3.2 / 5 ( 5 votes)

When dividing common property between ex-husband and wife, the question of repaying the remaining debt on a loan or credit now very often comes up. There are two difficulties in solving this problem. This is the procedure for determining the total debt and the procedure for agreement with the bank. Judges here are guided by articles of the RF IC, the RF Civil Code, the RF Tax Code, and a number of federal laws and regulations. Of great importance, in particular, are the internal documents of credit institutions, according to which borrowed funds are provided to clients.

General debt obligations

The RF IC determines that in the event of a divorce between spouses in 2021, not only joint property, but also debt obligations will be divided. Art. 39 indicates how this distinction occurs: when dividing common property, the court determines the size of the shares that are intended for each of the spouses. The total debt obligation is distributed in accordance with them.

The main problem is the difficulty of determining which debt is considered common. This is because their sources of origin can be completely different. Most debts are a consequence of loan agreements. And their subject-object composition can vary significantly:

- one spouse acts as a borrower and takes funds for his personal needs;

- the borrower is one of the spouses, the loan is issued and spent on general needs;

- the loan is issued to both spouses (or one of them acts as a guarantor);

- the loan is issued to one of the spouses, and the co-borrower is one of the family members, but not the second spouse, etc.

The condition of the loan agreement is joint liability between the borrowers or between the guarantor and the borrower. And such a rule sometimes conflicts with Art. 39 of the RF IC on the distribution of debts according to shares. Therefore, each court decision on such issues is made only after careful study of the opinions of lenders, borrowers and guarantors. If the judge makes a verdict that contradicts the loan agreement in terms of further repayment, the bank can challenge the decision in a higher court.

Let's consider what debt will be common to a husband and wife. The decisive factor in the determination is the purpose for which the loan or credit was issued. If money was taken and spent on the needs of the family, then it is classified as general debt obligations.

If the loan agreement specifies the purpose of purchasing household appliances, furniture, vouchers for a family vacation, etc., then these are joint needs. They should also include paying fees for the education of joint children or purchasing personal property for them.

In 2021, not only a loan agreement, but also sales receipts, vouchers, and the presence of the item itself in family ownership can serve as evidence of the existence of a common debt between spouses.

Court decisions

Divorce proceedings: How to bring ex-spouses to a settlement agreement

How to reduce alimony and divide property during a divorce

Divorce and all the ensuing consequences: what difficulties may arise during the divorce process?

When dividing property, the court left the wife an apartment purchased during marriage

Claim for communication with a child

How to return an illegally sold apartment

Personal debt of one of the spouses

When dividing property through the court, only shares in the common property are distributed. This rule also applies to debt during a divorce, i.e. personal debt will not be divided by a court decision.

Some difficulty arose earlier with the definition of personal debt. If it was registered before marriage, it automatically fell into this category. This fact can only be challenged in court, provided that during the marriage the loan was repaid from the general family budget.

But it happens that a loan is issued only by one of the spouses for personal needs. Even the purchase of a car can be considered such if the second spouse did not give his consent to receive borrowed funds from the bank. Previously, the burden of providing evidence that the money received was not spent on family needs was placed on the non-borrower spouse who wants to challenge the division of personal debt between spouses in 2021.

However, the Supreme Court of the Russian Federation, making a decision in the case of division of debts, noted that not all debts incurred during marriage are divided in half. Because when dividing property it is necessary to rely on Art. 39 of the RF IC, which establishes the principle of equality of shares, but it does not say anything about debt obligations. The legislation of the Russian Federation provides that each spouse may have their own obligations to creditors. The Supreme Court found that the common debt of the spouses is recognized as such only if a number of conditions are met.

If it is issued to only one of the spouses, then it must be accompanied by circumstances arising from Art. 45 RF IC. It establishes that a debt is declared common if it was taken out and fully spent on the needs of the family. Moreover, the burden of proof falls on the shoulders of the person who wishes to share it. Those. if the borrower is the wife, then in the event of a trial it is she who must prove that the funds were spent on the acquisition of common property of the spouses or other joint needs.

Customer Reviews

Gratitude from Elena and Alexander I sincerely thank lawyer Vasily Anatolyevich for his qualified and polite service. We will always contact you and tell our friends. Thank you.

Elena

Alexander 998-98-59

Gratitude from Vraveevsky S.A. Sergey Vyacheslavovich! Thank you very much for the consultation! All the details were disclosed to me in detail, all questions were answered comprehensively. I am very glad to receive help from a qualified specialist!

