How to get a mortgage for a young family: registration process, documents

A family is considered young if the spouses (or one spouse) have not reached 35 years of age. There are many programs offering this segment of the population more favorable lending conditions. You can take out a mortgage as a young family at any bank in the city. Each credit institution offers its own mortgage terms, interest rates, maximum amounts and conditions. Before submitting an application, you need to find out how it is profitable for a young family to take out a mortgage. If you meet certain requirements, you can receive a government subsidy (if you do not own housing). In other cases, you can choose any program you like in one of the banks.

When submitting an application, the borrower provides documents confirming his identity, marital status, and income. Must be presented:

- The borrower's passport, which contains registration in a given region, or a passport with a document on temporary registration. Some credit institutions allow the presentation of a driver's license.

- Marriage certificate and birth certificates of children, if any.

- Help 2-NDFL. The certificate is taken at the place of work. It indicates the name of the organization, position, full name of the borrower, and income for the last year.

- A copy of the work book, certified by the personnel department. Most banks have refused this document; a certificate of income is sufficient.

The further algorithm of actions is quite simple: the borrower brings the documents to the selected bank and fills out an application, after its approval, selects a property within two months after submitting the application, buys it after making a down payment, draws up a loan agreement and insurance.

Before taking out a mortgage under the Young Family program, you need to find out whether the borrower fits into the preferential category of citizens in a given region. Many regions have social support programs for young families who do not have their own housing or have insufficient real estate (less than 14-18 sq. m per person, depending on the region). You can find out about benefits and government support by contacting the city administration, where they will tell you in detail how to get a mortgage subsidy for a young family.

What it is

The income of young families is usually low, which does not allow them to acquire their own living space and have children. Under the Young Family mortgage lending program, citizens can receive a subsidy if they need living space, and it can be directed to any areas that relate to its purchase. The federal budget finances 30%-40% of the cost of an apartment or house, the rest is paid by young families.

This program is part of a larger one called “Housing”, extended until 2021. The subsidy can only be used to purchase apartments in new buildings, that is, the Sberbank mortgage calculator 2018 does not take into account secondary housing. Therefore, the goal can be called the development of the state’s infrastructure and support for the low-income population, who have the opportunity to buy their own apartment at a relatively low price.

How to get a mortgage for an apartment for a young family: features of lending

Information on how you can get a mortgage for a young family can be easily found on bank websites or from employees of credit institutions. The process of obtaining a mortgage loan for a young family is not fundamentally different from other programs. There are specific features related to the family budget, composition, etc., for example, how to get a mortgage for a young family with a child, how to use maternity capital, is it possible to get a deferment, etc.

- Young families have a hard time finding money for a down payment. This is quite a large amount. There are now practically no mortgages without a down payment, or they have a higher interest rate and unfavorable lending conditions. Maternity capital can be used as a down payment after three years have passed from the date of receipt of the certificate. Almost all credit institutions accept such certificates.

- After the birth of a child, a young family who has received a mortgage can receive a deferment. Such benefits are practiced by many banks. After the birth of a child, the borrower brings the birth certificate to the bank and receives a deferment for 3 years, during which he pays only interest.

- The loan and subsidy can be used to purchase any type of housing: a house, an apartment on the primary or secondary market, housing under construction. Before you take out a mortgage on a house for a young family, you need to calculate your budget, income and monthly payments. The amount issued by the bank is limited.

- After the birth of a second child, a young family can use maternity capital to pay off interest and debt. You can use the certificate immediately after receiving it, without waiting for the three-year period to expire.

- After purchase, an apartment under the “Young Family” program is registered in the name of both spouses. The second one is a co-borrower. In the event of a divorce, the apartment remains the property of both spouses, but one can buy out the share of the other with his consent.

