Reasons for the need to divide property between the founders

The division of property between the founders is a multi-stage process that occurs as a result of certain circumstances. Most often it is a consequence of:

- Liquidation of the company;

- Divorce of spouses;

- Withdrawal of the founders from the enterprise.

The circumstances resulting in the division of property between the founders determine the course of the procedure; in addition, the participants of the event take into account the requirements of the law. To avoid violations of legal norms, it is better to use the services of professionals during the division process.

Tax and section in general

What taxes in general relate to the division in one way or another? After all, there are several dozen of them in the Tax Code. Should spouses, in principle, pay any taxes in connection with the property they receive as a result of division of jointly acquired property?

INUSTA

The Russian Ministry of Finance believes that the personal income tax established by Chapter 23 of the Tax Code of the Russian Federation is relevant (letter dated March 15, 2021 N BS-4-11/4624). This opinion was expressed by the ministry in March 2021. Previously, the ministry had no opinion on the issue, and state authorities were not interested in the division of property in principle. Read about this in the article: For the division you need to pay a tax of 13%. Innovation of the Ministry of Finance of the Russian Federation on property agreements.

Briefly, the officials' statement boils down to the following. When the division of property - apartments and other real estate - is carried out by former spouses, that is, after a divorce, and this is done without court through the conclusion of an agreement on the division of property, then in some cases a tax base may arise. In particular, if the property is not divided equally. For example, if, by agreement, the marital apartment becomes the property of only the ex-wife, and the other does not receive anything, half of the cost of the apartment will be the tax base and the ex-wife must pay 13% of this amount, because this will be her income.

Thus, according to officials, personal income tax is imposed on that part of the property that, under an agreement on the division of property, is transferred to the former spouse and which exceeds half of what is being divided.

Another tax concerns the division of property of spouses, both before divorce and after dissolution of marriage - this is a state duty regulated by Chapter 25.3 of the Tax Code of the Russian Federation. True, it should also be called conditional, since it is paid in connection with filing a claim in court for the division of property or in connection with the registration actions of Rosreestr.

Thus, one way or another, the division of property of a husband and wife concerns only one tax - personal income tax.

Division of property between founders during the period of liquidation

Liquidation is the complete legal cessation of an organization’s activities. The process consists of several stages, at one of them it is important to draw up a liquidation balance sheet, which contains information about all the assets of the organization, current and non-current assets, its capital and liabilities.

In the division of property between the founders, the liquidation commission takes an active part, which objectively evaluates and carries out the division taking into account the size of the shares. This approach ensures that the division issue is resolved without scandals between the founders.

The process of dividing property involves its transfer from a legal entity into the hands of individuals (founders). It consists of two successive stages, carried out in accordance with the norms and regulations of the law:

- Division of monetary assets between participants;

- Division between the participants of the enterprise's fixed assets, taking into account the volume of investments of each.

The division of fixed assets between owners can occur in kind or in cash. The first method involves the transfer of parts of the enterprise, taking into account the volume of shares. To receive fixed assets in fact, you must have a proprietary right to them, as a basis for transfer, for example, ownership. The transfer of equipment takes place according to a transfer deed.

If the monetary method is used for division between the owners, then initially the objects are sold, and then, from the profits received, the obligations are repaid and the remainder is divided between the participants in proportion to the shares of each. If there are assets in the accounts, an order is sent to the financial institution to issue them, the basis being “return of contributions to the authorized capital.”

Note: if the company is liquidated through reorganization, then the described method of dividing property between the founders is impossible.

How is the value of actual LLC objects determined?

If there is a large amount of material assets, an assessment is carried out by independent experts during the period of settlement with creditors before the formation of the liquidation balance sheet. The liquidation commission is required to initiate such an assessment.

Authorized experts conduct an inventory of existing property, determine the suitability of the funds and the degree of their wear and tear. The price of fixed asset balances is determined by the residual book value on the day of complete liquidation of the enterprise. If the amount received does not reflect the real market price of the property, an independent appraiser is additionally involved in the issue.

We help divide the property of the founders.

We have lawyers with over 20 years of experience.

+7

Taxation of division of property between founders

The division of property is taxed in the same way as other profit-generating transactions. According to Art. 209 and 210 of the Tax Code of the Russian Federation, a person who has received income must necessarily pay income tax; the receipt of profit in the liquidation process is regulated by Art. 23 Tax Code of the Russian Federation.

In this case, tax is deducted only from income; compensation for the amount of shares is not considered as such.

When to pay personal income tax when dividing property between spouses during the divorce process: the position of the Ministry of Finance

To answer this question, it is necessary to determine the method of division of property, as well as the stage.

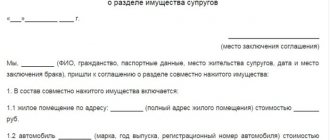

Paying taxes on property division agreements before and after divorce

Property can be divided by concluding an agreement before the divorce. To do this, the spouses negotiate among themselves what exactly will become the property of each of them. The completed agreement must be certified by a notary. Otherwise, the document will not have legal force.

The agreement must specifically state what each party will receive. For example, an apartment goes to the wife, and a car and bank account goes to the husband.

It can be concluded that if the spouses enter into an agreement before the divorce, they will not need to pay taxes.

Paying taxes during a divorce through court

If spouses cannot divide property without disagreement, they will have to go to court. However, it is important to take into account that in the end one of the parties may end up with a large part of the property. As an example, let’s take a situation where the wife gets 80% of the apartment, and the husband gets the remaining 20%. And it is impossible to say for sure that the spouse will receive monetary compensation, since it may well not be awarded.