Vraveevsky S.A. 12/18/2018

Review by B.I. Goreky Gratitude to Yuri Vladimirovich from B.I. Goreky for the consultation on family rights.

Gratitude from Rusanova N.V. I sincerely thank Konstantin Vladimirovich Ivanov and Sergei Vyacheslavovich Mavrichev for the qualified information assistance provided in a friendly atmosphere of communication, as well as for providing the opportunity to obtain guaranteed legal support in the future.

Rusanova Natalya Viktorovna, Associate Professor of the Department of Russian Language and Literature of St. Petersburg Mining University.

Thanks to Pavlyuchenko A.V. from Astafieva A.S. I express my gratitude to the Legal Agency and in particular to lawyer Alexander Viktorovich Pavlyuchenko for the work done, high qualifications and high-quality approach. Thanks to Alexander Viktorovich, we managed to achieve a result in court in a case on the protection of consumer rights that I did not even expect. The amount recovered in court even exceeded my expectations. Thank you very much for your qualified work and professionalism.

Sincerely, Astafieva A.S., 03/01/2019

Gratitude from Potapova T.I. I express my gratitude to Denis Yuryevich Stepanov for the work done, high qualifications, as well as for very clear, accessible help in solving my problem (protection of consumer rights). Excellent, very competent lawyer. Thank you very much!

Sincerely, Potapova Tamara Ivanovna, 07/09/2019

Gratitude from Truk N.N. I would like to express my gratitude to Vasily Anatolyevich Kavalyauskus, Alexander Viktorovich Pavlyuchenko and Maxim Andreevich Lobur for providing qualified legal assistance, with the help of which my problem was resolved quickly and clearly. When contacted, I always found understanding and attention. It’s good that the “Society for the Protection of Consumer Rights” employs such lawyers and advocates. I wish you success in your future work and defending the interests of consumers.

Sincerely, Truk N.N.

07.05.2018

Thanks to Pavlyuchenko A.V. from Sonets V.V. I express my deepest gratitude to Alexander Viktorovich Pavlyuchenko for the consultation and competent approach to the matter, as well as the successful outcome in my problem. I also want to express my gratitude for your kindness. I wish you success in this work that is necessary for us.

Sincerely, Sonets V.V. 05/17/2018

Gratitude from Bolotin V.S. I thank Alexander Viktorovich Pavlyuchenko for the work done as part of the investigation into the administrative case. I am especially grateful that almost all activities within the framework of the case were carried out by Alexander personally, without my involvement, which significantly saved my time. I would also like to note the efficiency with which the work was completed. I would like to wish Alexander further success in his professional activities and the successful completion of all current and subsequent cases, restoring justice to his clients.

Bolotin V.S., 02/12/2017

Gratitude to Sukhovarov I, Dmitry Vladimirovich Korchagin, express my gratitude and appreciation to lawyer Yuri Vladimirovich Sukhovarov for high-quality and qualified advice. Thank you.

Fictitious debt when dividing property

To reduce the share of the other party in the common property, some unscrupulous spouses use such a prohibited technique as creating a “fictitious debt.” For example, a husband or wife in collusion draws up a loan agreement retroactively, and indicates general needs as the purpose of receipt.

What is fictitious debt and how is it distributed between spouses during a divorce?

In this case, the injured party will have to act. Firstly, if a fictitious loan agreement is suspected, it is necessary to insist on an examination in order to determine the period of its actual writing. Secondly, an examination of the financial condition of the married couple at the time of the theoretical loan application may be necessary. Thus, the level of income must be determined in order to determine whether the conditions for obtaining a loan are met.

If the creditor is not a banking structure, then it is necessary to establish the existence of a connection between the “lender” and the second spouse.

If the injured party fails to prove that the loan is fictitious, then the division of debts in 2021 will end with the fact that they will have to answer for them with the common property.

How are spouses' debts divided?

If the common debts of the spouses are divided through the court, then three solutions are practiced:

- The division of joint debt is carried out in proportion to the shares of property distributed between the spouses. Typically, this principle implies equal amounts.

- When dividing debts, the opinion of banking specialists is taken into account, who give their consent to the distribution of debt between spouses. Thus, the number of borrowers in a monetary obligation may change upward or downward. For example, the second spouse is subsequently excluded from co-borrowers with the payment of funds as compensation.

- The court, at the insistence of the creditor, makes a decision to refuse to divide the debt obligations of the spouses if there are other co-borrowers under the loan agreement.