Required documents

Before you go to the bank and request a loan for a young family, you should prepare a list of documents that are standard for a regular mortgage. The papers are submitted to the municipal authority for inclusion in the “Young Family” mortgage program. The list of documentation includes:

- application for inclusion in the program;

- copies of passports of adult family members or other identification documents;

- papers on collateral property, that is, an apartment that the newlyweds plan to rent;

- a copy of the work record book, which reflects at least 6 months of experience at the current place of work;

- income certificate, which indicates the monthly profit, as well as the seals and signatures of the responsible persons of the enterprise;

- documents for the housing being purchased;

- papers stating that the down payment can be financed;

- copies of marriage and birth certificates;

- certificate of absence of own housing.

sample application for subsidy

Note! Additional paperwork may include the need to prove the absence of utility debts in order to confirm solvency and reliability.

How to get government support for a mortgage for a young family

State support allows families to receive free subsidies for the purchase of housing.

Subsidies to a young family who have taken out a mortgage on an apartment are given if they have received the status of a preferential category of the population. First, you need to find out about the availability of such benefits in a certain region, the conditions for participation in the program, then submit the appropriate documents and get in line for housing.

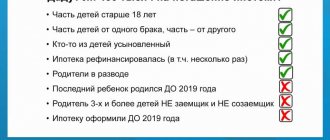

Participants in the program can include people under 35 years of age, officially married and in need of improved housing conditions. Housing conditions are considered non-compliant if there is less than 18 m2 of space per family member, if there is no real estate in the property at all or if it does not meet housing standards (non-residential premises, no amenities, the building is in disrepair, etc.).

Low-income and large families fall into a separate category. They are entitled to more lenient lending conditions and certain government assistance. Single-parent families with children can also participate in the program.

To become a participant, you must document your status as a person in need of housing. For this purpose, a certain package of documents is collected, extracts from the house register, certificates of family composition, the condition of housing, etc. These documents are presented to the administration in the department dealing with housing issues. There you can write an application, receive a program participant certificate and get on the waiting list for housing. With this certificate you need to contact the AHML branch (Agency for Housing Mortgage Lending), which deals with such mortgages.

As a result of participation in such a program, you can receive a subsidy in the amount of 35% of the cost of housing, as well as an additional 5% for each minor child.

For information on how to get a social mortgage for a young family, you can contact the city administration, and then any bank.

Most often people are interested in how to get a mortgage for a young family at Sberbank, since it is the largest bank working with government support. If you wish, you can choose any other bank that deals with social mortgages.

Requirements for participants

Since we are talking about supporting families financially, clear criteria are established for who is eligible for this; how to get a mortgage for a young family will depend on them. The legislation states that youth should be considered people who are under 35 years of age, and a young family is citizens of Russia who have entered into an official marriage and have not reached the specified age. Also, a family can have one or several children, and if the parent is a single parent, then the status of a young family also applies to him.

Other requirements of the program related to mortgages for young families include:

- the spouses live together, which is confirmed by documents;

- they have an official job that will allow them to repay the loan;

- per person there is less than 18 sq. measures of living space, and incomes are at

- level below the regional subsistence level;

- the current housing may be in disrepair, but this must be confirmed by a special conclusion from the municipality;

- a family can have many children and receive maternity capital.

Various bank programs according to the number of children in the family

As for the childless, it can be noted that if you participate in a subsidized program, you can receive 35% of the cost of housing from the state, but with the appearance of a baby in the family, the amount increases to 40%.

Banks offer low interest rates. Some may deduct a percentage depending on the number of children. If it is one child, then 0.25%, and if there are two or more – 0.5.

Banking organizations also provide holidays, i.e. you don’t have to pay the loan until the child turns 3 years old. Of course, not all institutions can afford this, so it is better to check this information with a bank employee.

Families with two or more children can use maternity capital for full repayment and to pay monthly payments.

In 2021, for large families, the loan rate does not exceed 8%, and in some banks with government support it is 6% per annum.

