark” may also be at risk » from tax authorities as counterparties noticed in fictitious transactions with other persons.

Fictitious transactions: what businesses should pay attention to so as not to fall into the risk zone

Recently, unfortunately, news often appears about criminal cases against the founders and managers of companies who are charged with illegal methods of minimizing tax payments. Tax optimization methods, which are well within the framework of the current Tax Code, in some cases may provoke claims from tax and other authorities. Our experts – lawyer, partner of the law office “Stepanovsky, Papakul and Partners” Elena Sapego and founder of the accounting firm Olga Ivanenko – draw attention to important legal and accounting subtleties in this area. We believe that their comment will help you avoid common mistakes and not fall into the risk zone.

– Transactions for the provision of services that inflate costs and reduce the base for paying income tax come under special control. Since for the most part such transactions are not material, and it becomes problematic to prove the fact of provision of services, they attract the greatest attention from tax inspectors.

And, of course, tax services pay special attention to checking their validity. A typical example of such “intangible” transactions are contracts for the provision of marketing or information services.

Let's look at common mistakes.

Not long ago, we were faced with a situation where a company operating in the wholesale trade sector entered into an agreement for the provision of customer search services with an individual entrepreneur. At first glance, a legitimate way to increase sales did not turn out to be so upon closer examination.

That's why:

1. The report on the provision of client search services included only those clients with whom contracts were concluded much earlier than with individual entrepreneurs.

2. The individual entrepreneur’s remuneration for concluding contracts with clients amounted to 95% of the company’s income.

3. The individual entrepreneur was an interdependent person in relation to the company.

This example is a typical illustration of the formal approach to tax relations. According to the law, no one prohibits hiring an individual entrepreneur to provide this type of service, since the costs of finding a new client are associated with an increase in sales of goods. Formally, the criteria are met, but in reality the business is at high risk in the event of tax audits.

At first glance, one can detect signs of a fictitious agreement, which was concluded only “for show.” Civil law defines such transactions as imaginary.

Photo from the site sablezubka.ru

How to distinguish such a transaction from a real one, which is truly important for the organization’s business?

Here are the criteria:

1. Availability of a detailed report on the essence of the marketing research conducted or on the information collected during the execution of the contract.

By the way, the presence of a report is a mandatory requirement of regulatory authorities for such contracts. It is a detailed, thorough report on the implementation of the subject of the contract that is the main indicator of the reality of the corresponding contract.

As a rule, such a report is accompanied by questionnaires, questionnaires, and other materials, which allow the customer to obtain the desired result for the service provided and are the basis for appropriate marketing or information analysis and conclusions.

2. Average market price level for the relevant service. Well, a businessman will not give 95% of his income to an attracted marketer!

Photo from framepool.com

And no businessman counting his money will pay for a service above the market price.

3. The production nature of the relevant costs. By the way, it is also determined on the basis of a report on the execution of a marketing or information contract.

It is impossible to reduce income tax by the amount of relevant costs if the result of the services does not in any way affect or affect the production activities of the company.

For example, the cost of paying remuneration to third parties for information about how the real estate market is developing in Russia for a Belarusian company selling clothing on the domestic market has no operational necessity or significance. In addition, the assessment of the production nature of such expenses is often made by regulatory authorities purely subjectively.

Accordingly, document flow becomes of paramount importance.

Photo from www.financeink.com

Unfortunately, no one likes filling out paperwork, and this often leads to negative consequences.

Although it is well known that, for example, the legislation imposes its own requirements on primary accounting documents. And, by the way, they are not that overpriced.

First of all, there must be a primary accounting document. It is its presence that is the basis for classifying certain payments as expenses for tax purposes.

And, of course, this document must be drawn up correctly. It must comply with all mandatory conditions established by the legislator.

For example, according to the Law “On Accounting”, the acceptance certificate must contain “the name of the document, the date of its preparation; name of the organization, surname and initials of the individual entrepreneur who is a participant in the business transaction; the content and basis for a business transaction, its assessment in natural and value terms or in value terms; positions of persons responsible for the execution of a business transaction and (or) the correctness of its execution, their surnames, initials and signatures.”

Not so much. However, the most common mistake in practice is the absence of the essence of the work performed or services provided in the acceptance certificate. It is not specified what kind of work was performed or service provided, i.e. the content of the business transaction itself.