Debts that cannot be divided

When dividing debts between spouses, those debts that arose as a result of one spouse receiving a loan will not be taken into account, provided that the second did not act as a co-borrower and did not give his consent to the processing.

Also, debts on loans issued before marriage are not divided if the other party does not claim part of the property acquired with the funds received.

Also, debts arising after the actual termination of joint life and management of a common household by spouses are not subject to division. Even if during the registration period they officially retained the status of husband and wife.

Bank loans section

The difficulty of dividing general debts on bank loans is that without the approval of the bank, the procedure is problematic. Those. the judge, of course, can make a decision, but if it does not satisfy the credit institution, then the latter can easily challenge it.

Should the first spouse be responsible for the personal loans of the second?

Not really

As a rule, banks insure themselves by initially including in the contract a clause for dividing the debt in the future in case of divorce. He will have to follow the sides. But if there is none, then the following division methods become possible:

- the debt is transferred to one of the spouses;

- then both spouses continue to pay the debt together;

- the loan agreement is restructured, drawing up two accounts. Next, each spouse pays their portion separately.

What types of debt liability are there?

Joint obligations

General debt includes loans and other debts that were taken out before or after the official registration of marriage:

- By a wife or husband in order to spend borrowed funds on family needs.

- In a loan agreement or under a promissory note, under which both spouses or the bride and groom act as the borrower before entering into a marriage.

Such debts include, for example:

- Loan for wedding celebrations.

- Loan funds for a vacation trip.

- Loan for the purchase of a car.

- Financial resources borrowed for a child’s education at a university.

Personal debts

Personal debts, for which each participant in the marriage is liable independently according to the law, include:

- Monetary penalties and fines imposed on one of the participants in a marriage relationship in connection with the commission of an administrative or criminal offense.

- Credit funds transferred by one of the spouses as payment for transactions of a personal nature, for example, contracts for the provision of medical or educational services.

- Debts that were incurred before the official registration of the marital relationship.

- Borrowed money to meet personal needs or to reconstruct or improve personal property that is legally impossible to divide. This could be, for example, improving the RAM or video card in the husband’s personal computer, which he uses for computer games.

Personal debts also include loans taken out by cohabitants living in a civil marriage. The fact is that Russian family legislation does not recognize any other form of marriage other than one registered in the prescribed manner with the civil registry office. Therefore, cohabitees are not subject to the provisions of the Family Code on the joint property of a wife and husband.

Loans with and without guarantee

If a wife and husband enter into a loan agreement with a credit institution, in which one of the spouses acts as a borrower and the other as a guarantor, then this debt is recognized as joint. It does not matter when the loan transaction was executed: before the registration of family relations or during legal marriage. Upon dissolution of the family union, this common debt must be distributed equally between the spouses, unless they have established other conditions for the division of credit debts in the marriage contract.

As for credit obligations without a guarantee, possible options for dividing the common debts of spouses are indicated in the table.

| When was the loan taken out? | How debts are divided between spouses |

| Before registering a marriage relationship by one of the future spouses | There is no division of debts, since the debt of one of the former spouses, acquired by him before the official registration of family relations, is considered personal. |

| Before marriage, jointly by the bride and groom | The division of debts of spouses intending to divorce occurs according to one of the following options:

|

| Married by one of the spouses | Recognition of debt as general or personal depends on the purposes for which financial resources were required:

|

| In a marriage, two participants in the marital relationship jointly | The debt is considered joint and is divided equally or on the terms specified in the marriage contract or agreement on the division of property. |

Mortgage

If the spouses decide to divorce and divide the housing purchased under a mortgage agreement, then a banking organization must take part in the divorce process.

As a rule, if a couple does not have a minor child, the bank insists on one of the following options for dividing the debt during a divorce:

If the banking organization is confident that both former spouses are solvent and can continue transferring funds to pay off the mortgage in the future, then it is possible to divide the total debt into the husband’s debt and the wife’s debt during a divorce. This is achieved by concluding separate mortgage agreements with each spouse.- If the spouse did not earn money during the marriage and did not take part in reducing the amount of the mortgage debt, then when dividing joint assets, she may lose the right to real estate, even though she was a co-borrower under the agreement. The bank will release the ex-wife from paying the mortgage loan, since it will consider her insolvent, and will sign a mortgage agreement with the ex-husband. In this case, the mortgage debt will be included in the husband's personal debts in the divorce.