Mortgage comparison table

| Type of preferential mortgage | Program content |

| With government support | A specific feature is the possibility of repaying part of the loan with funds from the federal budget. The mortgage is issued at a low interest rate, which eliminates overpayments. Previously, such a loan was issued only for categories of citizens who especially need additional social protection (disabled people, low-income people, large families), but from 2021, persons from 18 to 60 years old who have a permanent source of income are allowed to participate in the program. Down payment – 20% Loan term – up to 30 years Interest rate – 12% |

| For a public sector employee | The project involves doctors, teachers, military personnel, whose maximum age is 35 years, employed, and with at least 1 year of work experience in the field in question. |

| For young professionals | A mortgage loan for building a house or purchasing an affordable apartment is provided to scientists, doctors, teachers no older than 35 years old, working in municipal or government organizations. Project specificity – you can invite 2 borrowers when issuing a loan |

| For young scientists | Researchers, candidates and doctors under the age of 35, current employees of the Russian Academy of Sciences and the Russian Academy of Medical Sciences, if they have worked at their place of employment for at least six months, can become participants in the program. |

| Army | Military personnel who signed their first contract after January 1, 2005 are eligible to participate. |

| Project "Young Family" | Participants are a couple not older than 35 years. Requires formal employment and availability of funds to cover monthly payments |

Consequently, in Moscow and the region, young families can purchase their own housing at an affordable price thanks to several types of mortgage lending. Candidates will be presented with a specific list of criteria, compliance with which will allow them to quickly collect documents and participate in one of the programs proposed by the constituent entity of the Russian Federation.

About mortgages in Sberbank

Basic information is contained in the special law “On Mortgage”. You can read about Sberbank’s mortgage programs on the official website in the “Mortgage” section.

The person who takes out the mortgage is called the borrower. There may be several borrowers. Spouses, as a rule, take out a mortgage for two. There may also be co-borrowers - people who, among other things, will repay the mortgage and whose income will be taken into account when determining solvency. For young families, co-borrowers can be the parents on the wife’s and (or) husband’s side. This makes it easier to get a mortgage.

Also know that according to the law, the person who took out a mortgage must insure the subject of the mortgage: an apartment or a house (Article 31 of the Law “On Mortgage”). Therefore, be prepared for additional costs.

Young Family Program

Let us clarify right away: Sberbank does not have a separate mortgage loan for young families. There are loans for everyone and there is a “Young Family” condition (hereinafter referred to as “MS”) - a small bonus that applies to such borrowers. A married couple under the age of 35 is eligible. The fact of marriage registration is mandatory, but its date is not important.

“MS” does not apply to all mortgage programs, but only to three:

- purchase of housing under construction;

- purchase of finished housing;

- construction of a residential building.

At the time of writing, the rates on the above loans were 7.5%, 9.7%, 10.6%, respectively. When “MS” is applied to these loan programs, the interest rate is reduced by 0.5%. Other lending conditions remain the same as for all clients. Condition “MS” is a temporary promotion, the duration of which is from 01/01/2016 to 12/31/2018.

It is possible that the promotion will be extended. But as bank employees said, they do not yet know about plans for 2021 - they only have information on existing loans. News - after the New Year.

For young families, Sberbank has another bonus - deferment of loan repayment upon the birth of a child until he is 3 years old. It also works if there are several children, but the maximum deferment period is 5 years. Due to the deferment, the loan repayment period simply increases. To apply for it, you need to write an application at any Sberbank mortgage lending office.

When the first child is born, they give a delay of 3 years. After 2 years, the second child was born - 2 years are added to the deferment, not three (for a total of 5 years).

Maternity capital can be used to pay off some loans.

Video: mortgage in Sberbank

What affects the interest rate

Sberbank has a set of general conditions that affect the interest rate (in your favor or in favor of the bank) . These conditions are also relevant for young families, since they always apply, even along with “MS”.