As a consequence, such an act is recognized as improperly executed, expenses are deducted and additional income tax is charged.

4. Separation of responsibilities between full-time employees and hired individual entrepreneurs.

Photo from dengodel.com

A taxpayer’s mistake, which will indicate the unreasonableness (unrealism) of costs for marketing services, will be a unclear delineation or lack of delineation of the labor responsibilities and scope of work of internal specialists (for example, in this case, a full-time manager and marketer) and the responsibilities (scope of work) of a hired individual entrepreneur .

In other words, we are talking about cases where the services of an individual entrepreneur duplicate the responsibilities of full-time employees.

5. Time of conclusion of the contract. Managers, as a rule, learn that at the end of the tax (reporting) period a large profit is generated in the company and a large VAT to be paid, it is too late to plan in advance certain “material” expense transactions (or apply other systematic approaches), which could reduce these taxes. And the first thing that comes to the heads of managers is to write off part of the profit for such an “intangible” agreement for the provision of marketing or information services. The inspectors know these techniques well. Therefore, an act dated by the last day of the quarter for an amount close to taxable profit will not be ignored.

The described transactions come under the close attention of tax authorities and, if documents are prepared carelessly, can be regarded as fictitious (feigned or imaginary).

Therefore, be careful with “intangible” contracts.

Elena Sapego

Head of tax practice, lawyer, partner of the law office “Stepanovsky, Papakul and Partners”. Specialization: taxation, labor law and migration issues, commercial activities, international trade and customs law. Recommended for cooperation on the territory of the Republic of Belarus by such international directories of lawyers as Chambers Global (2004-2014), The World`s Leading Lawyers for Business (2004-2005, 2006, 2007), Chambers Europe. Europe's Leading Lawyers for Business (2007, 2009), IFLR1000 (2011, 2012). Based on the results of work in 2009, she was recognized by the Ministry of Justice of Belarus as the best individual entrepreneur providing legal services.

Olga Ivanenko

Founder, accounting tax consultant, founder of Binestart-invest.

Management experience – more than 10 years. More than 7 years of consulting experience: tax, accounting, management consulting for small and medium-sized businesses.

Methods for identifying fictitious transactions and business transactions of taxpayers

Thus, in the process of conducting verification activities or desk tax audits, tax officials check the taxpayer’s counterparties for signs of a “fly-by-night company” or their appearance in another register of companies engaged in “gray” activities (more details about “fly-by-night companies” can be found in our article “Responsibility for registering “one-day companies” and for entering false information into the Unified State Register of Legal Entities”, in which we disclosed the concept of “one-day companies” and indicated what actions the tax authorities are taking in relation to “one-day companies”). If such counterparties are identified at the audited taxpayer, the tax authorities will launch a set of verification measures against such taxpayer aimed at collecting evidence confirming the fictitiousness of transactions made by the taxpayer with such counterparties. In such cases, the actions of tax officials may be expressed as follows:

- inspection of the premises of a legal entity and its counterparties. During inspections, tax authorities identify the facts of the taxpayer’s location at his legal address, the presence or absence of space, equipment, goods, transport, etc. necessary for the execution of a fictitious transaction, as well as the presence of the director of the taxpayer’s company and employees at the workplace.

- eyewitness interviews. Tax officials often support their arguments with eyewitness testimony. In such cases, the taxpayer should pay attention to the identification of persons giving any evidence in relation to the taxpayer being audited. Often, in the inspection protocol, tax officials make mistakes in drawing up protocols, indicating only a general wording, for example: “according to employees of other (neighboring) organizations, they have not heard (don’t know) anything about the legal entity being inspected.”

- interrogations of witnesses. Protocols of interrogation of witnesses are also one of the pieces of evidence that together can confirm the legal position of the fiscal authorities. Therefore, a taxpayer intending to challenge the decision of the tax authority in court is first advised to study such documents.

- inspections, operational/investigative activities carried out by law enforcement agencies. If there are signs of tax or other offenses, law enforcement officers may be sent to the office of the taxpayer's company. In this case, a joint raid may be carried out with the tax inspectorate, or only on the initiative of law enforcement officers.