If the court rules that one of the spouses must pay the other monetary compensation for property, then there is no need to pay off personal income tax. This also applies to cases where a husband or wife receives an additional share of property.

If the spouses divorced and then decided to divide property

The law does not prohibit the division of property after a divorce. However, you should be prepared for the fact that in some cases an obligation to pay personal income tax may arise. This is due to the fact that the parties are no longer husband and wife.

If, after a divorce, the spouses enter into an agreement stating that the property will be divided equally between the parties, then they will not have to pay personal income tax. This is because each party gets their due share, which means there is no benefit.

If after a divorce one of the spouses receives a larger share, and the other is paid monetary compensation, then it is necessary to pay personal income tax. As an example, we can imagine a situation where a husband receives 100% of the apartment, after which he pays his wife 50% in cash. In this case, the wife is responsible for paying the tax.

If, after a divorce, the husband receives a large share of the property, and the wife is not paid monetary compensation, then the husband is responsible for repaying the tax, since it was he who received the benefit.

Taxation of marriage contract

According to the norms of the current legislation of the Russian Federation, if spouses enter into a marriage contract, then there will be no taxation when dividing property. This is due to the fact that when concluding such a contract, the spouses have no economic benefit.

Rules for the division of property if a participant leaves the LLC

If a participant leaves the ranks of the LLC, his share is distributed according to the rules prescribed in the Charter. The distribution is made in proportion to the contribution of each founder. The valuation of shares is carried out at nominal (the amount of the authorized capital) and real (proportional value of net assets) value.

Upon exit, a citizen has the right to receive a cash payment proportional to the actual value of his contribution to production. Settlement with the retiring property can also be made with the unanimous consent of the meeting.

Note: the fixed assets of the enterprise belong to all participants and cannot be the property of one founder, even if he contributed them when joining the ranks of the founders.

If the retiree does not agree with the amount of compensation paid to him, he has the right to initiate legal proceedings.

If the founders are spouses

According to the RF IC, divorce presupposes the termination of the marriage, in the process of divorce, according to Art. 34 everything acquired together is divided. The same applies to shares that were acquired in the process of living together.

The value of shares for the division can be used nominal or market. Since the nominal value usually does not exceed 10,000 rubles (formed on the basis of the amount of the authorized capital), it is recommended to use the market value, which is higher than the nominal and lower than the actual price, it corresponds to the real price for the current day.

Typically, spouses reach a common denominator in the process of division through negotiations, then the agreement is signed and notarized.

If it is not possible to reach an amicable agreement, the division of property is carried out in court.

Options for dividing property between founder-spouses

- Division of property into two equal parts in natural size - the agreed part is transferred to the spouse, after which he has the right to become a founder, but after observing certain formalities and entering data into the Unified State Register of Legal Entities.

- Payment of compensation to one of the spouses, while the other remains the founder - this option is more popular than the previous one. When using it, the real value of the share is taken into account, based on the balance sheet data or valuation of the enterprise’s property.

Please note: compensation paid in the agreed amount, not exceeding a share, is not subject to income tax for individuals.

Foreclosing on the share of the founder-spouse upon division of property

It happens that the parties accepted the option with compensation for execution, but the spouse who assumed these obligations does not fulfill them. Then the spouse awaiting payment has the right to foreclose on his share to receive compensation if the company lacks other property.

These plaintiff’s demands can be satisfied in several ways:

- The LLC reimburses the real value of part of the expected share, and subsequently the share transferred to the organization is sold in accordance with the law;

- The real value of the share is compensated by all participants of the company by unanimous decision in the amount corresponding to their contributions to the common capital, unless there are other established rules;

- If none of the above options for reimbursement is used within 3 months, the share is sold at a public auction.

It follows that when dividing property between spouses, the share of the founder of the LLC is divided in equal amounts or compensation is paid in the established way.

Difficulties in dividing jointly acquired property

The main problem that spouses face when dividing property is the jurisdiction of the claim. In this case, you need to build on the existing circumstances:

- If the value of jointly acquired property is no more than 50 thousand rubles*, and there are no disagreements about children, then you need to go to the magistrate’s court, according to the defendant’s place of residence.

- If spouses want to divide property, and there is also a dispute about children, then they need to contact the district court, according to the place of registration of the defendant.

- If the claim refers exclusively to the division of jointly acquired property, then you need to go to the court at the location of the property.

The applicant can file a claim at his place of residence, but only if there are grounds. One of them is poor health.

What the law says

In Russia, the division of common property is regulated by two legislative acts:

- Civil Code.

- Family code.

If we talk about the RF IC, then it spells out in more detail the division of property of spouses during a divorce. This legislative act regulates the following points:

- What property can be considered common.

- What things are considered the personal property of each spouse.

- How can jointly acquired property be divided? There are two ways: the first is by concluding a mutual agreement, the second is by filing a claim in court.

- The amount of share due to each spouse.

Personal belongings of spouses are not subject to division.

As for the Civil Code, you can find out from it what property is considered common, and also study the methods of dividing it.

How to divide property between the founders of a joint stock company

If a closed company, then its structure is as close as possible to an LLC, therefore the division of its property is carried out in a similar way. But if the joint-stock company is an open type, then everything depends on the meeting of shareholders, the personal participation of even the holder of the main block of shares is nominal, and he practically does not make global decisions - there are top managers for this.

Shareholders participate in the fate of the enterprise as holders of a block of shares and recipients of profits. The value of an enterprise's fixed assets is measured by the value of shares, therefore, when dividing property between the founders of an OJSC, the number of shares of each is taken into account. It is according to their number that the volume of payments for each participant is determined.