One of the main factors is the amount of the down payment. The bank likes it when it is more than 50% of the cost of housing. So he is sure that you will repay the loan, and therefore reduces the interest rate. How much is calculated individually, depending on the type of housing, cost, and loan term.

If you receive your salary on a Sberbank card, then it is aware of your financial affairs - it is easy for it to check the level of your income. Thus, the bank is confident in your solvency, which means it will be more willing to give you a loan. If the salary comes to the card of another bank (or is issued in cash), then Sberbank will ask you to confirm your income with a 2-NDFL certificate from your employer or a certificate in the bank’s form. Without this confirmation, the mortgage interest rate will increase by 0.3%.

Sberbank has it. Real estate transactions (including the purchase of housing with a mortgage) must be registered in a special state. authority - the Federal Service for State Registration, Cadastre and Cartography (hereinafter - Rosreestr), as stated in Art. 22 of the Law “On Mortgage”. Rosreestr enters information about the new owner of the apartment and that there is a mortgage on the apartment into the Unified State Register of Real Estate (USRN). Usually you handle this paperwork yourself. First, sign a loan agreement with the bank, submit it along with the registration application to Rosreestr, and pay a fee of 1,000 rubles. (Clause 28, Clause 1, Article 333.33 of the Tax Code), wait until everything is processed, pick up the documents from Rosreestr and take them back to the bank. Of course it takes time. That's why Sberbank came up with it. Its essence is as follows: at Sberbank they assign a manager to you who will deal with the issue of registration. He himself will send the documents to Rosreestr (electronically) and make sure that everything goes according to plan. After registration, Rosreestr will send you and the bank an email with a registered mortgage agreement and an extract from the Unified State Register of Real Estate. Faster, more convenient and no worries. If you used “Electronic registration”, then Sberbank also reduces the mortgage rate by 0.1%. But there is such a nuance that the service is paid - 5,500 - 10,250 rubles. The cost depends on the chosen housing and the region of the Russian Federation. In addition to the work of the manager, it includes the payment of state fees and the creation of an enhanced qualified signature necessary for electronic document management.

If you have life insurance, the rate is 1% less, without insurance, the rate is one percent more. Why the bank needs insurance is understandable. This is a guarantee that the lender will receive his money in any case: when you are alive and well - from you, if something happens to you - from insurance payments. You can get insurance from the Sberbank insurance company (Protected Borrower program) or from a company with which Sberbank is friends. Naturally, the service is paid. The cost depends on:

- insurance company;

- loan amount (the larger it is, the higher the insurance premium);

- gender (insurance is more expensive for men);

- month and year of birth (the younger, the lower the insurance premium);

- health status (if there is oncology, cirrhosis, coronary heart disease, disability of 1, 2 or 3 groups, there was a stroke or there is a referral for a medical and social examination, then insurance will not be issued).

Example: a young family takes out a loan of 300 thousand rubles. Both spouses were born in 1996. The insurance premium, depending on the month of birth, is equal to: for a man 1195 (January) - 1095 (December) rubles, for a woman - 924 (January) - 903 (December) rubles. And if they take out a loan of 4 million rubles, the insurance is as follows: man 14920 (January) - 14600 (December) rubles, woman - 12320 (January) - 12040 (December) rubles. If you do the math, paying for insurance every year is cheaper than giving it up. In case of refusal and a loan of 300 thousand rubles. you will give the bank another 3,000 rubles annually, with a loan of 4 million - 40 thousand.

You can calculate the cost of insurance online by entering your data

Sberbank removes 0.3% of the rate if you use the Domklik portal to select an apartment. You are automatically taken to this site from the Sberbank website when you begin to find out details about the mortgage program you are interested in. Domklik collects information about housing that Sberbank has checked (there is data from Rosreestr that the property is in order: registered, there is an owner, documents have been drawn up). The bank considers such a transaction reliable, and therefore reduces the rate.