- obtaining information from banks. During this type of audit, tax authorities analyze the banking transactions of the taxpayer and his counterparties. Moreover, this analysis may also affect counterparties of the following links in the overall chain of relationships between counterparties and the taxpayer. Here, tax officials identify the chain of circulation of funds, the transfer of funds to the accounts of affiliated companies, the withdrawal of funds or their cashing through “one-day companies” or to the accounts of foreign companies (offshore).

Unjustified economic benefit from fictitious transactions

Art. 54.1 of the Tax Code of the Russian Federation contains a definition according to which a taxpayer who has underestimated his tax obligations to the budget is recognized as having received an unjustified economic benefit.

The amount of understatement does not matter in this case. The very fact of underpayment of tax (fee, contribution, etc.) is essential.

The basis for obtaining unjustified economic benefit is the fact of underestimation of the tax base due to an error or intentional actions of the taxpayer.

Thus, a fictitious transaction concluded with the aim of reducing the tax base is recognized as an unjustified economic benefit obtained as a result of the taxpayer’s prior intent.

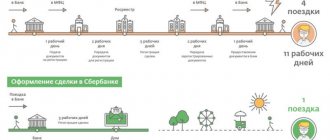

Read more about the unjustified economic benefit of the taxpayer in the infographic below:

Fictitiousness of transactions from the position of the courts

If we turn to judicial practice on the issue of fictitious transactions today, we can see that the courts have more than once drawn the attention of tax authorities to the fact that the taxpayer should not be held responsible for the dishonesty of second and subsequent level counterparties. According to the courts, the lack of good faith of all counterparties involved in the chain of transactions does not apply to the taxpayer’s exercise of due diligence, since the company, in particular each taxpayer legal entity, must be convinced only of the good faith of its direct counterparty - the transaction partner (see Ruling of the Supreme Court of the Russian Federation dated 29 November 2021 No. 305-KG16-10399, Resolution of the Arbitration Court of the Moscow District dated July 18, 2017 in case No. 40-43799/2016, Resolution of the Arbitration Court of the Ural District No. F09-3675/17 dated June 28, 2021 in case No. A76- 16418/2016).

As the courts point out, if the fact of the reality of transactions is confirmed, it is useless to refer to the most popular signs of “one-day companies”, signs of affiliation of the taxpayer and the counterparty, references from tax authorities that the director and founder of the counterparty belongs to the “mass” category due to the fact that he is also a manager and the founder of several more companies, the court rightfully declared that the location address of the legal entity indicated in the constituent documents is the address of “mass” registration and the latter is not actually located at the specified address, as unfounded, since all these facts, like the address of “mass registration” ", submission by the counterparty of accounting and tax reporting with “zero” indicators, failure to submit certificates in form 2-NDFL, documents in accordance with Article 93.1 of the Tax Code of the Russian Federation , on their own, in the absence of evidence refuting the reality of business transactions and other transactions made by the taxpayer , cannot be the basis for conclusions about the inability of the counterparty to carry out activities.”

But despite this, the courts have more than once taken the side of the tax authorities in tax disputes when the taxpayer company was provided with only an extract from the Unified State Register of Legal Entities and the constituent documents of the counterparty to the transaction as evidence of due diligence in completing the transaction. And as they say, they learn from mistakes, taxpayers began to personally inspect the premises and warehouses of their counterparties, get to know their employees, save work correspondence in electronic mailboxes, etc. And, by the way, with the participation of one of these savvy taxpayers, the taxpayer even sees fresh judicial practice, in a case where evidence of due diligence and the validity of the concluded agreement was the approval sheet for the agreement, which contained information about the counterparty including full name. representative of the counterparty, his contact phone number, email address and position. To get the green light to conclude a contract, this document had to have the signatures of the chief mechanic, deputy general director for finance, legal adviser, chief engineer and chief accountant (see Resolution of the Arbitration Court of the Ural District dated May 26, 2021 No. F09-2274 /17 in case No. A50-16250/2016).

In addition to the above, there is another example, this is the Resolution of the Volga Region Autonomous District No. F06-21881/2017 dated 07/03/2017. in case No. A12-49524/2016, in which the court indicated that the tax authority’s arguments about the fact that counterparties do not own any real estate, their own transport and employees, or the fictitiousness of transactions concluded by the taxpayer with dubious counterparties do not indicate, since they do not exclude the possibility attracting vehicles, property, employees under lease agreements, outsourcing, civil contracts, etc.