- Banking organizations that do not want to take risks are pushing through in court the option of selling the residential premises, after which the mortgage is repaid in full if the proceeds are sufficient for this, and the rest of the money is divided between the spouses in half or in another manner established by their agreement.

If a married couple has a minor child who is being cared for by a wife who is on maternity leave to care for him, then the judicial authority involved in the divorce process must take into account the child’s housing rights and the property status of his mother. Therefore, if the spouses do not have any other housing, or it is worse than the apartment purchased with a mortgage, then the court may refuse to repay the debt by selling the home to the representative of the banking institution.

Based on the analysis of judicial practice, in most cases judges act as follows:

- The child and the parent who is directly raising the child are allowed to live in residential premises taken on a mortgage.

- Mortgage debt is divided between the parents. The banking institution enters into a separate mortgage agreement with each of the former spouses. Typically, the parent with whom the children remain is awarded a smaller portion of the debt. The issue of dividing the debt into specific shares is decided in each case by the court individually, depending on the circumstances of the case.

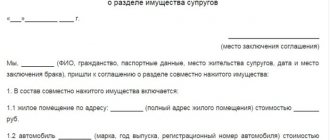

Statement of claim for division of debts

Each spouse has the right to file a claim in court for the purpose of dividing common property and debts. The claim is drawn up according to the standard rules set out in Art. 131 Code of Civil Procedure of the Russian Federation. It must indicate:

- name of the institution where it is provided;

- basic passport data of the parties;

- the main essence of the claims with reference to existing laws that confirm the validity of the claims;

- approximate calculation of the amount of debt.

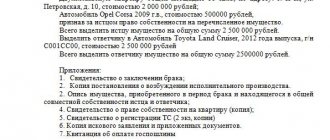

The claim must be accompanied by a package of documents that can serve as the basis for the plaintiff’s case, as well as copies of loan agreements and civil passports of both parties.

On our website you can.

Evidence supporting debt obligations

It is not difficult to collect evidence for the division of common debts if you initially treat all payment documents with care. It is they, after the loan agreement, which indicates the purpose of the loan, that are the main evidence. The very presence of common property is also such. For example, a couple has new furniture in their apartment, the cost of which does not allow them to be purchased immediately using funds from their shared income. In this case, an analysis of the family’s financial situation will be taken into account as evidence. It is done on the basis of income certificates (2-NDFL, 3-NDFL, etc.).

Counterclaim

The division of debts by spouses through the court may be significantly delayed if additional examinations are needed during the hearing and subject to the filing of a counterclaim by the defendant. A party can do this at any stage of the case. The document is drawn up according to the same rules as the main claim. Most often, the reason for filing is the unwillingness to answer for the personal debt obligations of the second spouse.

How to arrange everything correctly

Due to the fact that the marriage contract and agreement on the division of assets are notarial documents, notaries have their forms, and spouses can fill out these documents in the notary office.

As a template for filling out yourself, you can download a sample marriage contract from here, a sample agreement on the division of property - here.

Before drawing up a statement of claim, you must familiarize yourself with the one hundred and thirty-first article of the Civil Procedure Code, which determines the content of this document.

In order to simplify the writing process, use a sample statement of claim, which can be downloaded from here.

Arbitrage practice

Over the past two years, court decisions on the issue of division of common debts have changed significantly, thanks to clarifications of the RF Supreme Court on the inadmissibility of universal recognition of common liability for loans issued to one spouse.

Now the judge, when considering the case, requires evidence that the funds received from the loan were entirely spent on general family needs.

To divide common debts in 2021, former spouses can resort to the help of a court or reach an amicable agreement among themselves.

How is the amount of debt determined in a divorce?

The amount of debt to be paid by each former spouse can be determined by the methods indicated in the table below.

| Debt separation method | In what cases is it used? |

| Marriage contract | It can be concluded before registering family relations or during marriage. In the marriage contract, spouses can specify at their discretion not only the rules for the division of common material assets, but also the division of loans. |

| Property division agreement | It is drawn up by the spouses jointly at the stage of the divorce process until the final decision of the court is made. In legal terms, the agreement is similar to a marriage contract. The difference from a prenuptial agreement is that a prenuptial agreement is certified by a notary, and an agreement on the division of assets, if considered in court, must be approved by a court decision. In addition, before making a decision, the judge checks the wording of the agreement for compliance with Russian legislation and makes sure that it does not infringe on the property interests of the wife or husband. |

| Trial | In order to determine the amount of debt obligations of each participant in the marriage union, the judicial authority must determine:

|