Mortgage conditions for a young family

Let's briefly talk about the three mortgage programs that are subject to the MS condition. Remark: speaking about the interest rate, we will proceed from the fact that:

- there are no allowances, i.e. the salary comes to the Sberbank card, life is insured, we used “Electronic registration”, housing is available on the Domklik website;

- the “MS” condition applies (i.e. minus half a percent of the “total” rate).

New building

A loan under the “New Construction” program is given when a family wants to buy housing that is still under construction. Pros: relatively low loan rate, ability to use maternity capital. Disadvantages - there is no guarantee that the house will be completed at all and completed on time, repair costs are obligatory.

Mortgage conditions for housing under construction:

- minimum loan - 300 thousand rubles;

- maximum loan - 85% of the cost of housing;

- minimum down payment - 15% of the cost of housing;

- mortgage term - up to 30 years;

- interest rates for a young family are from 7 to 9%.

A special feature of this loan is a special subsidy program. Its essence: Sberbank has construction partner companies throughout Russia. If you buy an apartment from the companies listed in the list, the interest rate will be lower. Which one depends on the loan term: less than 7 years - 7%, from 7 years and 1 month. up to 12 years - 7.5%. Moreover, the construction itself can last longer than 12 years.

If you do not participate in the subsidy program, the rate will be 9%. The mortgage is not limited to 12 years, but can be issued for a maximum period.

Ready housing

The main advantage of a mortgage on finished housing is that it has already been rented out. Another plus is that you can use maternity capital. The downside is that the rate is higher than for an unfinished building (but lower than for a house).

In the case of finished housing, Sberbank reduces the mortgage rate by 0.3% if you choose an apartment for purchase on the Domklik portal. On the website, this opportunity to reduce the rate is called the “Showcase Promotion”.

Domklik allows you to select a proven apartment both on the secondary market and in a new building

The conditions of the “Ready Housing” mortgage program are as follows:

- minimum loan - 300 thousand rubles;

- maximum loan - 85% of the cost of the apartment;

- minimum down payment - 15%;

- period from 1 year to 30 years;

- rates: with the “Showcase” promotion - 9.2%, without the promotion - 9.5%.

My house

The conditions for the “Own Home” loan are more severe: the highest interest rate, there is no possibility of using maternity capital, the maximum loan amount is lower, and the down payment is larger. But in the end, the plus is your own home.

Conditions:

- minimum loan - 300 thousand rubles;

- maximum loan - 75% of the cost of the house;

- minimum down payment - 25%;

- period from 1 year to 30 years;

- The interest rate for a young family is 10.1%.

Other support

Families in the Russian Federation can receive other payments that should help them implement mortgage programs for young people and ensure comfortable living. For the second child and each subsequent child, maternity capital is paid at the level of 453 thousand rubles; it can be used to partially repay the mortgage or the first payment.

The state is entitled to a one-time payment of 15,382 rubles, which is issued within six months from the date of birth of the child. Governor's assistance is given to families under 30 years of age, but the amount depends on the region, and documents will require children's birth certificates, an application, an identity card and bank details.

Additionally, if there are three or more children in a family, it receives the status of a family with many children, but mortgage support is not provided. Instead, a number of benefits are provided, including a discount on housing and communal services, partial exemption from taxes, as well as assistance when starting a business or building a house.

Young families in Russia can get a Young Family mortgage loan from Sberbank to purchase their own home and ensure comfortable living conditions. It is issued to both people with and without children, but the main criteria are being under 35 years of age and having an income that allows you to pay monthly amounts.

Related Posts

- Social mortgage for low-income families What is it Social mortgage mortgage for low-income families is a loan product that is issued…

- Assistance program for mortgage borrowers Unfortunately, not all borrowers who take out a mortgage to purchase a home have financial stability…

- Mortgage for a garage Among residents of city apartments, the issue of vehicle placement is acute. Some people prefer to leave the car at…

- Mortgages for large families: new law 2021 Such support for citizens as mortgages for large families is providing the opportunity to acquire their own housing and...