Also, regarding the facts of fictitiousness of transactions made by a taxpayer, the courts note that if the tax authorities have no other evidence of the unreality of the transactions, except for the testimony of the taxpayer’s counterparty, the arguments of the tax authorities cannot be accepted by the court. In one of these cases, the court indicated to the tax service that the facts about the fictitiousness of the transaction made by the taxpayer must be examined comprehensively. At the same time, the court rightfully pointed out to the tax authorities that the facts established during control activities, including regarding the signing of disputed agreements by the counterparty by a person who denies signing them, when the court establishes the fact of execution of agreements, the provision of actual services to the company, and the exercise of due diligence by the company, are not are an absolute reason to believe that the taxpayer received an unjustified tax benefit (see Resolution of the Moscow District Arbitration Court dated May 30, 2021 in case No. A40-208019/2016).

Likewise, contradictory information or errors in the primary accounting documents of the taxpayer do not exclude the reality of the transactions performed by him (see Resolution of the Arbitration Court of the Volga District No. F06-20557/2017 dated May 30, 2017 in case No. A12-38366/2016, Resolution of the Arbitration Court of the Western -Siberian District dated July 18, 2017 in case No. A67-4937/2015).

In conclusion, we note that, first of all, taxpayers still need to take a sensible approach to the issue of tax savings. There is also no point in hoping that the court will apply the principle of presumption of innocence in relation to the taxpayer or interpret all inaccuracies and ambiguities in favor of the taxpayer. Today, courts apply the well-known doctrine of “balance of private and public interests.” This means that if the taxpayer company is suspected of fictitious transactions or any business transactions, then the taxpayer company itself will have to prove its good faith and the validity of the transactions and operations. That is why, when concluding contracts, it is worth checking information about counterparties in good faith and in as much detail as possible, and it is advisable to record the process of collecting it. How to exercise due diligence today when taxpayers make transactions with new counterparties can be found in our article “Taxpayer Due Diligence in 2017-2018.” Currently, the topic of due diligence is very relevant in tax legal relations, especially since the times when to prove one’s good faith it was enough to request a copy of the OGRN certificate are long gone.

What are the signs of an imaginary transaction?

The main sign of an imaginary transaction is the so-called “vice of will.” This means that the parties to the transaction, despite its terms agreed on paper, do not carry out actual actions arising from the agreement. Simply put, the actions of the parties (their internal will) do not coincide with the will set out in the document - the contract.

For example, when concluding a contract for the sale and purchase of a vehicle, the buyer does not transfer money to the seller, and the car remains in the actual use of the seller. But with the help of such a transaction, you can remove the car from division, forced alienation or possible arrest, which makes this transaction imaginary - without certain legal consequences.

Legal support! Legal assistance WhatsApp +79372234028 now!

ask a lawyer online

Depending on the type of transaction and its essence, signs of sham may include:

- Lack of fulfillment on one or both sides of the transaction: lack of payment, retention of the sold property by the seller, etc.

- Mutual desire to make an imaginary transaction. If one party paid for the property, and the second refused to transfer it against the will of the first party, this is not an imaginary transaction, but its banal non-fulfillment. Both parties must understand the true purpose of the sham transaction - to create the appearance of legal consequences.

- Excessive adherence to the form of the transaction. Usually, during an imaginary transaction, special attention is paid to the execution of documents: notarization of everything that is and is not necessary; acts of acceptance and transfer, registration of contracts, etc., since sometimes documentation is an end in itself.

- Lack of documents on the execution of the transaction. The reverse side of the “excessive” execution of a transaction: if there are no acceptance certificates, financial documents and other information confirming the execution of the transaction, this is one of the key signs that it is fictitious and exists only on paper.

- The presence of at least one party (usually both) of an unlawful interest in the outcome of the transaction. For example, hiding property through a fictitious sale.

- Dependence of the parties to the transaction on each other. The sign is more typical for legal entities - common founders or employees, financial dependence, etc.

- The costs of maintaining the property sold according to the documents continue to be borne by the seller.